Main Points :

- The Nordic-region’s largest bank Nordea Bank is launching a synthetic Bitcoin exchange-traded product (ETP) in December 2025.

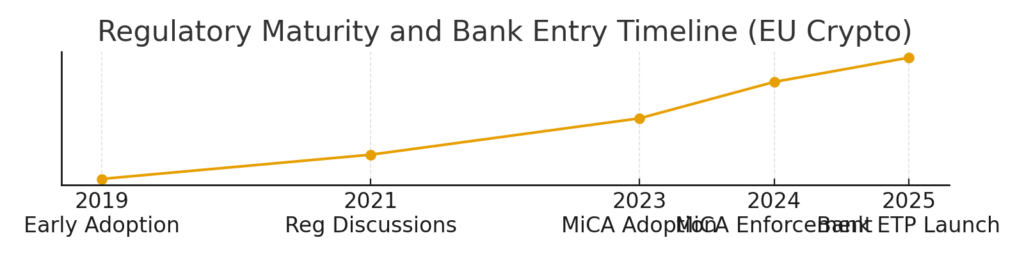

- The move is driven by the implementation of the Markets in Crypto‑Assets Regulation (MiCA) across the European Union, which came into full effect December 2024.

- The ETP is being issued by CoinShares International Limited and will be offered via an “execution-only” platform aimed at experienced investors.

- This development signals a further step in the institutionalisation of crypto assets in Europe, with potential knock-on effects for token adoption, asset flows, and blockchain-driven financial innovation.

- For new crypto-asset hunters and participants in the “Two-Extremes Model” of Asset-Backed Representation vs Autonomous Trust Tender, this event may mark a gateway: institutional access tools may drive greater on-chain real-world integration and secondary issuance opportunities.

I. Nordea’s Strategic Shift

In a striking pivot from its previous caution, Nordea Bank has announced that from December 2025 its clients will be able to gain exposure to Bitcoin through a synthetic exchange-traded product (ETP) provided on its platforms. Historically, Nordea defined crypto assets as unregulated and citing lack of investor protection refrained from offering such exposure. But now, citing both increasing institutional and retail demand across the Nordic region and the maturation of the regulatory landscape, the bank has opted to embrace crypto-linked investment tools.

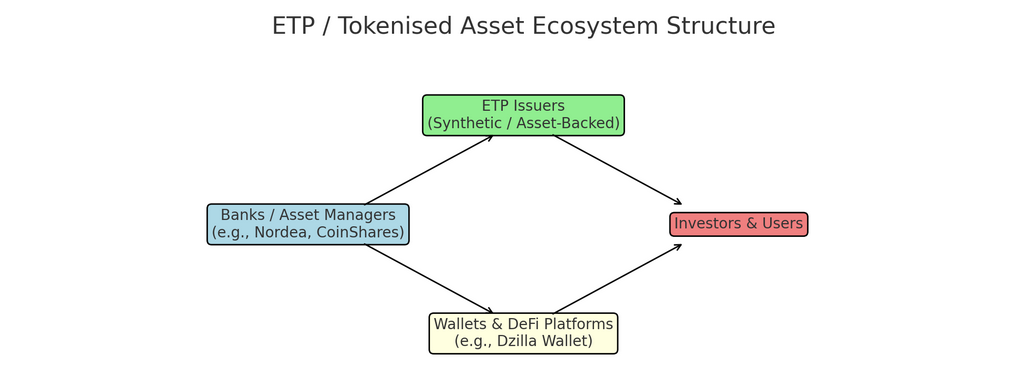

The product in question is issued by CoinShares International Limited — a leading digital-asset manager in Europe — and is structured as a synthetic ETP, meaning it offers Bitcoin price-exposure without requiring direct ownership or custody of the underlying asset.

Furthermore, Nordea will only offer this product in an “execution-only” format: the bank will provide the platform but no investment advice. The offering is targeted at experienced investors comfortable with alternative assets, reflecting a measured approach rather than full retail rollout.

From the viewpoint of blockchain practitioners and altcoin-seekers, this is meaningful: a major mainstream bank entering the space in a regulated way may catalyse the next wave of institutional infrastructure, liquidity, secondary products, and possibly tokenised derivatives or real-world asset bridges.

II. Regulatory Bedrock: MiCA and European Crypto Infrastructure

A key pillar of this development is the regulatory undertaking across the European Union known as MiCA (Markets in Crypto-Assets Regulation). Adopted in 2023, it became fully applicable from December 30 2024.

