Main Points :

- The Bank of England (BoE) has published a consultation paper (10 Nov 2025) on a regulatory regime for sterling-denominated “systemic” stablecoins.

- The regime will apply only to stablecoins denominated in British pounds and deemed “systemically important” by the HM Treasury; existing major US-dollar stablecoins (e.g., USDC, USDT) are explicitly excluded.

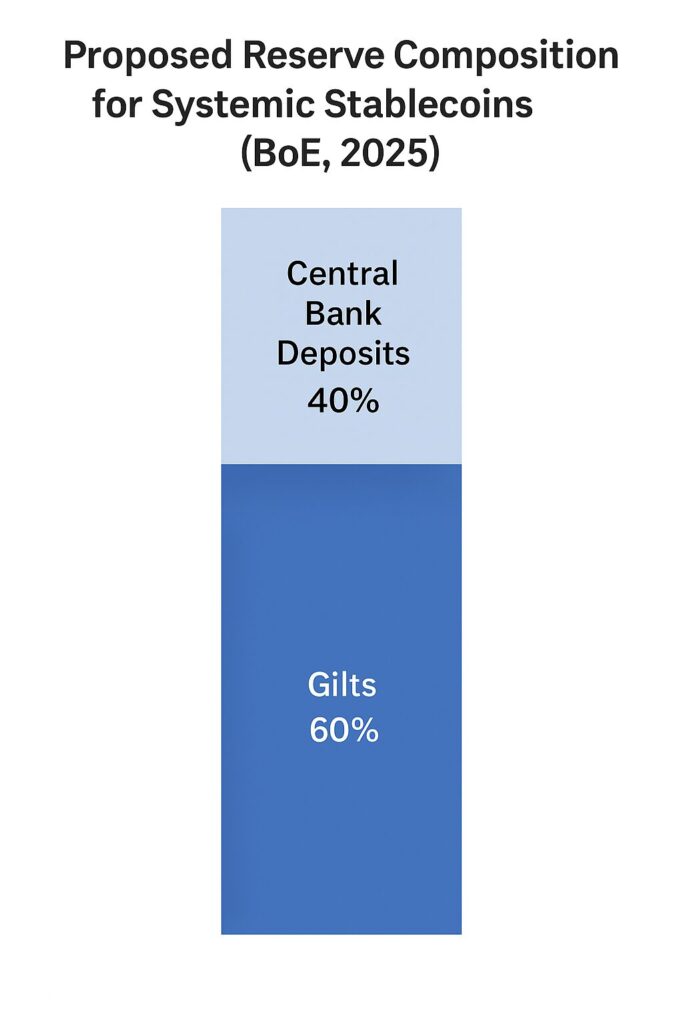

- Backing-asset rules: Up to 60 % of reserves may be held in short-term UK government debt (gilts), with at least 40 % held in unremunerated BoE deposits; for new entrants a step-up to 95 % gilts initially is permitted.

