Main Points :

- Europe is considering the creation of a unified supervisory authority to oversee both digital assets and traditional securities, signalling a major regulatory shift.

- This initiative aims to eliminate “dual regulatory compliance” burdens and accelerate market entrance in the European region, especially for hybrid tokenised financial instruments.

- The strategy reflects a paradigm in which crypto-assets are not transient phenomena, but permanently embedded components of the financial system.

- The larger goal: build a single digital financial market across Europe that removes regulatory fragmentation and fosters innovation and scale.

- For institutional and legacy financial players, this is a test of commitment to digital transformation and readiness to adapt.

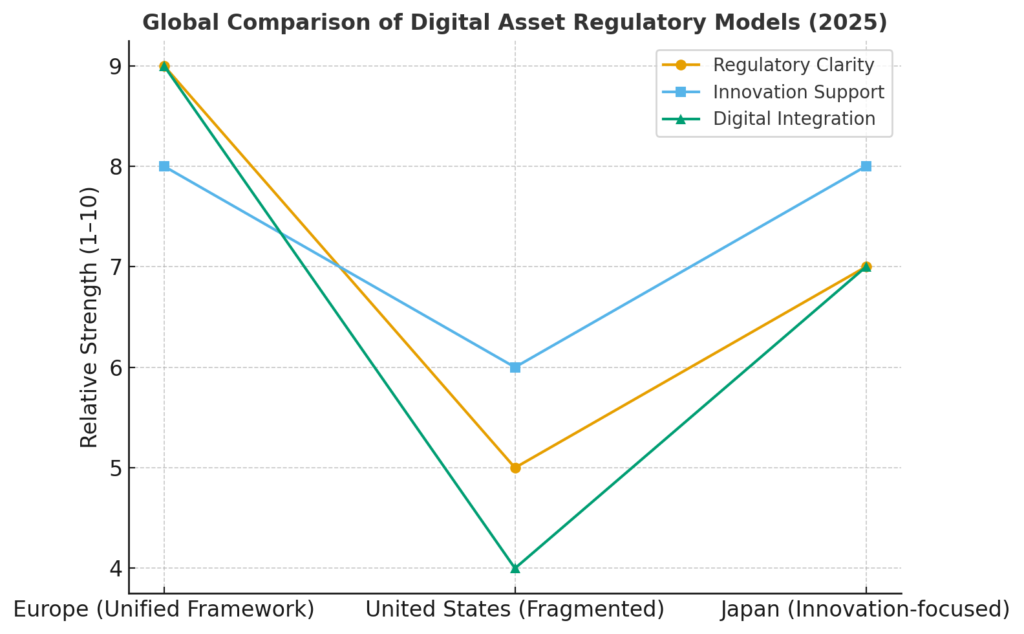

- Globally, this move triggers a regulatory race. Japan and other jurisdictions must navigate how to position themselves between the U.S. and Europe.

- Japan in particular must decide whether to build its own innovation-oriented regulatory model and reinforce its role as an Asian hub.

- The European strategy has implications for the restructuring of global finance: regions that lag may lose competitiveness in a world where digital assets are formalised within mainstream systems.

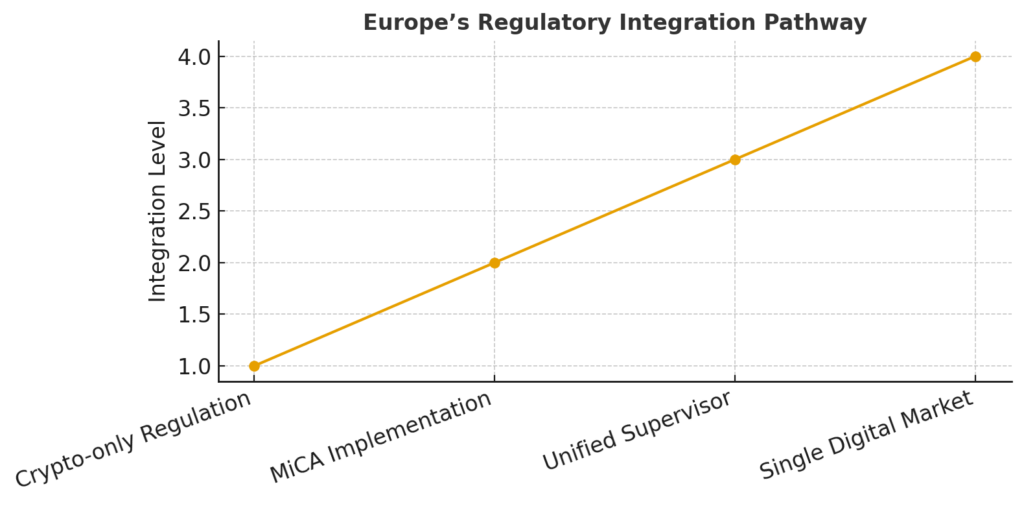

1. Europe’s Move to Destroy Regulatory Walls: The Shock of a Unified Supervisor

The recent news that the European Securities and Markets Authority (ESMA) may be expanded into a single supervisory body covering both crypto-assets and traditional securities marks a watershed moment.

