Main Points :

- The European Central Bank (ECB) is pushing ahead with a retail central-bank digital currency (CBDC) — the “digital euro” — aiming for first issuance around 2029.

- The ECB describes the digital euro as a symbol of European unity and monetary sovereignty in a digitising payments environment.

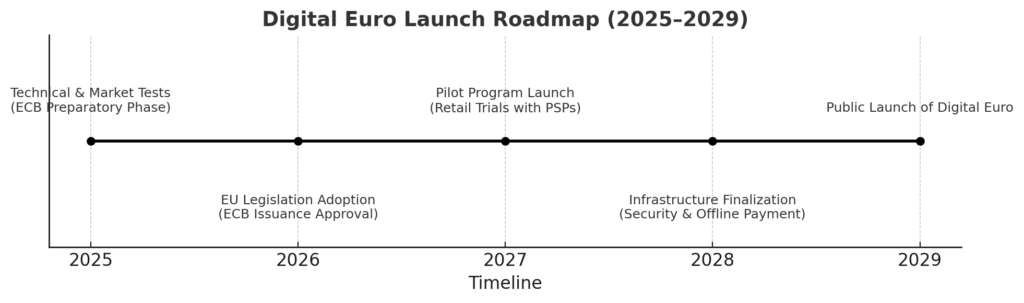

- The project encompasses technical readiness (including offline payments), market engagement (merchants/PSPs) and legislative input — and is contingent on EU law adoption in 2026.

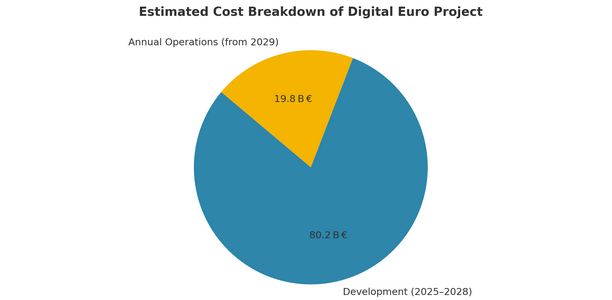

- Estimated development costs: ~€1.3 billion (≈ US$1.5 billion) up to issuance; annual operating cost ~€320 million (~US$350 million) from 2029.

- The crypto/DeFi community raises major concerns over privacy, decentralisation and potential surveillance; meanwhile, right-wing politicians in France and Germany propose banning CBDCs and embracing Bitcoin (BTC) instead.

1. A New Form of Euro-Cash

The digital euro is not intended to replace banknotes or coins, but to complement them. According to the ECB’s FAQ, users would still have the freedom to choose between cash and the digital euro for payments.

From the user’s perspective, the ambition is to have a digital means of payment that is as widely accepted as cash, both in physical shops and online, and functional even when connectivity is limited.

By deploying the digital euro, the ECB aims to make Europe’s payment landscape more resilient, inclusive and competitive — to reduce dependence on non-European payment systems and to reinforce its monetary sovereignty.

In practical terms for someone interested in crypto or blockchain: this initiative illustrates how a major central bank is integrating digital payment infrastructure with what amount to token-like properties — offline use, peer-to-peer value transfer, digital acceptance layer. Although the project is not decentralised in the sense of public permissionless blockchains, the architecture will likely involve “digital tokens” issued and overseen by the central bank, interoperable with private payment service providers under open standards.

2. Timeline, Cost and Scope

The ECB publicly outlines a “working assumption” timeline: if legislation is adopted in the course of 2026, a pilot phase could begin by mid-2027, and the Eurosystem aims for first issuance during 2029.

Cost estimates: development until issuance ~€1.3 billion (≈ US $1.5 billion); operating cost ~€320 million (~US $350 million) annually from 2029.

From a blockchain perspective, this means the window between pilot and full launch (2027-2029) may open opportunities for fintechs and payment providers to integrate with or build on the digital-euro infrastructure. For developers and token-issuers (or wallets), this could be a design-opportunity to build interoperability, value-added services, or merchant integrations around the digital-euro rails.

3. Technical Architecture & Design Considerations

The ECB emphasises three principal work-streams:

- Technical readiness: building the foundation, validating core functionalities (including offline payments) and selecting component providers.

- Market engagement: working with payment service providers (PSPs), merchants and consumer representatives — designing an ecosystem that supports the digital euro alongside existing payments infrastructure.

- Legislative support: liaising with EU co-legislators, providing technical input, calibrating e.g., holding limits or compensation models.

Notably, the digital euro is being designed with features often discussed in blockchain/crypto circles: offline functionality (so payments when internet is down), interoperability, open standards, and possibly co-badging with physical cards and e-wallets.

For practitioners in blockchain, this suggests a hybrid architecture: central bank issued tokens, open standards for acceptance, layered infrastructure for merchant/consumer PSPs. Projects that align with this approach (wallet providers, merchant integrations, cross-border settlement) may find strategic relevance.

4. Implications for the Crypto & Blockchain Ecosystem

The announcement of the digital euro has triggered debate across the crypto community. Critics argue that CBDCs are antithetical to the decentralised finance (DeFi) ethos: while blockchains emphasise permissionless access, decentralisation and user-custody, a CBDC is typically permissioned, centralised and potentially surveilled.