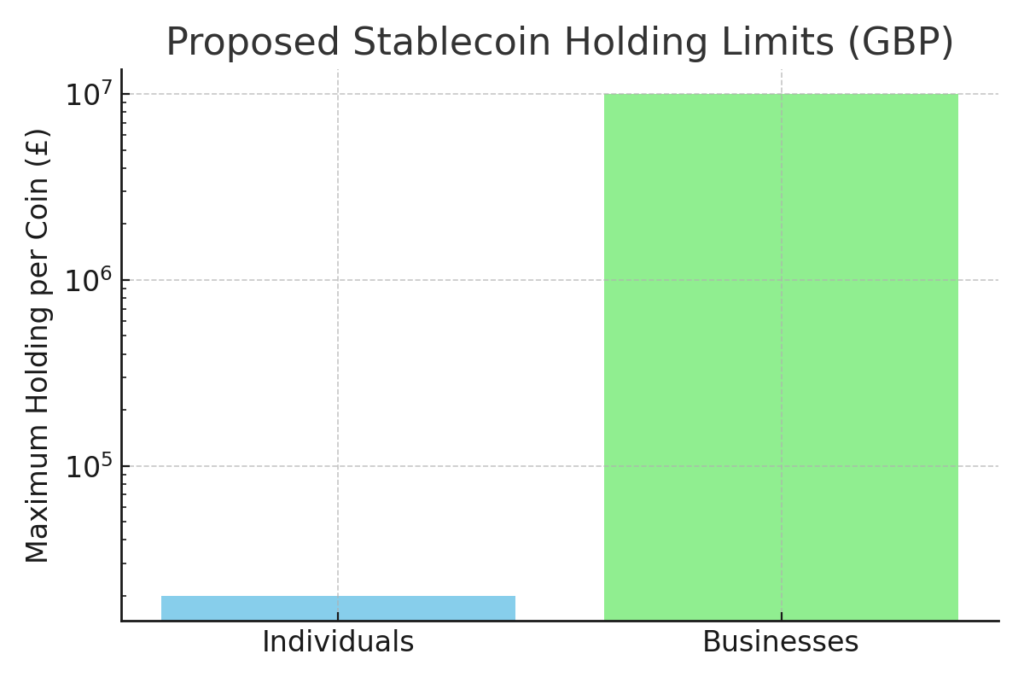

- Holding-limit proposals: Individuals may hold up to £20,000 (≈ US$26,000) in each stablecoin; most businesses may hold up to £10 million (≈ US$13 million) per coin — temporary measures to protect the banking-based mortgage economy from rapid deposit migration.

- Joint regulatory oversight: The BoE will cover prudential/financial-stability risks of systemic stablecoins; the Financial Conduct Authority (FCA) will continue to supervise non-systemic stablecoins and general conduct/consumer protection.

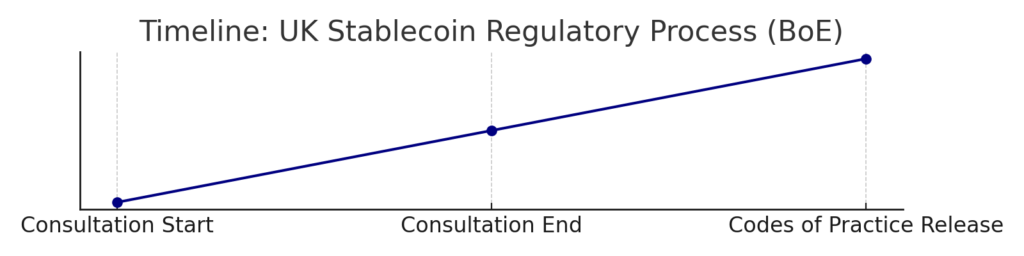

- Timeline & next steps: The consultation runs until 10 Feb 2026; subsequent detailed Codes of Practice will follow later in 2026.

- Implications for blockchain, crypto assets, and payments: The regime aims to support payment-use-case stablecoins and tokenised deposits/interoperability of public and private money in the UK.

- Strategic context: The UK seeks to keep pace with the US, while guarding its bank-based economy; global stablecoin market growth and cross-border regulatory coordination are key.

1. Setting the Scene: Why the BoE is Acting

In November 2025 the Bank of England published a consultation paper titled “Proposed regulatory regime for sterling-denominated systemic stablecoins”. The background to this is multifaceted. On one hand, the stablecoin market — global aggregations like the US-dollar-denominated assets such as USDC and USDT — has ballooned into the hundreds of billions of dollars and plays a central role in crypto-asset trading and increasingly in payments. On the other hand, regulators recognise that a future in which stablecoins play a more prominent role in retail and wholesale payments brings both opportunities (innovation, efficiency, cross-border flows) and risks (financial stability, bank deposit outflows, operational resilience).

