Key Points :

- The global market for tokenized real-world assets (RWAs) is projected to surge, with forecasts from Standard Chartered and partners pointing to tens of trillions of dollars over the coming decade.

- Tokenization is moving beyond stablecoins into private credit, securitized debt, private equity, and illiquid assets — offering new yield and access opportunities for crypto-savvy investors.

- Although the current non-stablecoin RWA market remains modest (around US$ 20-30 billion), growth is accelerating rapidly.

- A key enabler is the combination of DeFi rails and improved token issuance/settlement infrastructure; the biggest risk is regulatory uncertainty.

- For those exploring new crypto assets and revenue streams, RWA tokenization presents a practical blockchain use-case bridging TradFi and DeFi, but liquidity, custody, compliance and real-world settlement frameworks still demand attention.

1. The Big Picture: A Multitrillion-Dollar Tokenization Wave

In a recent report, Standard Chartered and its partners highlight that the tokenization of real-world assets — that is, the digital representation on a blockchain of assets such as money-market funds, U.S. stocks, funds, commodities, private debt, and real estate — is poised to enter a phase of exponential growth. For example, the bank estimates the tokenized RWA market beyond stablecoins could expand markedly in the next few years.

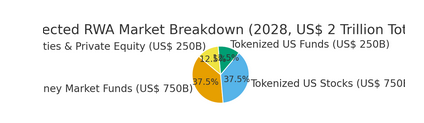

Although earlier figures (from the Japanese article you provided) cited a US$ 2 trillion market by 2028, more recent iterations of the analysis indicate a longer-term horizon: for instance, an estimate of US$ 30.1 trillion by 2034.

From the standpoint of someone looking for new crypto-related revenue opportunities, this suggests that tokenization of real‐world assets is not purely speculative but could become a mainstream locomotive in financial infrastructure.

Importantly, the projection from low billions today to trillions tomorrow signals a structural shift rather than a fleeting trend.

2. From Stablecoins to Private Markets: The Shift in Focus

Historically, the on-chain asset space has been dominated by stablecoins, which now count supply in excess of US$ 300 billion.

The report emphasizes that tokenizing assets merely for novelty is not sufficient; real value comes when tokenization yields cost, settlement, liquidity or access advantages vis-à-vis traditional off-chain equivalents.

Thus, Standard Chartered sees the next growth frontier in tokenizing private markets and illiquid assets: private credit, securitized debt, private equity, real estate and commodities. These classes often suffer from high entry barriers, limited liquidity and structural inefficiencies.

For the crypto-investor seeking new income streams, this translates into possibilities: on-chain debt instruments, fractionalized private equity tokens, token-enabled yield products tied to real-world assets.

