Main Points :

- The US Senate’s passage of the GENIUS Act creates the first comprehensive federal framework for payment stablecoins, clarifying rules for issuance, reserves, and oversight.

- The CLARITY Act (aka “Digital Asset Market Clarity Act”) and other market-structure bills aim to define digital assets, clear broker/dealer regulation, and provide certainty for tokenised asset flows.

- Executives at Coinbase see the stablecoin and market-structure legislation as “mutually complementary” and liken them to lubricant for the on-chain economy, enabling capital to flow more freely into tokenised assets.

- For investors and blockchain practitioners, the regulatory clarity offers new opportunities: issuance of tokenised assets, deeper stablecoin-based finance, and enhanced institutional participation.

- Risks remain: the legislation still faces political hurdles, uneven state vs federal regulation, concerns about big-tech involvement, and the timeline for full implementation remains uncertain.

1. Introduction

In the rapidly evolving crypto and blockchain space, regulatory clarity can serve as a catalyst for growth. Recently in the United States, two major legislative efforts have advanced: the GENIUS Act (targeting stablecoins) and the CLARITY Act / other market-structure bills (targeting tokenised assets and trading infrastructure). Executives at Coinbase describe these laws as more than mere rules—they represent the “lubricant” that allows capital to flow seamlessly in the on-chain economy. In this article we explore the implications of these bills, the opportunities they create for new crypto assets and blockchain applications, and what practitioners and investors should watch going forward.

2. A New Federal Framework for Stablecoins (GENIUS Act)

2.1 What the bill does

The GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins) of 2025 represents the first major U.S. legislative framework dedicated to payment-stablecoins. Key features include:

- Definition of “payment stablecoins” (fiat- or high-quality-assets-backed digital tokens used for payments or settlement).

- Issuers must hold reserves one-to-one or in high-quality assets (e.g., U.S. Treasury bills) redeemable on demand.

- A dual regulatory track: non-bank issuers with < US$10 billion outstanding may operate under state supervision if the state regime is “substantially similar”; larger issuers must fall under federal oversight (e.g., Office of the Comptroller of the Currency (OCC) or Federal Reserve System).

- Prohibition on misleading names, commingling of funds, and issuance of payment stablecoins by unlicensed entities.

- Clarification that payment stablecoins are not securities or commodities under specified circumstances, and are not federally insured.

- Passage in the Senate on June 17 2025 with 68–30 bipartisan vote.

2.2 Why this matters for investors and blockchain applications

From the standpoint of someone hunting new crypto asset opportunities or building blockchain use-cases:

- A clear legal regime reduces issuance risk for stablecoins. A project can now plan to launch or integrate a payment-stablecoin with known regulatory guardrails.

- Institutional capital may increase its stablecoin exposures (used for settlement, DeFi, tokenised asset movement) when risk of regulatory surprise decreases. For example, stablecoin issuers can issue tokenised deposits and use blockchain rails more confidently.