For the UK specifically, the BoE points to its bank-centric mortgage and deposit model: if substantial funds were to migrate into stablecoins rather than bank deposits, that could undermine credit flows and deposit funding in the real-economy mortgage market. Moreover, the BoE and HM Treasury recognise that if a stablecoin becomes widely used for payments in the UK, it should be regulated akin to a payment system rather than simply another crypto asset. Governor Andrew Bailey has previously stated that widely-used stablecoins must be regulated “like money” and have access to central bank reserves.

In short: the UK is positioning itself to create a regime for stablecoins that can support innovation in payments, while preserving financial-stability guardrails and ensuring that innovation does not undermine the banking system’s role. For blockchain and crypto-asset practitioners, this signals that payment-use-case stablecoins (rather than pure trading vehicles) are heading into the regulatory spotlight — and there may be opportunities for tokenised currencies, interoperability and new business models built around compliant stablecoin issuance and usage.

2. What is a “Systemic Stablecoin” under the Proposed Regime?

The consultation paper defines a “sterling-denominated systemic stablecoin issuer” as a payment-system or service-provider that issues a stablecoin denominated in British pounds and which, if its design or operations carry a deficiency or disruption that could threaten the stability or confidence of the UK financial system, is recognised by HM Treasury under the Banking Act powers.

Key elements of the definition include:

- The coin is denominated in sterling, so US-dollar-based stablecoins (USDC, USDT) are excluded from this regime.

- The coin is likely to be widely used for payments (retail or wholesale) or cross-border flows.

- The issuer may be a non-bank issuing stablecoins, given the regime is scoped to non-bank stablecoin issuers (banks are regulated differently).

- Once the issuer is recognised as systemic, the BoE obtains powers to issue codes of practice, directions, and supervision under the Banking Act 2009.

For users and businesses in blockchain and payments, this means that if you are considering building or issuing a sterling-based stablecoin aimed at payment-use (rather than just trading), you will face a higher regulatory regime — but also a clearer pathway to legitimate use with potential central-bank interface. The regime distinguishes payment-use stablecoins (systemic) versus those used mainly for trading/exchange (non-systemic regulated by the FCA). That differentiation matters for strategy.

3. Backing Assets and Reserve Requirements: Business Model Impact

One of the most materially relevant proposals for stablecoin issuers is the backing-asset regime. In its earlier 2023 discussion paper, the BoE had proposed that backing assets must be 100% deposited at the BoE (unremunerated). Industry feedback strongly objected this as impractical for viable business models.

In the 10 November 2025 consultation, the BoE significantly softened the rule:

- Up to 60 % of backing assets may be held in short-term sterling-denominated UK government debt securities (gilts).

- At least 40 % must be held as unremunerated deposits at the BoE.

- For issuers transferring from the FCA regime or new entrants, a transitional allowance permits up to 95 % gilts (and only 5 % BoE deposit) to support early-stage growth.

- Coin-holders must not receive interest (i.e., no yield paid) from the stablecoin. This aligns it with a payment medium rather than investment vehicle.

From a practical perspective, this backing-asset design has several implications:

- For issuers: Holding substantial gilts means securing short-term government debt, which may have modest yield but also low risk. It offers more business viability compared to zero-interest BoE deposits for 100 %.

- For token design: The prohibition on paying interest to coin-holders means stablecoins under this regime must focus on payment utility, not yield-seeking. That may limit “yield farming” stablecoin models, making them more like digital cash.

- For integration: Holding BoE deposits gives potential access to a central-bank deposit window, signalling a high-trust architecture and perhaps lower credit risk — potentially useful for institutional settlement use-cases or tokenised deposits.

- For investors/use-cases: If one is building an application that uses a sterling-stablecoin for payments or settlements, this regime clarifies that such coins may be eligible for central-bank-grade infrastructure and oversight — which could enhance trust and adoption.

