Main Points :

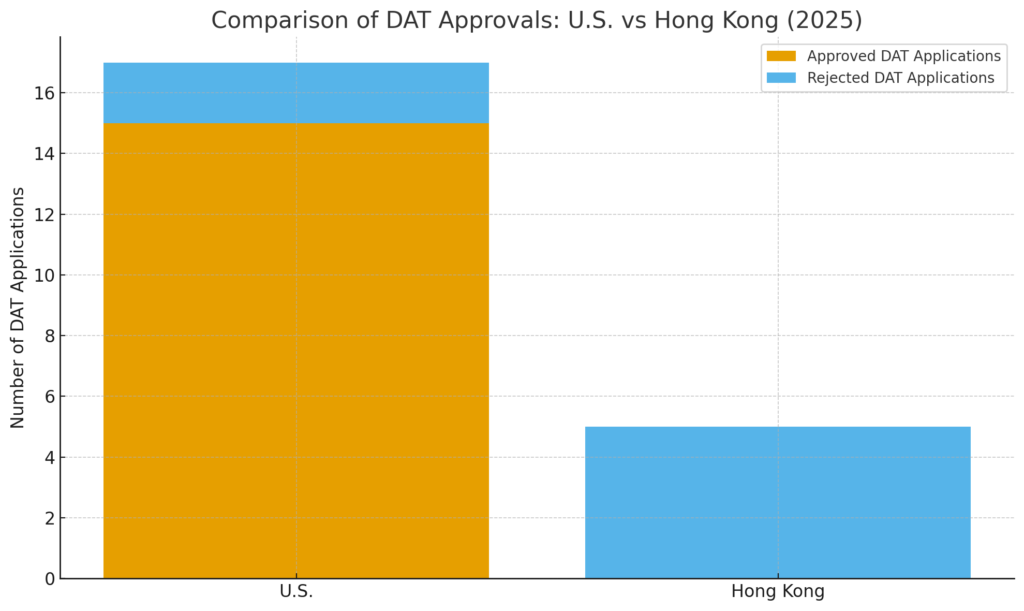

- The Securities and Futures Commission (SFC) of Hong Kong has rejected at least five applications from listed companies seeking to adopt a “Digital Asset Treasury” (DAT) model, i.e., holding cryptocurrencies on the corporate balance sheet.

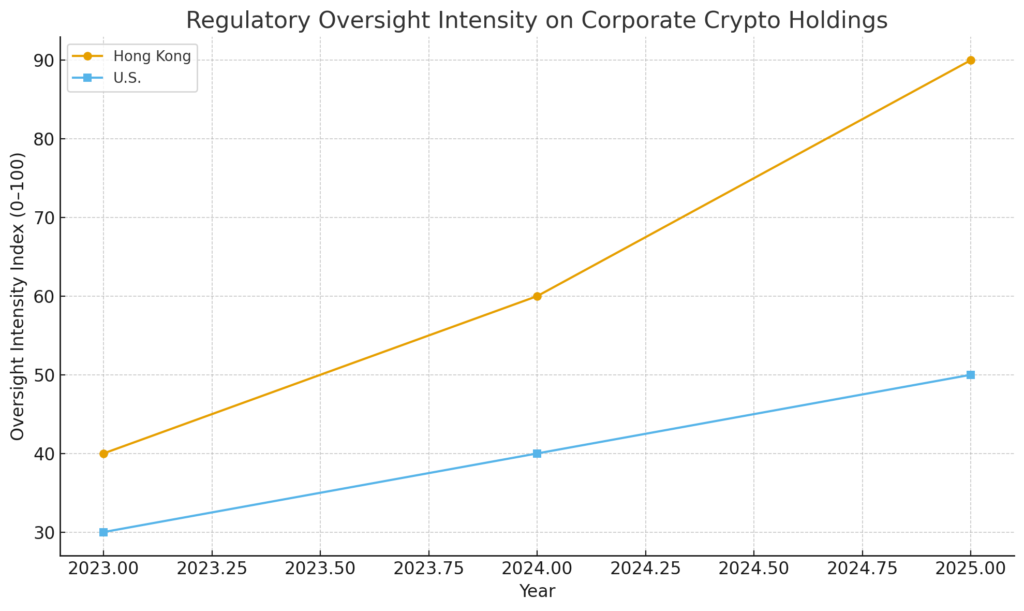

- Hong Kong currently lacks a formal regulatory statute governing listed companies’ involvement in crypto‐treasury strategies; the SFC is now stepping up oversight, investor education, and possible guidance development.

