Main Points :

- A global bank is teaming up with a payments-network veteran to launch a credit card enabling stablecoin payments.

- The pilot is in Singapore, a jurisdiction with advanced stablecoin regulation, with plans for global roll-out.

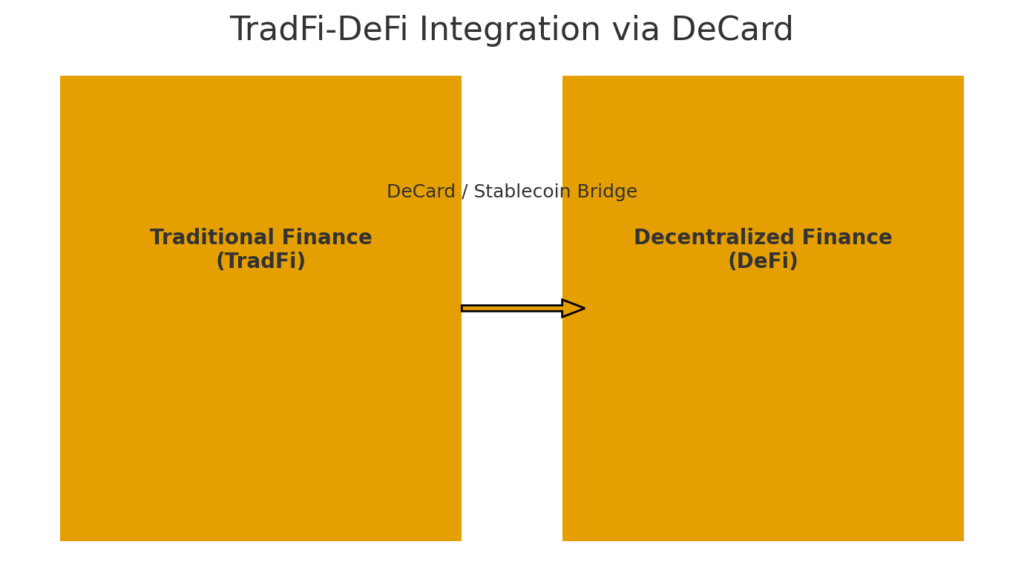

- The initiative is positioned as a bridge between traditional finance (TradFi) and decentralized finance (DeFi).

- For crypto-asset hunters and blockchain practitioners this signals a growing real-world adoption of stablecoins beyond trading.

- The regulatory backdrop in Singapore provides a blueprint for compliant stablecoin-based payment systems.

- Key implications: new payment rails, token-economy integrations, wallet-issuance possibilities, and UX/operational challenges.

1. Introduction: Finance’s Next Frontier

Global banking giant Standard Chartered Bank (StanChart) has announced a strategic partnership with DCS Card Centre (formerly Diners Club Singapore) to launch a next-generation credit card product, branded as “DeCard”, which enables direct spending of stablecoins in everyday merchant transactions. This marks a significant step for stablecoins moving from purely trading or investment assets into practical payments tools.

The pilot location is Singapore, and the intention is to expand into other major markets globally.

2. What DeCard Offers: Stablecoins for Everyday Payment

Under this partnership, Standard Chartered will serve as the principal banking partner, supporting DeCard’s payment infrastructure in multiple ways :

- Card-holder top-up processing, account management, and the settlement of both fiat and stablecoins for merchant payments.

- Treasury, liquidity management and foreign-exchange hedging support for the card business.

- API connectivity and virtual account infrastructure that allows DCS to immediately identify and reconcile incoming payments from DeCard holders across channels. This enhances transparency and efficiency.

DeCard aims to make spending stablecoins as seamless as swiping a traditional credit card, thereby bridging the gap between the crypto asset world and legacy payment rails.

3. Why Singapore? A Regulatory Sandbox and Stablecoin Hub

The choice of Singapore as the launch market is strategic. The Monetary Authority of Singapore (MAS) has established a stablecoin regulatory framework for “single-currency stablecoins” (SCS) — stablecoins pegged to SGD or a G10 currency, issued in Singapore and fully backed by reserves. Key features of this regulatory framework include:

- Issuers must maintain reserve assets equal to at least 100% of the stablecoins in circulation.

- Reserve assets must be denominated in the peg currency and held in cash, cash equivalents or short-dated debt securities (up to three-month maturity) issued by governments, central banks or supranationals.

- There must be monthly independent attestations of the reserve assets (published) and annual audits.

- Issuers must enable redemption at par within five business days.

- At the initial stage, multi-jurisdiction issuance is disallowed if the stablecoin wants the “MAS-regulated” label.

This makes Singapore one of the more forward-looking jurisdictions for regulated stablecoins. For projects and practitioners seeking real-world payments adoption, Singapore offers a clear signalling effect.

4. Implications for New Crypto Assets and Blockchain Applications

For readers hunting the next crypto opportunity, or designing blockchain-based payment systems, the DeCard announcement opens several interesting angles:

4.1 Real-World Use Case for Stablecoins

Most stablecoins today are used in trading pairs, DeFi protocols or on-chain bridges. A mainstream card means the vector shifts to consumer payments, merchant acceptance, and integration into everyday commerce. That enhances the utility layer and could increase demand for stablecoin rails or tokenised fiat.

4.2 Bridge Between TradFi and DeFi

TradFi institutions backing DeCard signals that traditional banks are actively building infrastructure bridging to DeFi. The APIs, virtual accounts and liquidity solutions show how a bank integrates token-rail services with legacy systems. This is relevant for non-custodial wallet designs, for example: how do you manage on-chain assets, off-chain settlement and UX transparency? The wallet you’re working on—‘dzilla Wallet’—could consider such hybrid rails.

