Key Points :

- The “hash-price” (expected daily revenue per TH/s of mining power) for the Bitcoin network has fallen to its lowest level since April, following a ~20 % drop in BTC price and weak transaction-fee income.

- Network hashrate remains elevated above ~1.1 ZH/s and mining difficulty has reached a new high (~156 T), pressuring miner profitability.

- Miners are responding by shifting toward more stable revenue operations—especially leasing infrastructure or converting facilities for AI and high-performance computing (HPC) workloads.

- For crypto investors and those seeking new asset or infrastructure plays, this shift may mark an inflection point: mining now more than ever must be viewed not just as block-reward chasing, but as data-centre/infrastructure business.

- From a practical blockchain use-case perspective, this dynamic highlights how “proof-of-work” infrastructure is increasingly being repurposed into broader compute-services, suggesting opportunities in adjacent sectors (AI, data-centres, hosting) rather than just coin mining.

1. What is “Hash-Price” and Why Does it Matter?

The term “hash-price” was coined by Luxor Technologies and is broadly defined as the expected daily revenue in USD for one TH/s (tera-hash per second) of mining power.

In simple terms, if you operate mining equipment with 1 TH/s of hashrate, the hash-price number tells you roughly how much revenue you’d generate per day before costs. It is influenced by:

- The price of Bitcoin (higher price = higher USD revenue for same coin mined)

- The block-reward subsidy and transaction-fee income (total coins + fees earned)

- The network difficulty and hashrate (higher difficulty means more work for same reward)

Thus, hash-price is a key profitability metric for miners: it helps assess how much revenue they can expect from a given hashrate, and whether the operation remains viable given electricity and capital costs. For the broader ecosystem, falling hash-price can indicate stress in the mining business, which may lead to miner shutdowns, lower hashrate, or weaker network security—but may also create re-purposing opportunities for infrastructure.

2. Current Mining Landscape: Revenue Squeeze + Rising Cost Base

2.1 Hash-price Has Dropped Significantly

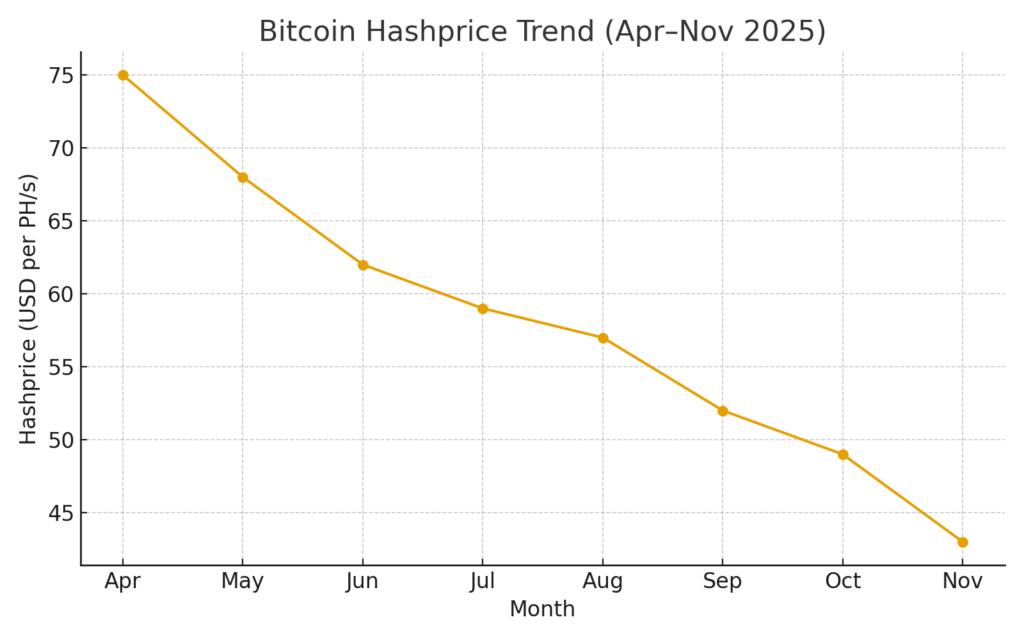

According to recent data, the Bitcoin hash-price has dropped to US$43.1 per PH/s (i.e., per petahash; note 1 PH = 1,000 TH) which is the lowest since April.

