Main Points :

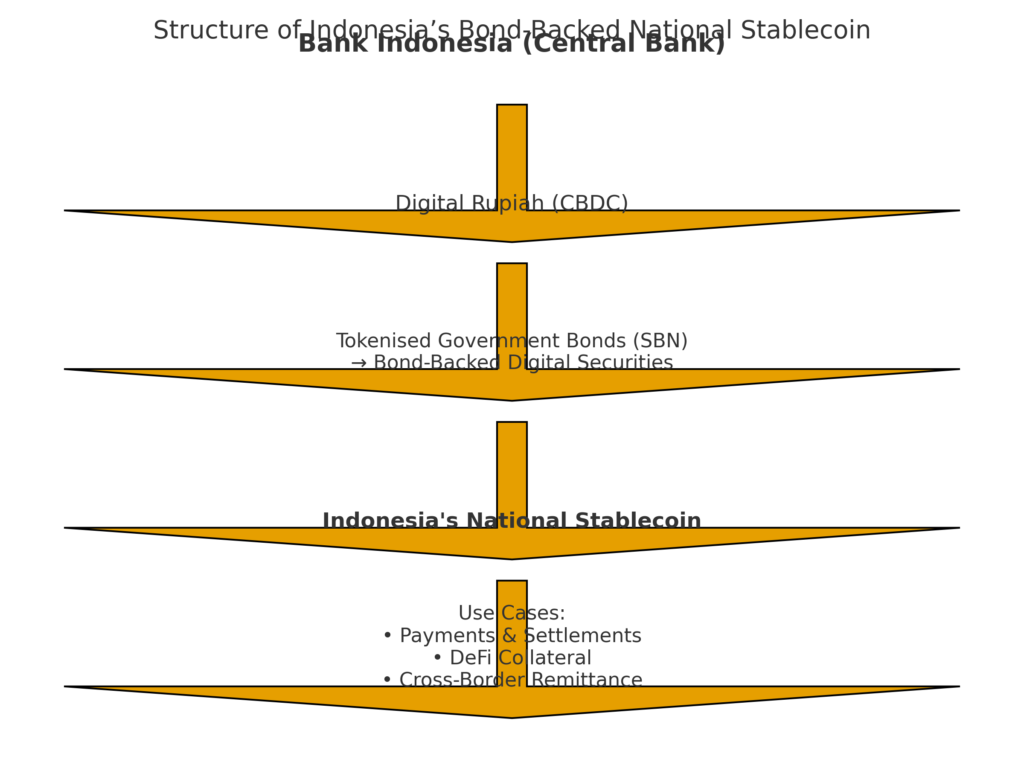

- Bank Indonesia (BI) plans to issue a national “stablecoin version” backed by government bonds (SBN) and underpinned by the digital rupiah (the CBDC).

- The new digital securities/tokenised bonds will be issued in digital form by BI, as part of its digital-finance strategy and integration of blockchain into monetary infrastructure.

- Although stablecoins are not yet legal tender in Indonesia, the regulator Otoritas Jasa Keuangan (OJK) is actively monitoring their use, imposing AML requirements and reporting obligations on stablecoin issuers/traders.