MiCA was introduced to bring legal clarity to crypto-assets, including security tokens, stablecoins and other digital assets, aiming to enhance investor protection, supervision of crypto-asset service providers (CASPs) and the integration of distributed-ledger technology into regulated financial markets.

In Nordea’s own statement, the bank explicitly referred to MiCA’s maturation of the regulatory environment as a pre-condition for its willingness to “offer products and services to meet our customers’ needs as the environment matures.”

What this means practically for crypto-asset builders and project teams:

- A clearer compliance roadmap in the EU potentially lowers institutional hesitation to partner with token issuers or service providers.

- Tokenised asset platforms, DeFi protocols interacting with regulated banks or ETP issuers may see new opportunities.

- For a wallet developer like your “dzilla Wallet”, integration with regulated banking or ETP flows could open pathways for asset-back representation implementations (your first extreme); conversely, the autonomous trust side (second extreme) may be supported by institutional rails gaining acceptance.

Moreover, while MiCA is specific to the EU, the signal effect globally is larger: when conservative institutions like Nordea pivot, we can expect contagion into other jurisdictions and possibly native token-issuance models that claim “MiCA-compliant” status or reference the EU standard.

III. Market Dynamics: Demand, Product Evolution and Strategic Implications

Several factors converge to make this moment noteworthy for crypto-asset strategists:

Rising demand for regulated crypto exposure

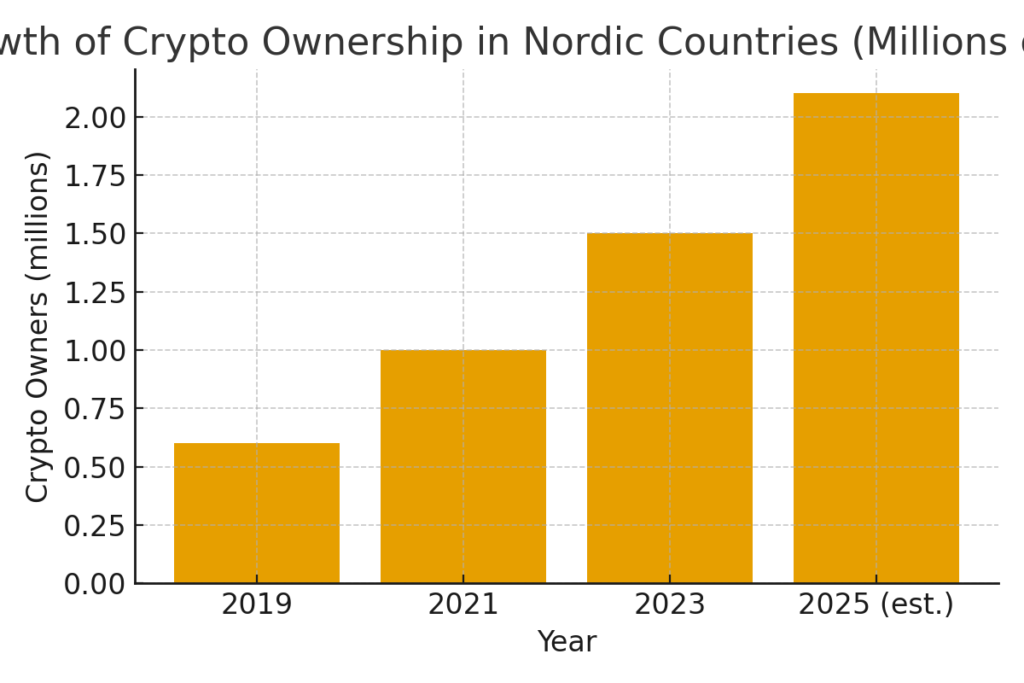

Nordea pointed to rising interest in cryptocurrency-related investment products across Nordic countries. For instance, a survey referenced by media showed that crypto ownership in the Nordic region (Denmark, Norway, Sweden, Finland) sits at around 2.1 million people out of a population of over 28 million, up from about 1.5 million the prior year.

The availability of ETPs offers a familiar traditional finance wrapper for crypto exposure, appealing to investors who may be wary of buying and storing crypto directly but are open to regulated financial instruments.

For new crypto-asset bettors, this means:

- Increased liquidity and institutional back-stop may lead to tighter spreads and deeper markets in major tokens like Bitcoin (BTC) and Ethereum (ETH) via derivatives.