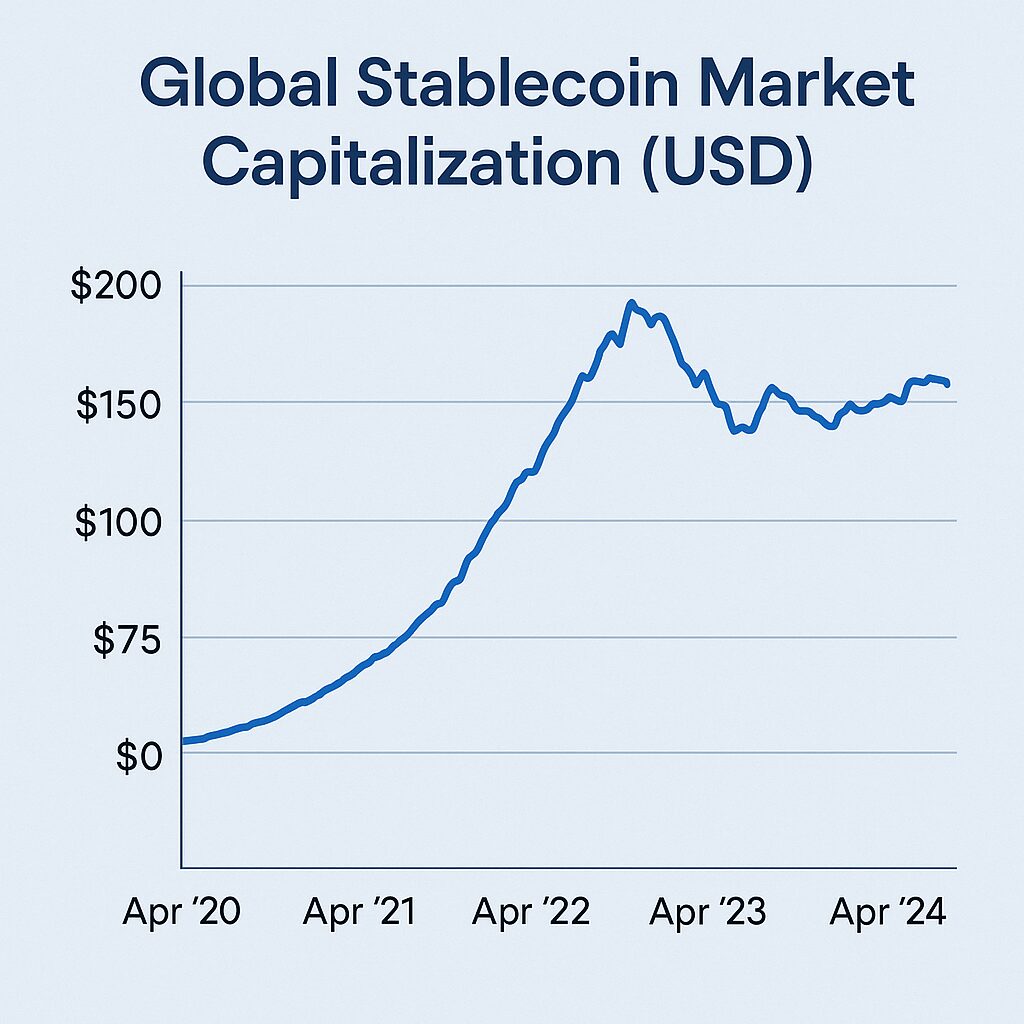

- Tokenised assets (e.g., tokenised real estate, funds, private equity) will benefit because the stablecoins backing them have a clearer underpinning. As the Coinbase executive put it, the GENIUS Act builds the “foundation” for stablecoin growth, which in turn feeds tokenisation via the market‐structure legislation.

- For blockchain practitioners: more willingness to build on-chain applications involving stablecoin transfers (e.g., money-markets on-chain, collateralised borrowing, tokenised bond or treasury flows). The clearer the rails, the easier to build compliance-aware solutions.

2.3 Outstanding issues & timeline

- The bill still requires full implementation of regulations: regulators must undertake rule-making (notice and comment) within one year of enactment; full effect will be triggered either 18 months after enactment or 120 days after final regulations by primary federal regulators.

- While Senate passage is achieved, the House and possibly reconciliations remain. Differences exist between the Senate’s GENIUS Act and the House’s alternative (e.g., STABLE Act) particularly around federal pre-emption and foreign issuers.

- Consumer-protection and AML concerns remain: critics (including Elizabeth Warren) argue the bill may open the door to big-tech stablecoin issuers and may not sufficiently protect consumers or curb conflicts of interest.

- For new blockchain applications, waiting for implementing regulations is prudent—though early movers may gain advantage.

3. Market-Structure & Tokenisation Legislation (CLARITY Act and others)

3.1 What the bills cover

While the GENIUS Act targets payment stablecoins, market-structure bills address how digital assets (including tokenised securities/commodities and tokens) are classified, traded, and regulated. Key among them: the CLARITY Act (H.R. 3633) and the Senate’s draft “Responsible Financial Innovation Act / Digital Asset Market Structure” bills.

Key elements include:

- Defining clear categories: e.g., “digital commodity”, “ancillary asset” etc., to distinguish token types and apply proper regulatory treatment.

- Expedited registration and provisional status for digital-asset exchanges, brokers and dealers under the securities laws.

- Provisions to ensure that tokenised asset offerings (e.g., tokenised funds, securities, real-world assets) can be accommodated within the regulatory framework, providing certainty for issuance and secondary markets.

- The House passed the CLARITY Act on July 17 2025 by a vote of 294-134.