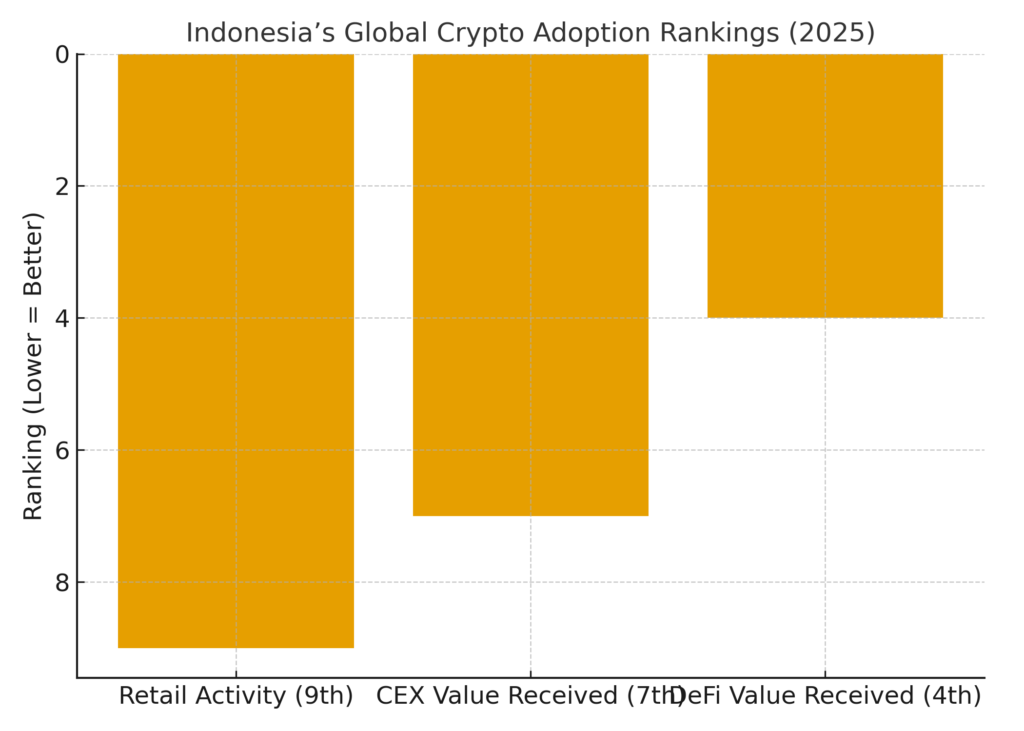

- Indonesia ranks high in global crypto/DeFi adoption (7th in the 2025 Global Crypto Adoption Index), giving a favourable backdrop for such initiatives.

- For investors and blockchain practitioners, this opens potential opportunities around tokenisation, sovereign-backed digital assets, and the merging of traditional finance with Web3 flows.

1. Background: Why Indonesia is launching this initiative

In recent years, Indonesia has taken significant steps to modernise its monetary and digital-finance infrastructure. Under the omnibus Law No. 4 of 2023 on Financial Sector Development and Strengthening, the digital rupiah (a CBDC) has been introduced as a legal form of currency alongside physical banknotes and coins. At the same time, the rupiah currency has faced pressure and the digital-asset space has been growing rapidly in Indonesia — prompting BI to respond strategically.

At the Indonesia Digital Finance & Economy Festival and Fintech Summit 2025 in Jakarta, BI Governor Perry Warjiyo announced the concept of issuing “digital securities” — tokenised government bonds (SBN) backed by the digital rupiah — and labelled them as “Indonesia’s national version of a stablecoin”.

This design reflects three strategic goals: (1) strengthening the monetary sovereignty and credibility of the rupiah; (2) leveraging blockchain / tokenisation technology to modernise financial markets; and (3) positioning Indonesia as a regional leader in digital finance by combining traditional public-finance instruments with digital asset mechanics.

2. What exactly is being proposed?

The structure is multi-layered:

- BI will issue digital central-bank securities — these are tokenised versions of the existing government bonds (SBN: Surat Berharga Negara) on a blockchain or DLT infrastructure.

- These digital securities will be backed by the digital rupiah (the CBDC issued by BI), meaning the stablecoin-analogue will derive its value and backing from the central bank currency.

- BI refers to this product as “the digital rupiah with underlying SBN, Indonesia’s national version of a stablecoin”.