- The introduction of bank-offered ETPs may catalyse tokenised products, secondary issuance, staking derivatives, and co-investment platforms.

Strategic evolution of product architecture

The synthetic nature of the ETP means that Nordea is offering exposure to Bitcoin’s price without providing custody of the underlying asset. This has pros and cons:

- Pro: For the bank and issuer this reduces operational risk, custody risk and regulatory fallout from direct crypto holdings.

- Con: For the end-investor, counter-party risk and structure risk increase; the wrapper may not perfectly mirror on-chain dynamics or allow direct protocol participation (e.g., staking, DeFi).

From the viewpoint of an innovator in Web3, this underscores that the first wave of institutional crypto is still anchored in traditional finance frameworks, not fully Web3-native models. But as acceptance rises, second-wave models (tokenised funds, decentralised ETPs, real-world asset bridges) may proliferate.

Implications for institutional and retail flows

Nordea’s decision is a signal: traditional banking institutions are now prepared to embed crypto exposures in regulated products. This could trigger:

- A rise in institutional allocations to digital assets (previously constrained by custody, regulation, reputational risk).

- Enhanced infrastructure investments (custody, tokenisation platforms, compliance tooling) to serve this demand.

- A potentially positive feedback loop: more bank-driven crypto products → more retail/institutional comfort → more protocols build trust-enabled services (e.g., custody + DeFi integration).

For your interests (new assets and practical blockchain use): this can translate into: - Protocols designing token models that anticipate institutional wrappers.

- Wallets or platforms that offer “institution-grade” rails but on a user-friendly front-end (thus bridging decentralised native users and regulated users).

- Creative token issuance models that leverage bank ETP access to underpin token liquidity or provide bridging between asset-backed representation and autonomous trust tender.

IV. Opportunities & Cautions for Crypto-Asset Hunters and Practitioners

Given this backdrop, what are the opportunities and what should you watch out for?

Opportunities

- Token Issuance & Secondary Markets

With banks and asset managers offering exposure via traditional products, token issuers may find new channels or partnerships with such ETP/ETC issuers. This could facilitate secondary listings, tokenised funds or security-token offerings (STOs). - Integration into Institutional Infrastructure

Projects that can position themselves for institutional readiness — e.g., audited smart-contracts, compliance-friendly KYC/AML flows, custody integrations — may have a competitive edge. Your wallet development (dzilla Wallet) may benefit by offering features that cater both to decentralised users and institutional-adjacent segments. - Bridging Two Extremes of Finance

Your “Two-Extremes Model” (Asset-Backed Representation vs Autonomous Trust Tender) becomes more relevant:- Asset-Backed Representation: Tokenised real-world assets, protocols working with banks or asset managers, regulated products (like this ETP) become enablers.

- Autonomous Trust Tender: As institutional exposure normalises, there may be room for truly decentralised trust models to leverage that infrastructure (liquidity pools, tokenised funds, programmable finance).

- Increasing Crypto Adoption & Product Complexity

Product complexity is increasing: beyond spot tokens, ETPs, synthetic products, tokenised funds etc. This creates niches for specialised altcoins, DeFi protocols, staking platforms, tokenised real-world asset (RWA) frameworks. Innovators in complementary sectors (wallets, DeFi tooling, compliance APIs) could capture organic growth.

Cautions

- Structure Risk & Counterparty Risk

The synthetic ETP doesn’t imply direct crypto custody; risks include issuer default, tracking error, regulatory shifts, or product discontinuation. Investors expecting direct on-chain participation need to be aware of limitations. - Regulatory Complexity Remains

While MiCA offers a framework in the EU, territories outside the EU may not have the same clarity. Also national regulators may still impose varying rules; compliance burdens may increase for protocols and service providers.

For instance, while 19 % of EU financial institutions offered crypto services by early 2025, the number was still relatively low, indicating that institutional adoption is far from ubiquitous. - Innovation vs Regulation Trade-Off

There is a broader industry concern that heavy regulation may slow innovation. Some Web3 advocates argue that compliance burdens, licensing costs and regulatory oversight risk constraining agility. For builders focused on autonomy, this tension must be managed. - Token Value & Market Timing

Institutional entry is positive, but timing and market context still matter: token price, macro conditions, regulatory chatter and liquidity remain variables. New asset seekers must perform discipline: tokenomics, protocol fundamentals, regulatory fit, market positioning.