In April, with BTC trading around about US$76,000 (the article reference) the hash-price was materially higher.

This sharp drop reflects a combination of: the ~20 % drop in BTC price from its October highs (~US$104,000) to currently-lower levels; weak transaction-fee income (fees per transaction remain low); and an increased challenge due to the elevated network difficulty and hashrate.

2.2 Network Hashrate and Difficulty Are Still High

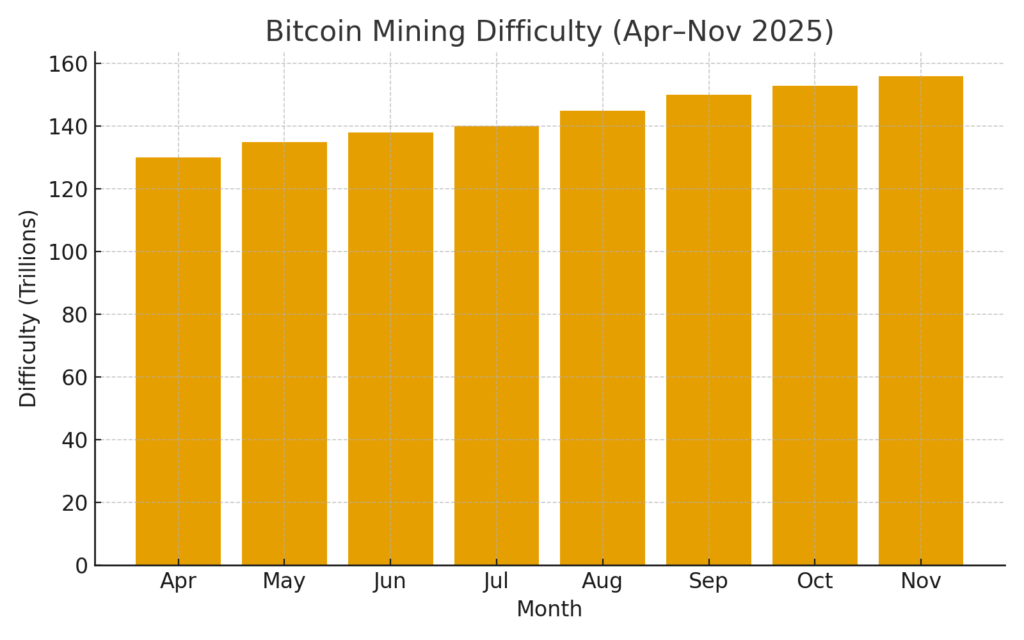

Despite the revenue drop, the Bitcoin network’s total hashrate remains at very high levels: over ~1.1 Zetta-hash per second (ZH/s).

The mining difficulty has just been adjusted upward about 6.3 % and reached ~156 trillion (T) difficulty-units, the highest on record to date.

What this means: miners are working harder, and the competitive environment remains intense—so the revenue per unit of hardware (hash-price) is squeezed, while costs (electricity, hardware depreciation) remain material.

2.3 Impact on Miner Profitability

As a result of the revenue squeeze + intense competition, miner margins are under pressure. Miner profitability in September reportedly declined by over 7 % year-on-year (reported by ForkLog).

Utilities, electricity, hardware cost increases, and difficulty upward trends all tighten the margin. On the flip side, some miners report positive earnings growth because they scale or diversify—but the overall signal is caution.

3. Strategic Shift: Mining Firms Pivot to AI/HPC Hosting

Given these structural pressures, miners are moving decisively to pivot their business model. Several key dynamics are at play:

- Existing mining facilities have large land, power infrastructure, cooling, connectivity—attributes valuable for AI/HPC workloads.