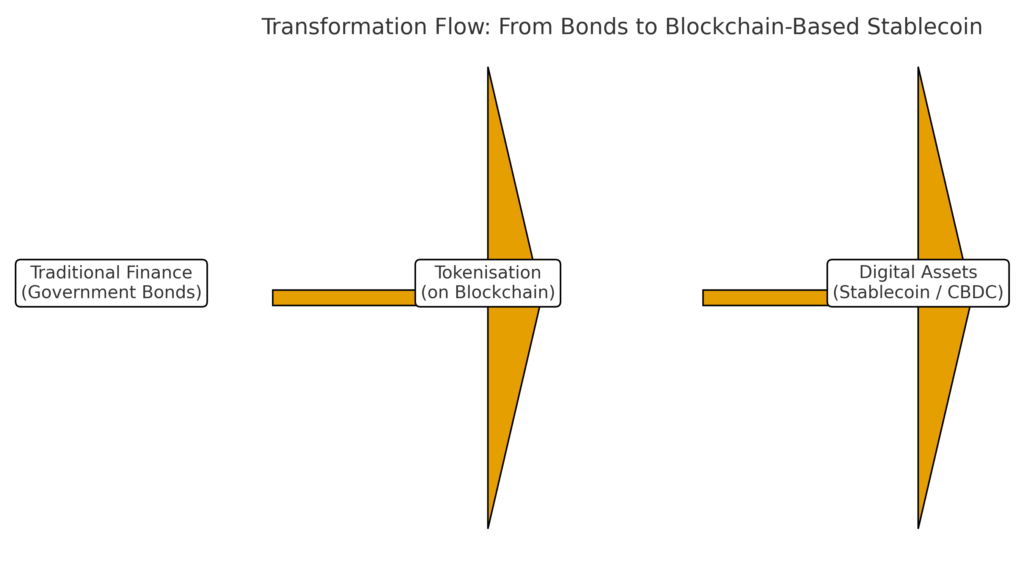

- The stablecoin concept isn’t simply a private stablecoin pegged to fiat; rather it is a sovereign digital instrument combining CBDC + tokenised sovereign bonds, designed for efficiency, transparency, and stability.

- Although detailed rollout timelines, technical frameworks or network designs have not yet been fully published, this initiative clearly signals that BI hopes to integrate blockchain-based tokenisation into its monetary and market infrastructure.

For a blockchain practitioner or crypto-asset hunter, this offers intriguing implications:

- A new class of tokenised sovereign digital securities might surface, potentially tradable (or at least interoperable) in digital-asset environments.

- The underlying backing by government bonds may provide lower volatility and higher trust compared to typical privately issued stablecoins.

- Infrastructure developments (CBDC + tokenised securities) may create ecosystem opportunities: e.g., wallets, token-issuance platforms, cross-border payment rails, DeFi overlays anchored on sovereign digital assets.

3. Regulatory and market context

While stablecoins are not yet recognised as legal tender in Indonesia, regulatory oversight is strengthening. The OJK has mandated that stable-coin issuers/traders be subject to AML/KYC, periodic reporting, and inclusion under exchange-monitoring systems.

Governor Warjiyo’s remarks come amid a broader context: Indonesia was ranked 7th in the 2025 Global Crypto Adoption Index (by Chainalysis). It placed 9th in retail crypto activity, 7th in value received by centralised services, and 4th in DeFi value received.

Thus, the digital-asset ecosystem in Indonesia is relatively advanced (by emerging-market standards) and the timing is opportune for a sovereign digital initiative. That said, for implementation the project will face challenges such as:

- Ensuring technological infrastructure (DLT, permissioned/consortium networks, security) is robust and scalable.

- Achieving interoperability with existing payment systems and cross-border rails.

- Gaining public/business adoption: stablecoin usage must go beyond novelty and integrate into payments, remittances, settlement services.

- Managing legal/structural risk: issuing tokenised bonds + CBDC implies regulatory frameworks must be clear, supervisory mechanisms in place, and investor protections enforced.