3.2 Implications for blockchain practitioners and investors

- For builders: With clearer definitions and trading infrastructure, projects can now more confidently design tokenised asset platforms (e.g., tokenised funds, real estate, private credit). The regulatory architecture lowers the risk of being classified as an unregistered securities offering.

- For investors: Tokenised assets become more accessible. Capital deployed via stablecoins can flow into tokenised assets more directly. The “1 + 1 = 3” effect described by Coinbase’s senior executive is precisely that: stablecoin growth + tokenisation framework = amplified on-chain capital movement.

- For yield and product innovation: Because stablecoins may be used as collateral, or as payment rails for tokenised asset transactions, new yield opportunities (on-chain money markets, tokenised debt, fractionalised real-world assets) may accelerate.

- For strategic partnerships: Traditional financial institutions may now enter blockchain niches (e.g., tokenised bond desks, digital-asset custody). Projects that integrate fiat on- and off-ramps, regulatory-adherent compliance modules, and tokenised asset issuance will have first-mover advantage.

3.3 Risks and timing

- Reconciliation between House and Senate versions is still ongoing: jurisdictional issues (SEC vs CFTC), definitions, and scope remain unresolved.

- The timeline is uncertain: regulatory implementation may lag, and companies building today must anticipate both technology and law. For investors seeking immediate yield, waiting for clarity may reduce risk.

- Even with legislation, state‐level regulation (and enforcement) may differ greatly, raising complexity for projects operating across states or issuing tokenised assets globally.