While the Markets in Crypto‑Assets Regulation (MiCA) already offers a harmonised framework for many crypto-asset issuers and service providers within the European Commission’s digital finance agenda, the establishment of a broader regulator would blur the regulatory boundary between “crypto” and “securities” in a decisive way.

For companies developing new tokenised securities, stablecoins, or hybrid instruments, this may be interpreted as Europe signalling that crypto-assets are not side-projects but permanent, regulated components of the financial ecosystem. This signal alone could alter investor sentiment, strategic planning, and innovation pipelines.

1.1 Eliminating “dual regulation”: Accelerating access to the European market

Historically many companies in the digital asset or tokenisation space have faced “dual regulation” where crypto-assets fell under one regime and securities under another—leading to complexity, cost and uncertainty.

By consolidating supervision, European firms (and global firms targeting Europe) may face fewer overlapping obligations, lower compliance cost and a more certain regulatory path—which in turn could accelerate entry into the European market.

As many commentators note, this is especially relevant for tokenised securities and hybrid offerings that straddle both worlds—those products may now be more easily developed and scaled under one unified framework.

This is clearly strategic for Europe: it supports fintech innovation, shows regulatory clarity, and positions the region as an attractive territory for cross-border scaling of digital finance.

1.2 Establishing permanence: Crypto-assets as system components

By proposing a regulator that views crypto and securities under the same roof, Europe is making clear that crypto-assets are not temporary or speculative, but intended to be embedded permanently in the financial system.

This move legitimises the sector in the eyes of institutional capital and conventional financial firms. With regulatory oversight approaching the same level as securities, the confidence barrier for large investors may decline.

In short: the message is that crypto-assets are here to stay, and the regulatory architecture will reflect that permanence.

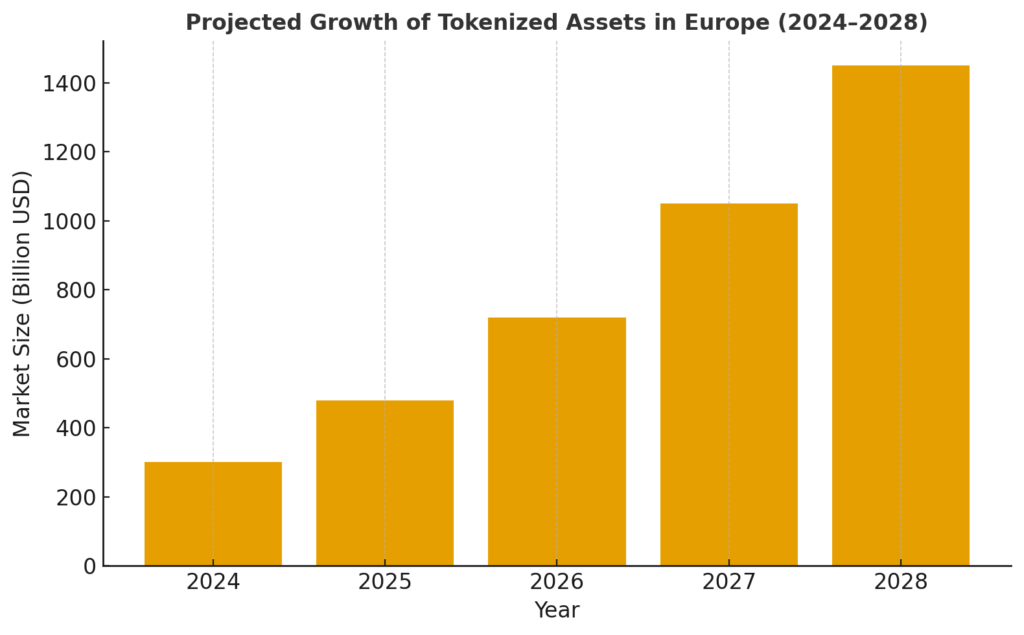

2. Irreversible Change: Europe’s Vision for a “Single Digital Financial Market”

What this regulatory consolidation really underpins is a much larger ambition: the creation of one seamless European digital financial market.

Rather than disparate regimes across member states, Europe aims to build cross-border fluidity for digital assets and tokenised instruments.