4.3 Token-Economy Design and UX Considerations

Introducing a card that spends stablecoins raises UX and token-economy design questions:

- How is the conversion between stablecoin and fiat handled? Are there manual steps for the user or fully seamless settlement?

- Does the user hold stablecoins directly in the card-linked wallet or does the card provider abstract that away?

- How are credit limits, repayments, rewards, merchant acceptance handled when the underlying asset is a stablecoin rather than fiat?

These are relevant when designing wallets or payment rails: the more seamless the user journey, the broader the adoption.

4.4 Geographic Expansion and Market-Specific Roadmap

While Singapore is the pilot, global expansion is planned. That means market-specific regulatory and operational challenges. For your interest in token issuance, marketing, SNS/DISCORD integration and wallet design: consider how promotion differs by region, what KYC/AML requirements will look like, and how viral mechanisms (rewards, hashtags etc) can be leveraged when real-world payments are involved.

5. Recent Developments: Stablecoins and Payments in Asia

Beyond DeCard, other signals reinforce the trend of stablecoins moving into payments rails:

- OKX launched “OKX Pay” in Singapore in September 2025, enabling users to pay merchants on GrabPay via USDC or USDT, then converted into Singapore dollars.

- Ant International (the overseas arm of Ant Group) is seriously considering applying for stablecoin licences in multiple jurisdictions and emphasised stablecoins for global payments rather than speculative crypto products.

These developments reinforce that payments is the strategic thrust for stablecoins, not just trading. For blockchain practitioners, this means increased demand for integration of wallets, merchants, rails and infrastructure.

6. What This Means for Your Wallet Project (dzilla Wallet)

Given your interest in building a non-custodial wallet with BTC⇄ETH swaps and good UX transparency, the DeCard announcement dovetails with key considerations:

- If you support stablecoin flows in your wallet, anticipate that payment use cases (card-linked or merchant-linked spend) are becoming real. That means you may want to provide UI/UX flows that handle on-chain stablecoin holdings, conversion to fiat, settlement tracking, and merchant acceptance indicators.

- The integration of TradFi bank rails (as demonstrated by Standard Chartered) means you’ll face interoperability decisions: on-chain wallet → bank-settled card → fiat merchant settlement. What data is exposed to the user? How is the flow audited? How is transparency communicated?

- For incentives, viral mechanisms (rewards for card-linked spend, social sharing, hashtag detection) become more tangible when the underlying payment asset is a token. You can integrate token-rewards, referral bonuses, spend-based unlocks etc.

- Compliance implications: since the infrastructure moves into payments, AML/KYC, travel rules, sanctions, and audit trails become significant. While your wallet is non-custodial, partner rails (cards, banks) will impose compliance requirements.

- Market expansion: the pilot is Singapore, but your wallet may target Asia-Pacific, Southeast Asia or cross-border flows. Consider regulatory variations, regional merchant adoption, stablecoin acceptance and partner network building.

7. Challenges and Risks to Watch

While the momentum is clear, a few risks and operational hurdles remain:

- Merchant acceptance: The card is new, and real-world merchant coverage and user adoption will take time. Until the network effect is strong, spend volume may be limited.

- Volatility and liquidity: Even if stablecoins are designed to be stable, ensuring instant liquidity, fiat settlement, and managing FX risk (for merchants) remains complex. Standard Chartered is providing FX hedging support.

- Regulatory evolution: Singapore’s framework is robust but still in implementation. Other jurisdictions may impose different rules, limiting expansion speed.

- UX and consumer education: Users may still think of crypto payments as more complex than tapping a card. The smoother the UI, the higher the adoption.

- Credit-card-style risk: A card implies credit limits, repayments, fraud risk — layering token-assets adds complexity in risk management and regulatory oversight.

8. Outlook and Strategic Takeaways

For investors and blockchain practitioners, the DeCard launch signals that stablecoins are edging into the mainstream payments domain, not just speculative assets or protocol utilities. Key strategic takeaways:

- Utility builds demand: Stablecoins gain traction when they enable everyday transactions—not just trading. Payment rails amplify utility.

- Banks are key enablers: The involvement of a major global bank indicates that the infrastructure is converging between TradFi and DeFi.

- Wallets matter: Non-custodial wallets that offer seamless integration with payment-rails, token holdings, card links and UX transparency are increasingly relevant.

- Regulatory clarity matters: Singapore’s framework provides a safe pilot environment; other jurisdictions may follow or diverge.

- Token ecosystem design opportunities: If users can spend, earn, refer, carry balances in token form via cards or wallets, that opens creative incentive and token-economy models.

For someone seeking the “next asset” or “next income stream”, consider protocols or tokens that enable payments, rails adoption, stablecoin issuance, wallet integrations or merchant networks—not just speculative price plays.

9. Conclusion

The standard-bearing move by Standard Chartered and DCS to launch DeCard in Singapore marks a milestone in the stablecoin narrative. What was once largely confined to exchanges and DeFi protocols is now being embedded into real-world payments via a familiar credit-card form factor. For crypto-asset seekers and blockchain practitioners alike, this shift underscores the importance of the payment-utility vector: stablecoins, wallet-integration, merchant spend, and user-friendly rails. The regulatory backdrop in Singapore gives added credibility to the endeavour and sets a precedent for other jurisdictions. As you build your wallet, design your token model or explore new assets, keep one eye on the payment-rails dimension: the next growth wave may not just be in the token price—it may be in the volume of payments and utility.