From the user’s lens: If you are seeking new crypto assets and revenue sources, the digital euro may not offer tokenomics of a typical crypto (e.g., capped supply, decentralised governance). However, it may open infrastructure opportunities — for example, wallet providers, payment service integrations, token-issuance platforms compatible with CBDC rails, or merchant solutions leveraging “digital euros”.

Furthermore, the push for digital euro is partly motivated by stablecoins and the threat they pose to monetary sovereignty: e.g., the ECB has warned that U.S.-dollar-linked stablecoins (~US$250 billion) may weaken euro-area policy control.

The crypto space may therefore view the digital euro as both a challenge (central bank competition) and an opportunity (new rails, new payment-token interplay). Projects that can bridge between digital-euro infrastructure and decentralized tokens might carve out niche utility.

5. Strategic and Business-Use Cases

For readers interested in practical blockchain use-cases and revenue opportunities, the digital euro initiative suggests a number of strategic angles:

- Wallet and infrastructure services: Non-custodial wallets, e-wallets or hybrid wallets that support both traditional crypto assets and the digital euro could provide users seamless switching between conventional tokens and CBDC-backed digital euros.

- Merchant and payment integrations: Merchants that accept the digital euro will have to integrate with EU acceptance standards. Payment providers or fintechs that build plug-ins, POS modules or e-commerce SDKs for the digital euro ecosystem could capture early-mover advantage.

- Token-ecosystem layering: Projects that issue utility tokens or stablecoins in Europe might consider compatibility or co-operation with digital euro rails (e.g., instant settlement, co-badging).

- Cross-border and financial-inclusion applications: As the digital euro aims to be inclusive (covering consumers without bank accounts, offline functionality) , blockchain-based remittances, micro-payments and mobile-first consumer use may align well with it, especially in emerging markets tied to Europe.

- Compliance, privacy and governance: Given regulatory scrutiny and design emphasised by the ECB (privacy, offline payments, holding-limits) , blockchain projects can specialise in bridging decentralised assets with regulatory-compliant CBDC ecosystems — offering audit trails, identity-management, and modular compliance.

6. Risks and Considerations for Crypto Investors

While the digital euro ecosystem opens opportunities, there are risks and important caveats:

- Centralisation vs decentralisation: The digital euro is centrally issued by the ECB and will operate within strict regulatory frameworks (e.g., holding-limits, mandatory acceptance) — this is divergent from typical decentralised token designs.

- Competition with existing crypto assets: CBDCs may occupy a payments-rail niche that could compete with stablecoins, limiting the growth of unbacked or loosely-backed payment tokens.

- Regulatory-leverage and surveillance concerns: Critics highlight privacy risks — although the ECB states offline payments will protect privacy (payer/recipient only) , user-behaviour, merchant-data and holding-limits may still be scrutinised.

- Technology and adoption risk: The digital euro is not yet live; its rollout depends on EU legislation in 2026, with pilot in 2027 and issuance in 2029 — until that occurs, uncertainty remains.

- Impact on banking/deposit flows: If users shift deposits from commercial banks to the CBDC, this may affect banking sector liquidity — banks are already raising concerns.

For investors seeking new crypto assets, it may be wise to view the digital euro not as a speculative asset itself (since it is a liability of central bank) but as an infrastructure catalyst — and look at adjacent opportunities (wallets, PSPs, token-rails that integrate CBDC and crypto).

7. What This Means Going Forward for Blockchain Projects

Given the direction of the digital euro, blockchain-projects and crypto entrepreneurs should consider the following actions:

- Monitor the legislative timeline: The regulation establishing the digital euro is expected in 2026, with pilot programmes from 2027. Projects that engage early (pilot integrations, PSP-partnerships) may gain advantage.

- Design for interoperability: Projects that enable smooth movement between crypto assets and digital euros (for example, token-swaps, wrapped digital euros, merchant acceptance) will have relevance.

- Focus on value-added services: Since the CBDC itself won’t have tokenomics for yield, projects should build value-added layers (loyalty programmes, merchant networks, micro-credit extensions) on top of the digital euro rails.

- Highlight compliance and privacy: Blockchain architectures that embed high privacy, offline-capability, and open-standard adaptability will align with the digital euro’s design goals (offline payments, inclusion).

- Don’t ignore global competition: The digital euro partly responds to stablecoins and non-European rails. Projects in Asia, Latin America or other jurisdictions may need to consider how CBDCs influence global token flows, settlement networks and regulatory models.

Conclusion

The digital euro represents a significant crossroads between traditional finance and digital-asset infrastructure. For readers who are exploring new crypto assets, income opportunities and practical blockchain applications, this project is not about “creating a crypto replacement” but about building a digital-money rail anchored by a central bank, yet embedded in a modern payments ecosystem.

While it does not replicate the decentralised, open-token design of many cryptocurrencies, the digital euro creates infrastructure demand for wallets, payment providers, merchant integrations, settlement layers and compliance-bridges. In the two-to-four-year horizon (2026 legislative approval → 2027 pilot → 2029 issuance) lies a window of opportunity to architect solutions that mesh crypto innovation with CBDC-readiness.

As always, with innovation comes risk: projects must reconcile centralised control with decentralised aspirations, regulatory mandate with token flexibility, and global competition with local sovereignty. But for those willing to build “at the intersection” of blockchain and central-bank digital currency, the digital euro offers a compelling strategic inflection point.