- The regulatory concern centres on valuation risk: some companies in the U.S. deploying DAT models have seen their market capitalisation exceed more than double the cost of their crypto holdings, creating potential bubble risks.

- For crypto investors and blockchain practitioners seeking new assets or treasury strategies, Hong Kong’s stance suggests heightened caution and differentiated opportunities: crypto treasury plays may be less feasible in Hong Kong while other jurisdictions evolve.

- From a practical blockchain/crypto operations perspective, institutional treasury adoption (stablecoins, holdings, risk management) must factor in regulatory alignment, governance, liquidity and volatility risks — Hong Kong’s move underscores that.

1. Regulatory backdrop: why Hong Kong is tightening

In recent weeks the SFC has made clear that listing applications by companies wishing to pivot into a crypto treasury model will be subject to elevated scrutiny. According to media reports, at least five companies seeking to convert their corporate model towards a DAT structure were rejected by the Hong Kong Exchanges and Clearing Limited (HKEX) in cooperation with the SFC.

The core impetus stems from concerns that retail investors may not fully understand the risks involved in crypto‐treasury strategies, including high volatility of underlying assets, uncertain liquidity, and the possibility that corporate valuations become detached from tangible business models.

Moreover, Hong Kong lacks a legislative framework specifically regulating listed companies’ crypto‐treasury business—SFC Chairman Kelvin Wong Tin‑yau has openly stated that “there is currently no regulation in Hong Kong that governs listed companies’ participation in cryptocurrency investment”.

This regulatory gap has elevated the supervisory role of the SFC: monitoring market developments, investor education efforts, and considering whether formal guidance or regulation is required.

From the vantage of blockchain‐finance practitioners and asset hunters, this move signals that Hong Kong is adopting a cautious posture with respect to corporate crypto exposure—even while other jurisdictions may be warming. It reminds us that treasury strategies involving digital assets are not universally “open” and depend heavily on local regulatory context.

2. The mechanics and risks of the DAT model

The concept of a Digital Asset Treasury (DAT) refers to companies holding cryptocurrencies (e.g., Bitcoin, Ethereum) on their balance sheets as part of treasury management — either because they believe in long-term appreciation or for corporate liquidity/hedge purposes. This model has gained traction especially in the U.S., with some firms noting substantial appreciation of crypto holdings and associated stock‐market “premium”.

However, the risks are significant: crypto asset volatility can destabilise corporate cash-flow and balance‐sheet metrics; valuations of such companies can decouple from intrinsic business operations and instead become proxies for crypto speculation; and the “market‐to‐net‐asset value” (mNAV) discount or premium may swing widely.

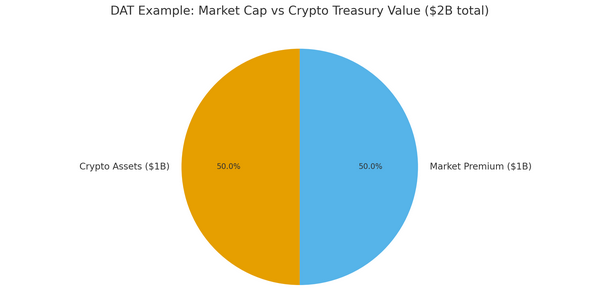

For example, Chairman Wong referenced data indicating that when a company purchases, say, $1 billion of cryptocurrencies, the resulting stock price and market capitalisation may exceed $2 billion — more than double the cost of holdings — raising questions of sustainability and risk.

In many jurisdictions the accounting, liquidity, governance, disclosure and taxonomy issues around DATs remain immature. For blockchain practitioners designing treasury strategies (for example in a non-custodial wallet, stablecoin holding, token issuance or project treasury setup) these are key dimensions: how does the entity guard against shocks, how is the asset treated (liquid vs illiquid), what is the governance framework, how is investor/distributor risk managed? Hong Kong’s tightening underscores that these models cannot be assumed to be straightforward.