- AI-ready data centre demand is growing rapidly (McKinsey estimates ~33 % annual growth 2023-2030), so converting mining infrastructure has potential for higher-margin, longer-term contracts with data companies.

- Miners want to stabilise cash-flow and reduce dependence on highly volatile Bitcoin production revenue—which fluctuates with BTC price, difficulty, and hashrate.

3.1 Examples of the Shift

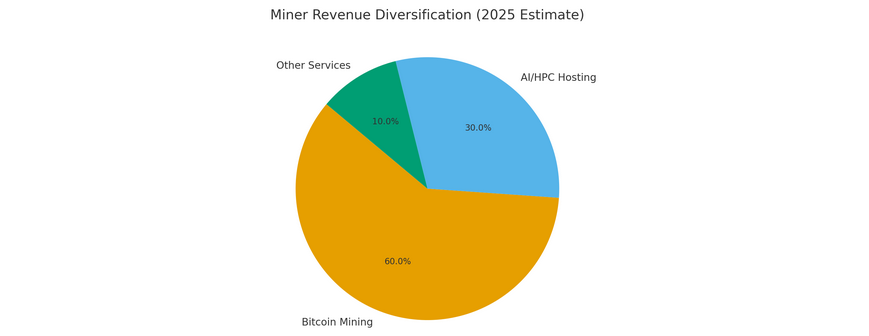

One illustration: miner-operator Cipher Mining reported its self-mining hashrate rose to ~23.6 EH/s in Q3 2025 (up ~40 % Q-on-Q), yet the headline takeaway was strategic: the firm emphasised an “AI hosting” transition as driving ~65 % revenue growth in that segment.

Another: The report by RSM US highlighted that Bitcoin miners’ investor priorities are shifting: miners with AI/HPC hosting already have higher multiples, and those that retrofit mining facilities gain a competitive edge.

3.2 Implications for Investors and Blockchain Practitioners

For readers seeking new crypto assets or infrastructure plays: this trend opens two interesting vantage-points:

- Infrastructure exposure: Rather than pure coin-mining exposure, there may be opportunity in firms converting to compute-hosting / data-centre services, which have longer-term contracts and are less exposed purely to Bitcoin price swings.

- Token / project exposure: For blockchain projects or new crypto assets exploring mining or compute-backing models, the shift suggests the importance of diversified revenue models. A project tied purely to proof-of-work coin production may face margin pressure; but one that integrates compute/hosting or AI-adjacent services could have stronger business fundamentals.

- Technical use-case: The repurposing of mining infrastructure to compute-services reflects how blockchain-industry hardware is converging with broader data-centre/AI infrastructure. For blockchain practitioners, this means that deployment, hosting, cooling, power efficiency, connectivity—all typical for mining—are now more relevant to hybrid compute infrastructures (mining + AI + HPC). That means new asset classes or service models might emerge around “compute-commodity” rather than “hash-commodity”.

4. What This Means for New Crypto Assets & Income Opportunities

For our target audience—readers looking for new crypto assets, next-income sources, and practical blockchain uses—here are some derived implications:

4.1 Mining’s diminishing margin suggests higher consolidation

As hash-price drops, smaller or high-cost miners may exit or be acquired. This could lead to fewer but larger, more efficient operations—suggesting projects that rely on decentralised low-scale mining may face headwinds. Projects or tokens aligning with large-scale efficient operations may have advantage.

This dynamic also means that hardware-intensive tokens (PoW altcoins) may face the same profitability squeeze unless they optimise energy or diversify revenue.

4.2 Infrastructure-adjacent assets gain attractiveness

Tokens or projects tied to compute-hosting, data-centre co-location, GPU/ASIC leasing, AI-compute services or similar may become more interesting. For example, a blockchain token that provides compute-resource monetisation, or a platform that connects spare compute/hardware with AI workloads, might capture part of this transition.