4. Implications for crypto investors and blockchain practitioners

Given your interest in new crypto assets, income opportunities and practical blockchain use cases, several angles stand out:

a) Tokenised sovereign digital assets as investment/utility infrastructure

If Indonesia issues a bond-backed digital stablecoin, it may spawn ecosystem tools: wallets, platforms offering access to tokenised bonds, DeFi protocols utilising sovereign-backed collateral. The existence of a sovereign-backed instrument could become a “safe-asset” anchor within a broader digital-asset portfolio.

b) Enhanced bridge between traditional finance and blockchain

This initiative may accelerate tokenisation of real-world assets (government bonds → digital securities) in Indonesia, meaning increased demand for smart-contract infrastructure, regulated token-issuance markets, secondary trading platforms. Blockchain developers (especially in Node.js/web3.js as per your preference) could target building wallet modules, SDKs, integrations for sovereign digital assets.

c) Stablecoins + CBDCs as settlement/rail options for decentralized finance

Sovereign-backed digital ruble/rupee-type constructs may serve as low-volatility collateral or settlement rails in DeFi ecosystems. For example: a tokenised bond-backed stablecoin could be used as stable collateral in Indonesian DeFi platforms, reducing exposure to major global stablecoin risks.

d) Geopolitical/regional finance layering

As Indonesia moves in this direction, regional cross-border digital-asset flows may increase (ASEAN payments, intra-Asia remittances). For an asset-defender/investor viewpoint, this suggests the growing importance of regional stablecoins and CBDCs — diversifying away from USD-based assets and exploring southeast-Asia-centric rails.

5. Recent trends and what to watch

- Other Asian jurisdictions (e.g., China’s digital yuan, Hong Kong’s digital HKD explorations) are also advancing sovereign stablecoin/CBDC efforts, meaning regional competition and collaboration will increase.

- Indonesia’s currency pressure (rupiah) and macro-financial backdrop (inflation, FX volatility) provide strong impetus for a sovereign-backed stablecoin.

- Regulatory frameworks are advancing: the role of OJK is expanding, and tokenisation of government securities is being reviewed actively. This is good for transparency and risk-mitigation, which matter for institutional players.

- For blockchain practitioners: expect the release of technical frameworks, consortium networks, sandbox regulations, pilot programs in 2025-26 as BI moves from proof-of-concept toward rollout.

- From an investment standpoint: monitoring issuance conditions, backing ratio, secondary-market liquidity, redemption mechanisms, asset-eligibility of the stablecoin/ tokenised bonds will be key.

6. What this means for your strategy

Given your focus on new crypto assets, income opportunities and blockchain application use-cases:

- Asset scouting: Keep an eye on token-issuance platforms/IDOs in Indonesia that might tap into this sovereign initiative — e.g., platforms issuing digital-bond tokens, wallets onboarding digital rupiah stablecoins.

- Infrastructure development: With your JavaScript/web3.js preference, you might consider building SDKs or modules for Indonesian-market wallets, tokenised sovereign bond integration, or cross-border payments using the digital rupiah stablecoin.

- Yield/risk perspective: The emergence of a sovereign-backed digital asset may provide new yield opportunities (e.g., bond token interest, staking of digital bonds) though one must assess regulatory, counterparty and tech risks carefully.

- Diversification: As sovereign digital assets proliferate, you may consider reducing exposure solely to USD-based stablecoins and major L1 tokens, and instead include regionally-anchored digital assets (e.g., Indonesia, ASEAN) that offer different risk/return profiles.

- Use-case integration: Beyond investment, consider practical blockchain ties: e.g., programmable payment flows using the stablecoin, remittance solutions for Indonesian-Philippines corridors, integration into DeFi platforms with lower-volatility collateral.

Conclusion

The plan by Bank Indonesia to issue a government bond-backed digital stablecoin anchored on the digital rupiah marks a significant evolution in the blending of traditional finance with blockchain innovation. For investors seeking new crypto assets and practitioners building blockchain applications, this development opens a frontier of opportunity: tokenised sovereign assets, regional digital-currency rails, and new infrastructure stacks. That said, implementation will require robust technology, clear regulation, public adoption and secondary-market ecosystems. In the meantime, staying attuned to the technical frameworks, pilot programs and regulatory signals will position you ahead of the curve. Indonesia’s move may not only reshape its own financial architecture, but also signal a broader shift in how emerging economies deploy digital finance — making this an important development for any serious blockchain-asset strategist.