4. The Synergy: On‐Chain Economy Taking Off

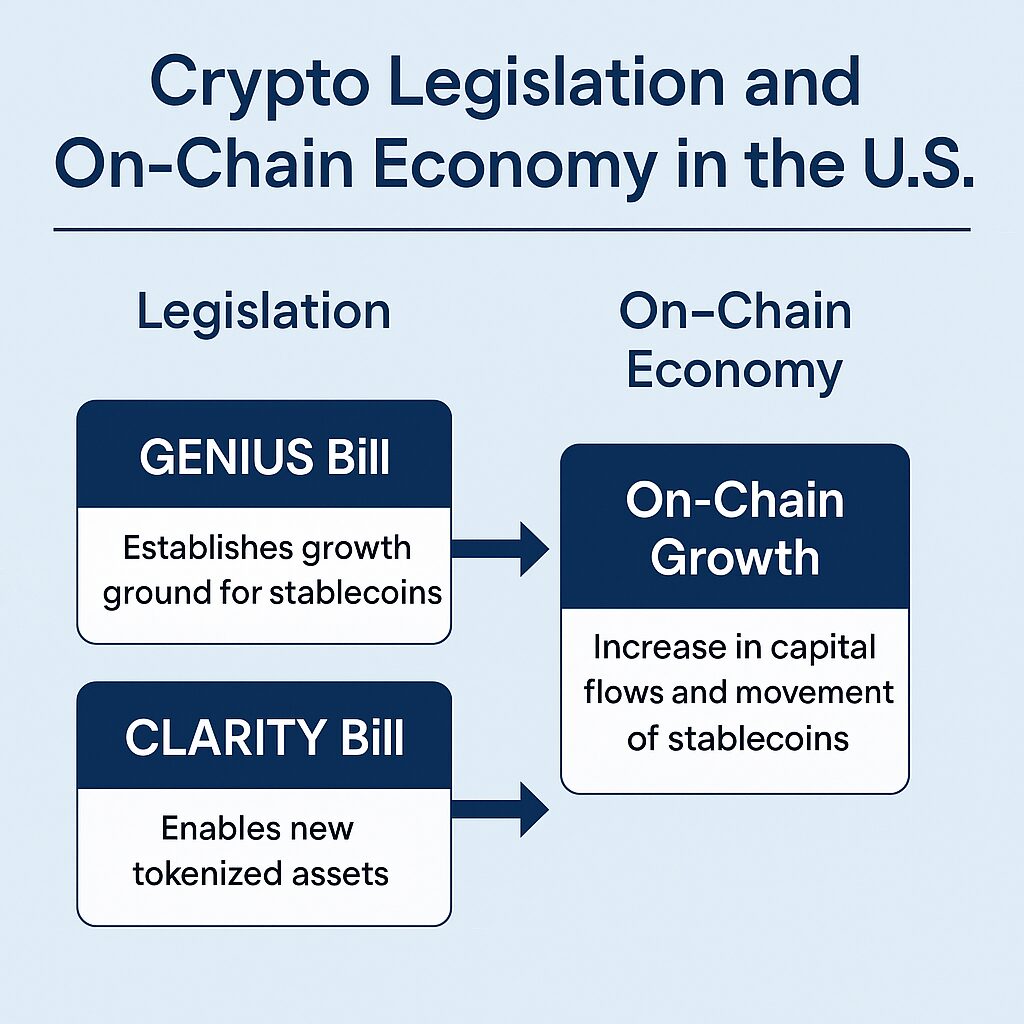

Executives at Coinbase (e.g., Sean Aggarwal and Scott Meadows) emphasise how the stablecoin and market-structure bills are not isolated—they work together as “lubricant” for on-chain capital flows.

“The GENIUS Act built the growth base for stablecoins; with supply increasing, more capital flows on-chain, and the CLARITY Act enables tokenised assets, so that the capital in stablecoins moves into tokenised markets.” — Sean Aggarwal

“With clarity from GENIUS and market structure from CLARITY, the effect is 1+1=3: clear rules plus engagement thresholds means a full ecosystem forms.” — Scott Meadows

For new crypto assets and blockchain applications, this means:

- Projects can utilise regulated stablecoins as on-chain liquidity rails for tokenised assets.

- Tokenised assets (e.g., real-world debt, private equity, real-estate) become more deployable on-chain, increasing the addressable market.

- Institutional investors may now allocate capital into on-chain yield markets, tokenised assets, or hybrid structures, expanding liquidity, promoting scale, and boosting infrastructure investment.

- Builders of blockchain platforms (wallets, tokenisation platforms, DeFi protocols) now can design with regulatory-aware architecture from the outset (e.g., KYC/AML modules, reserve audits, compliance integrations).

Thus, for anyone looking for the next revenue source or practical blockchain application, the window is opening. Rather than merely trading bitcoin or ETH, the frontier is: stablecoin-enabled tokenised assets and enterprise-grade blockchain rails.

5. Strategic Recommendations for New Asset Hunters & Blockchain Builders

Here are practical thoughts for readers:

- Select compliant stablecoins: When building on-chain applications or issuing tokenised assets, ensure the underlying stablecoin adheres (or plans to adhere) to frameworks like the GENIUS Act. This will reduce legal risk and improve institutional access.

- Plan tokenised asset issuance: With market-structure rules emerging, consider tokenising real-world assets (e.g., mortgages, bonds, real-estate equity) and leveraging stablecoin rails for settlement.

- Focus on infrastructure and middleware: Middleware that handles reserve-backed token settlement, audit transparency, and compliance automation will be in demand.

- Monitor regulatory timeline: Even though bills have passed parts of Congress, full implementation takes time. Projects ready before mass adoption can secure first-mover advantage, but also must manage regulatory uncertainty.

- Build for institutional involvement: Institutional capital is key. Projects that integrate custody, audit, regulatory reporting, and tokenisation of large-scale assets will stand out.

- Watch for yield opportunities: On-chain money markets backed by regulated stablecoins, tokenised fixed-income streams, and settlement of tokenised assets may present new yield avenues. For investors, this means looking beyond simple spot crypto holdings.

6. Case Study: Coinbase & the Ripple Effect

Coinbase stock surged following the Senate’s passage of the GENIUS Act: shares rose as much as 17% to around US$297.44, driven by investor optimism about the regulatory tailwind. This illustrates how regulatory clarity translates into market momentum—and for new crypto asset architects, that momentum can translate into user adoption, capital inflows and ecosystem growth.

7. Summary & Outlook

In summary, the twin regulatory advances—the GENIUS Act for stablecoins and the CLARITY/market-structure bills for tokenised assets—mark a watershed moment for the crypto and blockchain industry. For investors and builders seeking the next wave of opportunity, the substantive take-aways are: stablecoin rails are being legitimised, tokenised real-world asset frameworks are coming into view, and the on-chain economy is likely to enter a new phase of capital efficiency and institutional participation.

That said, execution and regulatory detail matter: rule-making, regulatory alignment across states, institutional readiness and technology integration will determine who wins. For those ready to act now—designing tokenised asset platforms, integrating compliant stablecoins, building the infrastructure for on-chain finance—the potential reward is substantial. The on-chain economy’s lubricant is now being poured—will you be positioned to capitalise?