Hence, for blockchain practitioners and crypto investors tracking “new revenue sources”, this regulatory clarity may open new stablecoin issuance or payment-rail business models in the UK — albeit under stricter guardrails. The shift from the 2023 proposal to 2025 shows regulator responsiveness to business viability, indicating scope for innovation within defined bounds.

4. Holding-Limits and Transition Safeguards: What This Means

Another critical element of the consultation concerns holding-limits: temporary caps proposed on how much of a systemic sterling-stablecoin an individual or a business can hold per coin. These are clearly aimed at addressing rapid deposit migration risks (i.e., people shifting money from bank deposits into stablecoins), which could impact bank funding and credit flows.

Key proposals:

- Individuals: capped at £20,000 (≈ US$26,000) per coin.

- Businesses: generally capped at £10 million (≈ US$13 million) per coin. Some larger entities (e.g., supermarkets, crypto-trading platforms) may be exempt under certain circumstances.

- These are described as temporary measures, to be lifted when risks to credit availability in the real economy are judged to have subsided.

What does this mean for the crypto ecosystem and revenue/seeking opportunities?

- For end-users and token-holders: The individual cap means that sterling-stablecoins under this regime may not be suited for large-scale treasury placement by retail users (beyond £20k) in the initial phase. For individuals, these coins become more akin to transactional instruments rather than large-scale store-of-value holdings, at least initially.

- For businesses: While £10 m is large, for certain institutional treasury operations or large corporate payments this may be constraining. However, exemptions provide flexibility for significant participants.

- For issuer business models: The transition cap underscores that the regime is launching gradually; this creates window for issuers to build infrastructure, payments-rails, use-cases, and adoption before full liberalisation. It also means that business planning should anticipate a phased lifting of limitations.

- For market positioning: If you’re exploring “next-generation” stablecoin models or tokenised-payments rails, understanding that UK legislation will favour payment-use coins (with holding caps temporarily) may help you align your model accordingly: focus on transactional volume rather than large store-of-value functions in the first stage.

In context, this is a clear signal: the UK is enabling stablecoin-innovation but wants to control scale-risk initially, especially given its banking system structure. For crypto investors looking at opportunities, this means that sterling-stablecoin issuance or applications may be early adopters of UK regulation — offering first-mover advantage — but token-holders need to be aware of structural limits in the near-term.

5. Timeline, Regulatory Architecture & Cross-Border Considerations

The consultation paper provides and clarifies the regulatory architecture and transition plan.

Key timeline and architecture points:

- Consultation opens 10 November 2025 and closes 10 February 2026.

- After stakeholder feedback, the BoE and FCA will publish detailed Codes of Practice later in 2026; these will set out detailed requirements for systemic stablecoins.

- The BoE and the FCA will publish a joint approach document in 2026 to clarify regulatory responsibilities (prudential vs conduct) for stablecoins.

- The classification of “systemic” is determined by HM Treasury; non-sterling stablecoins may still be subject to UK regulation if they become systemic in the UK. For non-UK affiliates issuing stablecoins denominated in other currencies, the BoE proposes to defer to home-authority frameworks if outcomes are equivalent, with co-operation.

From a cross-border and business-model perspective:

- If you issue a stablecoin denominated in pounds (sterling), and expect substantial use in UK payments, you will likely fall under the BoE regime (once designated systemic) and thus must plan for the higher standard.

- If you issue a non-sterling coin (e.g., USD-pegged) but want UK activity, the BoE’s regime may still apply if it becomes systemically used in the UK — or you may seek “equivalence” via home-authority.

- The timeline suggests a window between now and final Codes of Practice in late 2026: an opportune moment for innovators to engage with the consultation, shape the regime, and build compliant platforms ahead of full implementation.

- For investors: the existence of this roadmap signals that UK regulators are legitimising stablecoins for payments — which means that crypto assets designed for payment rails (not only trading) may gain regulatory legitimacy and adoption — a potential source of next-generation revenue.