If a project can leverage mining‐derived infrastructure (power contracts, cooling, land) but then host AI/HPC workloads and tokenise that service, it may present a new income stream beyond pure coin mining.

4.3 Blockchain use‐cases around service-layer (hosting + KPI) become more relevant

One practical utilisation for blockchain is in the traceability, contracting, and tokenised monetisation of compute services. For example:

- A platform that records SLA metrics of hosting or compute via smart contracts (uptime, cooling efficiency, energy footprint) and issues tokens to customers or hosts.

- A compute‐market where spare hashing/compute capacity can be rented out and billed automatically via blockchain tokens or stablecoins.

Thus, the pivot of miners into HPC/AI can catalyse new token use-cases at the edge of crypto + infrastructure.

4.4 Timing matters: when to evaluate entry or exposure

Given that hash-price is at a multi-month low, margins are tight today; but if Bitcoin price recovers or transaction fees increase (e.g., via more on-chain usage), hash-price could rebound. For income-seeking investors, this may signal an entry point—but one still must assess cost structure (electricity, hardware efficiency) and diversification.

Meanwhile, for infrastructure plays, the AI/HPC demand tailwinds are longer-term (2023-30 growth ~33 % p.a.) per McKinsey quoted in the RSM report.

Therefore, smart strategy may involve a dual lens: short-to-mid term: mining facilities under pressure; longer term: compute hosting/infrastructure services rising.

5. Risks & Considerations

- Energy / cost risk: Mining remains energy-intensive. Even with low hash-price, if a miner has access to very cheap electricity (renewables, subsidised), they may survive; but marginal miners face shut-offs.

- Regulatory/environmental risk: Proof-of-work mining has environmental scrutiny (high electricity consumption, carbon footprint) which may lead to additional costs or limits.

- Compute-conversion complexity: Converting mining infrastructure into AI/HPC hosting isn’t trivial: latency, connectivity, cooling, location (often near metropolitan hubs) differ from remote, cheap-power mining sites.

- Bitcoin price dependency: Despite diversification, many miners still hold large Bitcoin inventories or operate self-mining, so they remain exposed to Bitcoin price swings.

- Token/asset risk: For new cryptos or infrastructure tokens tied to these trends, one must assess token economics, utility, governance, and avoid projects that simply hype “mining pivot” without real infrastructure or contract backlog.

Conclusion

In summary, the mining sector of the Bitcoin ecosystem is undergoing a pivotal shift. The hash-price for Bitcoin has dropped to multi-month lows (~US$43.1 per PH/s), driven by a ~20 % drop in Bitcoin price, weak transaction fees and rising network difficulty. At the same time, network hashrate remains high (>1.1 ZH/s) and difficulty is near record levels, pressuring miner profit margins.

In response, many mining firms are pivoting away from pure block-reward mining toward more stable compute-hosting and AI/HPC operations—leveraging their infrastructure, power contracts and land assets to secure longer-term, less volatile revenue streams. For crypto investors and new asset hunters, this dynamic suggests that the “mining narrative” is expanding beyond pure coin production into the broader compute-infrastructure business, opening opportunities in tokens or platforms that bridge mining/infrastructure with AI or data-centre services.

That means, from a practical standpoint, projects or tokens with exposure to compute-hosting, infrastructure monetisation, and blockchain-based service layers (such as renting compute power or tracking SLA via smart contracts) may have compelling appeal—especially in a world where pure mining margins are under pressure.

For readers seeking new crypto assets or revenue streams, I thus recommend evaluating both: (1) mining-adjacent infrastructure tokens or platforms that offer real compute/service value, and (2) PoW mining projects only if they have very low cost structures, diversification strategies, or strong margin differentiation. As blockchain use-cases evolve, we may increasingly view mining not merely as coin creation, but as compute creation—and tokens that capture compute economics may become the next frontier.