2.1 The paradox of regulation enabling innovation

At first glance, stronger regulation might appear to hamper innovation. Yet the paradox here is that by creating clarity, uniform rules, and reduced fragmentation, regulation becomes a catalyst for innovation.

Under Digital Operational Resilience Act (DORA) and MiCA, the EU has already demonstrated this approach: strong frameworks, yet explicitly enabling digital finance.

Companies can redirect resources from navigating regulatory ambiguity into building new technologies and services, confident they understand the rules of engagement. Europe is signalling: “Come build in Europe under clear rules.”

2.2 A test for traditional financial institutions’ readiness

This movement also places a burden on incumbent banks, custodians and financial institutions. If there is one regulator for both crypto and securities, these institutions must adapt their legacy systems, personnel, controls, and culture to manage digital-asset risk, custody, token issuance, trading, and settlement.

Those that fail to adapt risk being sidelined as new digital-native players gain scale under the unified regime.

Thus, the regulatory shift is in some ways a trial of legacy institutions’ “digital readiness” and commitment to embrace tokenisation.

3. The Global Alarm Bell of Regulatory Competition: Challenges for Japan

As Europe charges ahead, this isn’t just a regional story—it presents a global regulatory inflection. And for Japan, this trend raises strategic questions.

3.1 Japan’s strategic positioning

Japan must evaluate how it positions itself between the two emerging poles: the U.S. (with its fragmented enforcement-driven regime) and Europe (with its unified, regulatory-framework-driven approach).

Japan could either follow Europe’s model of clear, harmonised digital finance regulation, or carve its own path—emphasising innovation, tokenisation, and Asia-centric market leadership.

Already in areas such as regulated stablecoins and domestic virtual asset service provider (VASP) rules, Japan has shown leadership; reinforcing those strengths and leveraging them to become an Asian hub may yield strategic advantage.

3.2 The looming re-engineering of global finance

The European strategy is not just regulatory housekeeping—it may precipitate a deeper re-ordering of global financial flows, structures and competitive standings.

If Europe becomes the preferred zone for tokenised securities, institutional capital flows, and regulated digital-asset business, then markets in other jurisdictions could see relative declines unless they respond proactively.

For Japanese financial and Web3 firms, the imperative is to monitor this shift and adapt quickly: maintaining competitiveness may require stepping up regulatory clarity, innovation incentives, and cross-border connectivity.

Recent Developments & Context

Beyond the original article’s focus, some critical updates provide further texture:

- MiCA and its companion regulation Regulation on information accompanying transfers of funds and certain crypto‑assets became fully applicable across EU member states by 30 December 2024.

- Crypto-asset service providers (CASPs) and issuers of asset-referenced tokens (ARTs) and e-money tokens (EMTs) are now subject to EU-wide authorisation regimes.

- The European Supervisory Authorities (ESAs) have issued a public warning to consumers that crypto-assets carry risk and emphasised that consumer protection may be limited depending on the asset type.

- A recent regulatory source states that the evolving global crypto regulatory landscape emphasises the need for harmonised, proportionate frameworks to foster innovation while maintaining market integrity and safety.

- On the supervisory front, the push to centralise crypto supervision under ESMA is generating resistance among some national regulators, e.g., the Malta Financial Services Authority (MFSA) has opposed further centralisation citing bureaucracy concerns.

For our audience—those seeking new crypto assets, income opportunities, and real-world blockchain applications—the implications are real:

- Tokenised securities may become more accessible in Europe, offering new yield and asset-class opportunities.

- Projects targeting Europe should anticipate stronger oversight, clearer compliance obligations, and thus potentially lower friction for institutional participation.

- Conversely, jurisdictions lagging the regulatory curve may face higher risk or loss of competitive edge—project strategy must account for jurisdictional regulation as part of asset selection and partnerships.

Conclusion

What we are witnessing is potentially a landmark evolution: a shift from fragmented national crypto regimes toward unified, cross-border digital finance markets. Europe is positioning crypto-assets not as fringe experimentation but integral components of regulated financial systems. For innovators, investors and blockchain practitioners, this offers both opportunity and challenge.

Opportunity lies in gaining clearer access to large, institutional pools of capital, leveraging tokenisation and cross-border issuance under a coherent framework. Challenge lies in navigating compliance, adapting to shifting regulation, and anticipating how competitive positioning across jurisdictions (Europe, Japan, U.S., Asia) will evolve.

For Japan and other jurisdictions, the question is not simply “Will we regulate crypto?” but “How will we regulate it to be competitive and innovation-friendly while robust?” The next decade may see winners and losers determined by regulatory agility and alignment with the digital-asset future.