6. Implications for New Crypto Assets, Blockchain Use-Cases and Revenue Opportunities

Given the reader’s interest in new crypto assets, income opportunities and practical blockchain applications, the BoE’s regime has several concrete implications:

a) Payment-Use Stablecoins as Growth Opportunity

The regime favours stablecoins that are used for payments (retail, wholesale, cross-border) rather than those purely for trading. If you are designing a new crypto asset, a sterling-stablecoin (or payments-use token) that meets the regime’s design criteria could gain institutional support, central-bank linkage, and trust advantages. This may open revenue streams in: merchant payments, tokenised deposits, corporate treasury services, cross-border settlement, inter-operability with central-bank money.

b) Tokenised Deposits & New Money-Rails

The BoE explicitly mentions interoperability between systemic stablecoins, tokenised bank deposits and central-bank money. For a JavaScript/Node.js developer (as you are), this suggests a fertile ground: building infrastructure for tokenised deposit rails, APIs linking stablecoins and bank deposit systems, transparent settlement smart-contracts. Given your interest in non-custodial wallets and swaps (as per your earlier project “dzilla Wallet”), integrating with sterling-stablecoin rails or establishing EVM-compatible stablecoin rails could be lucrative.

c) Risk-Adjusted Revenue Models vs. Yield-Seeking

Since coin-holders cannot receive interest (under the payment-use design) and holding caps limit large store-of-value use, the business models will focus on transaction volume, network effects, payment fees, tokenised asset settlement rather than “yield farming”. For revenue-seekers, this points to designing utility-tokens anchored in payments/activity rather than speculative holding.

d) Market Differentiation & Geographic Coverage

With this UK regime, issuers who operate compliant sterling-stablecoins may differentiate themselves from US-dollar stablecoins in terms of regional suitability and regulatory clarity for UK and perhaps EMEA markets. If you can build a sterling-stablecoin that complies from day one, you may gain adoption amongst UK/European merchants or treasuries seeking regulatory-safe rails. For investors, the token’s regulatory compliance becomes an added layer of value (trust, auditability, adoption potential).

e) Timing for Innovation and First-Mover Advantage

We are in the consultation phase now. The opportunity exists for projects to engage with the consultation, shape the regime, build products ahead of full implementation. For someone designing wallet infrastructure or stablecoin issuance (you indicated interest in token launch), aligning with sterling stablecoin regulation could provide first-mover advantage in the UK payments market.

f) Caution: Holding Limits and Scope Constraints

However, there are constraints: holding caps mean that mass retail adoption in the UK for large-value store-of-value placements may be limited initially. Also the regime applies only to sterling-denominated coins deemed “systemic” — if your coin is USD-based or used mainly for trading, it remains under the lighter-FCA regime but may not enjoy the same central-bank-linked benefits. When designing a project, you need clear positioning: payment-rail vs trading token, sterling vs non-sterling, compliance architecture, user-cap implications.

7. Strategic Recommendations for Crypto Assets & Blockchain Practitioners

Given the above, here are actionable strategic considerations for your interests (new assets, revenue opportunities, blockchain use-cases):

- Evaluate stablecoin denomination and market geography

If you intend to target UK/EMEA payments and treasury flows, consider issuing a sterling-denominated stablecoin compliant with the BoE’s regime. Alternatively, if you focus on global/trading use, a USD-based stablecoin may still be viable but faces different regulatory contours. - Design for payment-use (volume + utility) rather than yield-seeking

Create tokenomics that reward transaction usage, merchant adoption, settlement speed, interoperability, rather than high yield. The BoE’s prohibition on interest for coin-holders signals how the regime views the instrument. - Build compliance and auditability from the start

Reserve backing (gilts + BoE deposits) requires transparency, audit, high-quality short-term assets. Your issuance model should include clear governance, reserve attestations, and readiness for regulatory oversight. - Leverage wallet infrastructure with non-custodial design