3. Implications for crypto asset hunters and blockchain practitioners

a) For new crypto‐asset investors

The regulatory warnings act as an important signal. If companies in Hong Kong cannot easily pivot to DATs, then pure exposure via corporate proxy may become less available in that jurisdiction. This may push investors to look for jurisdictions more permissive (subject to risk) or to directly hold digital assets rather than rely on corporate wrappers.

Additionally, the valuation risk flagged (premium over underlying crypto holdings) suggests that some listed companies using DAT models may become speculative proxies — and those often carry higher risk. Therefore, when spotting a “treasury company” model, examine whether the premium (share price vs net crypto value) is justified, and evaluate governance, liquidity, disclosure.

b) For blockchain/tokens/treasury design

For practitioners building treasury systems (such as the user’s interest in wallet design, non‐custodial swaps, stablecoins, or token ecosystems) the regulatory dimension is now even more material. Suppose a wallet integrates corporate treasury-style holdings of crypto, or a project’s token treasury is large and invested in crypto assets — the design must incorporate:

- Clear governance and disclosure chains (who reviews the treasury, how are decisions made)

- Liquidity management: crypto holdings may be illiquid, volatile; protocols must plan for drawdowns

- Regulatory fit: in jurisdictions like Hong Kong, holding crypto as a corporate treasury may trigger scrutiny or outright rejection; choosing where to domicile asset-holding vehicles matters

- Investor education: if a project markets itself as holding crypto assets as treasury, then downstream token-holders or users may need transparency and risk awareness (mirroring what SFC emphasises for retail investors)

In short, the Hong Kong example emphasises that token/treasury design must not only focus on blockchain technicalities but also on regulatory and investor‐protection architecture.

4. Recent Related Developments and How the Landscape Is Evolving

Beyond the immediate Hong Kong story, a few adjacent movements are worth noting:

- In the U.S., several firms continue to adopt DAT‐like models (holding large crypto reserves) and many projects replicate that model, underscoring regional divergence in regulatory attitudes.

- Separate but related: jurisdictions are increasingly examining how listed firms invest in crypto or real-world‐asset (RWA) tokenisation; for instance, China’s China Securities Regulatory Commission (CSRC) recently advised some brokerages to pause RWA tokenisation business in Hong Kong, signalling regional regulatory calibration.

- Hong Kong’s own licensing of crypto trading venues continues: it recently approved additional exchanges, suggesting that while Hong Kong remains crypto-active, it prefers to shape the ecosystem via licensing rather than corporate treasury liberalisation.

From the vantage of new assets, this signals that: treasury models will be differentiated, regulatory arbitrage may become a strategic lever (but also a risk), and token/asset design must anticipate jurisdictional differences. Projects that can show strong governance, clarity of asset backing, transparent treasury operations may gain advantage when regulators tighten scrutiny.

5. Strategic Takeaways for Action

- Due diligence is critical: If you are hunting new crypto assets, and you encounter entities that use corporate treasury holdings of crypto, dig into the premium vs net asset value, disclosure, governance, liquidity, and the jurisdictional regulatory environment.

- Jurisdiction matters: Holding large crypto assets as a treasury in Hong Kong is currently fraught; other jurisdictions may be more permissive, but that may come with higher regulatory risk. Factor location into your design or investment thesis.

- Treasury architecture matters: Whether you are building a wallet, project, token ecosystem or treasury management structure, ensure you embed governance, risk controls (volatility, liquidation, custodial risk), and investor education / disclosure.

- Transparency wins: Regulators emphasise investor education and transparency; blockchain projects that proactively demonstrate how treasury assets are managed, how risk is controlled, and how disclosures are made will have advantage.

- Monitor regulatory signals: The fact that the SFC openly flagged valuations, lack of regulation, and rejected conversions is a signal that regulators may introduce formal guidance — projects and investors should monitor developments closely.

Conclusion

Hong Kong’s regulatory posture toward corporate crypto treasuries provides a timely cautionary tale for anyone seeking to deploy digital-asset holdings at scale — whether as an investor seeking new revenue sources, as a blockchain practitioner designing treasury systems or token ecosystems, or as a company exploring strategic crypto exposure. The key take-aways: regulatory clarity (or lack thereof) can dominate treasury strategy viability; valuation dynamics around crypto holdings can introduce outsized risk; and operational details (liquidity, governance, disclosure) cannot be an afterthought. For those hunting the next crypto asset, the differentiator may no longer be purely “what token” but also “how the asset is held, governed, disclosed and regulated”.