V. What This Means for Wallet-Builders & DeFi Practitioners

Since you’re developing a non-custodial wallet (“dzilla Wallet”) and are interested in practical blockchain integrations (e.g., BTC-to-ETH swaps, bridging, UX transparency), how might this bank-ETP development matter?

- Institutional Back-end Meets User-Front-End: The fact that a major bank offers a crypto exposure product means users will increasingly expect seamless, regulated-grade experiences. Your wallet can differentiate by offering auditability, transparency, modular compliance features, swap flows that align with institutional rails.

- Tokenised Asset Support & ETP Connectivity: If tokens or structured products issued by banks become more common, wallets might need to support tokenised ETPs, synthetic assets, or tokenised equivalents. Designing wallet features anticipating such assets (custom asset type, regulatory metadata, secondary market access) could yield first-mover advantage.

- Bridging On-Chain DeFi and Off-Chain Finance: Your interest in a “Two-Extremes Model” is validated here: one extreme (asset-backed) is integrating with banks/asset managers; the other extreme remains purely on-chain autonomous trust. A wallet that supports both models — e.g., user holds tokenised real-world asset representation parts while also participating in DeFi native flows — could appeal to hybrid users.

- Compliance-Friendly UX Without Custody: Non-custodial wallets are inherently more decentralised; yet as institutionalisation grows, UX demands may include KYC/AML, transaction monitoring, sanctions screening etc (especially if users deal with tokenised bank products). Incorporating compliant modules (optional but available) may position your wallet for both retail and institutional friendly use cases.

- Tokenism & Infrastructure Expansion: More institutional adoption may drive incremental infrastructure: advanced custody, staking services, tokenised products, liquidity pools. Wallets that integrate with those services via APIs, SDKs or protocol support can leverage the growth wave.

VI. Broader Industry Implications & Trend-Spotting

Beyond Nordea and this particular ETP, this event reflects and may accelerate several broader trends in the crypto/blockchain industry:

- Mainstream Financial Institutions Entering Crypto in an Accredited Way: The move by Nordea is part of a wave of banks, exchanges and asset managers entering crypto services, custody and tokenised asset products.

- Tokenised Real-World Assets (RWA) Gain Traction: As banks and financial institutions embrace tokenised exposures, the path for RWAs (real estate, commodities, private equity) on-chain becomes more credible.

- Regulation as a Catalyst, Not a Barrier: While regulation is often seen as a headwind, for many institutional actors, regulation (like MiCA) is the green light. It signals a safe environment, enabling risk-averse institutions to enter.

- Layering of Financial Products on Crypto Base: As the crypto infrastructure matures, more complex financial products — ETPs, structured tokens, synthetic derivatives — are layered on top of basic spot token markets. This leads to new entrants and new token usage models.

- Hybrid Finance Model Gains Legitimacy: Your conceptual “Two-Extremes Model” finds real-world backing: asset-backed representation (banks issuing tokenised exposure) and autonomous trust tender (pure decentralised tokens and protocols) both advancing, and potentially converging via hybrid architectures (regulated tokens but on-chain settlement, or decentralised apps leveraging bank-issued token rails).

Conclusion

The announcement by Nordea Bank to offer a Bitcoin-linked synthetic ETP beginning December 2025 marks a significant inflection point in the evolution of crypto assets from niche speculative instruments to mainstream financial exposures. Underpinned by the EU’s MiCA regulatory regime, this step reflects how regulatory maturation can unlock institutional participation, deepen liquidity, and expand the architecture of tokenised finance.

For those seeking new crypto assets, revenue opportunities or practical blockchain applications, this development offers both an arrow pointing to where the market is heading and a set of frameworks to build around. Wallet builders, token issuers, DeFi practitioners and hybrid-finance innovators should take note: the institutional bridges are now being built, and the convergence of regulated finance and decentralised infrastructure is accelerating.

In your context—developing the dzilla Wallet, implementing BTC-to-ETH swaps, focusing on user transparency and bridging two extremes of finance—this moment is an opportunity. The “asset-backed representation” side is reinforced by bank-issued ETPs; the “autonomous trust tender” side remains fertile for on-chain innovation enhanced by institutional rails. By designing for both, you position for relevance in an ecosystem that is evolving, not just in token price but in structure, regulation and user demand.

In short: the door to institutional-grade crypto infrastructure is opening wider. The next phase isn’t just about token price moves—it’s about token access, regulated wrapping, infrastructure integration and real-world application. For builders and asset-seekers alike, the time to align strategy with this shift is now.