Since you’re interested in non-custodial wallet development (e.g., “dzilla Wallet”), integrate support for sterling-stablecoins and payment rails, with swaps (BTC ↔ ETH ↔ stablecoin) and seamless UX. Compliance modules (KYC, AML, monitoring) may need integration given the regime’s implications. - Explore tokenised bank deposits and rails integration

Explore partnerships with UK banks or payment-infrastructure providers to issue tokenised deposits or stablecoins that interoperate with central-bank/BoE infrastructures and the upcoming retail-payments infrastructure board. This aligns with the BoE’s stated goal. - Monitor cross-border frameworks and competitive jurisdictions

While the UK moves forward, the US has its own legislative regime (e.g., the “GENIUS Act”), Canada is drafting standards, and the EU is advancing stablecoin/digital-asset policy. For asset designers, understanding cross-border interoperability, regulatory equivalence, and geographic strategy is key. - Engage with the consultation and policy evolution

The consultation phase (until Feb 2026) offers a window for feedback and industry input. Projects can position themselves as stakeholders, shape the rules, and pre-position for regulatory compliance and promotional advantage.

8. Risks & Considerations

No regime is risk-free; here are caveats:

- Regulatory uncertainty remains: The consultation is ongoing; final Codes of Practice will come later in 2026. Operationalising a stablecoin under this yet-to-be-final framework carries implementation risk.

- Adoption risk: Holding caps might slow mass adoption, and market liquidity challenges can arise if coin-holders cannot treat the stablecoin as large-value store-of-value early on.

- Competition and network effect risk: USD-based global stablecoins carry strong network effects. A sterling-stablecoin will need to build compelling use-cases and acceptance.

- Treasury/backing risk: Holding gilts and BoE deposits may appear safe, but issuers must manage repayment risk, redemption risk, liquidity risk especially under stress scenarios (BoE letter mentions liquidity facilities for systemic stablecoins).

- Technology/infrastructure risk: Tokenised rails, inter-operability, settlement models require robust infrastructure, and non-custodial wallet design must integrate with KYC/AML frameworks if used in UK regulated environment.

- Geographic & regulatory arbitrage risk: As regulation moves ahead globally, jurisdictional mismatches may create compliance complexity; e.g., a non-UK issuer may need a UK subsidiary if issuing sterling-denominated coins.

9. Conclusion: A New Frontier for Blockchain Payments — And Revenue

The Bank of England’s November 2025 consultation marks a pivotal moment in the maturation of stablecoins and payments-use blockchain assets. By drawing the line between “systemic” sterling-stablecoins and other crypto assets, the UK is signalling that it expects stablecoins to move beyond trading-adjacent phenomena into legitimate payment rails and tokenised money forms. For readers who are exploring new crypto assets or seeking revenue-generation opportunities in blockchain, this regime offers a clear signal: there is opportunity in payment-use tokenisation, stablecoin issuance, and wallet/rail infrastructure — provided you are aligned with regulation, design your asset for utility not speculation, and integrate with tokens, rails and wallets built for transparency and compliance.

In practical terms, for wallets, swap tools, token launches, and blockchain-based payment systems, aligning with this UK framework early could create competitive advantage. The holding-limits, backing-asset rules, and regulatory timelines define constraints and shape the business model: lean toward high-frequency utility, token-networks, settlement infrastructure, interoperability, rather than pure speculation.

Finally, whether you are designing a new token, building wallet infrastructure, or identifying the next crypto-asset to invest in, the era of “just trading coins” is evolving into the era of regulated payments tokens, tokenised deposits, and interoperable rails between private money and central-bank money. The UK’s approach offers a blueprint — and for those with the developers’ mindset (such as your Node.js/web3.js background) and interest in blockchain applications, it is a timely starting point for planning what comes after yield-seeking: responsible utility in the future of money.