3. Current Market State: Small But Rapidly Expanding

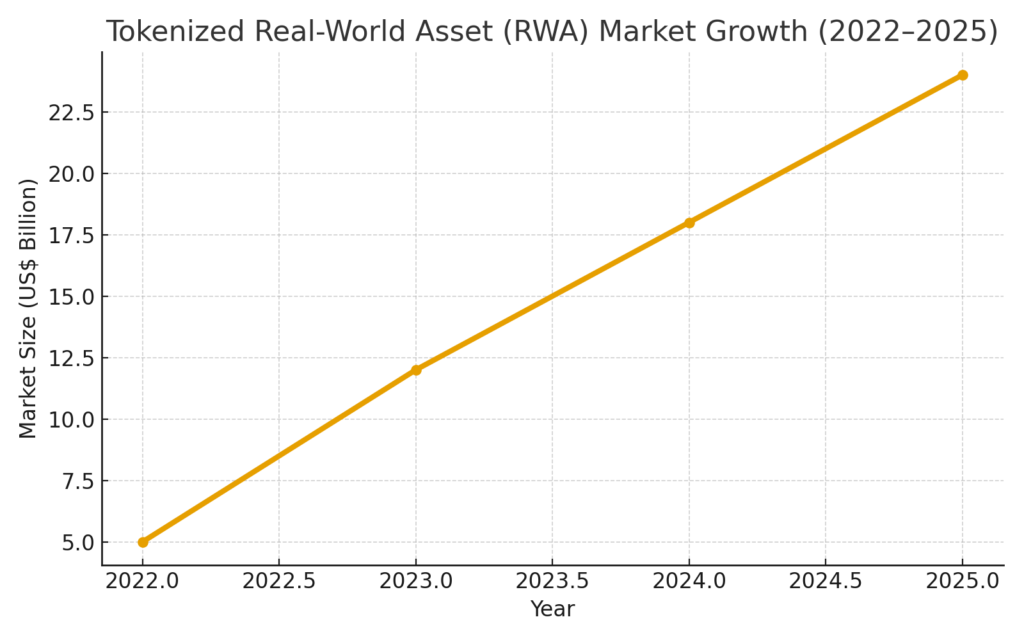

Despite the lofty forecasts, actual tokenized RWA volumes (excluding stablecoins) remain modest. For example, non-stablecoin RWA is estimated around US$ 23 billion as of mid-2025.

This means the market remains very early — but given historic growth rates (for example ~85 % year-over-year in tokenized RWA units according to one estimate) there is potential upside for early‐mover crypto players.

(Insert Chart: Growth of non-stablecoin RWA market from ~US$ 5 billion in 2022 to ~US$ 24 billion in 2025)

— “Tokenized RWA market size (US$ billion) 2022–2025”

Thus, for those scouting new crypto investment opportunities, the tokenization sector remains under-penetrated relative to its future potential.

4. Practical Use Cases and What’s Driving Adoption

Several factors drive tokenization’s appeal: fractional ownership, 24/7 settlement potential, global investor access, reduced counter-party/trust friction, programmability via smart contracts.

One clear use-case example: tokenized money-market funds — e.g., a tokenised version of a U.S. Treasury fund (such as the BUIDL fund by BlackRock launched in March 2024 — are being used in crypto collateral management.

Another example: a tokenised oil & gas capital stack in Latin America valued at US$ 75 million was recently executed, underlining how real-world asset deals are starting to transpire on‐chain.

For blockchain practitioners or crypto-developers (such as yourself developing wallet infrastructure), these trends signal a convergence: DeFi rails begin to host real-world yield-bearing assets, meaning workflows such as BTC→ETH (or other chain swaps) may increasingly interface with RWA-backed tokens. This opens practical implementation scenarios for your wallet project (“dzilla Wallet”) where RWA tokens could be integrated as on-chain assets.

5. The Big Risks: Regulatory, Liquidity and Infrastructure Gaps

Despite all the promise, the tokenized RWA domain has important hurdles. Standard Chartered points to regulatory uncertainty as the largest single risk: inconsistent global regimes, unclear KYC/AML frameworks, fragmented regulation across jurisdictions.

Another critical issue: liquidity — while tokenization promises tradability, many tokenised assets remain illiquid, have limited secondary markets, and may not benefit from the same market-making infrastructure as traditional markets. (See academic paper on liquidity challenges in RWAs).

Third, for crypto investors and wallet developers alike: custody, asset-attestation, smart-contract risk, oracle risk, settlement risk — all need robust frameworks. The report emphasises that tokenisation works when it adds value versus simply replicating existing off-chain markets.

In sum: while new investment opportunities abound, careful due diligence is required — especially when dealing with tokenised private credit or real estate sectors.

6. Implications for Crypto Investors & Practitioners

From the vantage of someone looking for new crypto-asset opportunities and practical blockchain uses, several implications emerge:

a) Diversification beyond typical tokens:

RWA tokenization allows investors to go beyond native crypto tokens (e.g., utility or governance tokens) into yield-bearing, asset-backed tokens. This potentially complements traditional crypto holdings and ties into real-world economic activity.

b) Yield and revenue opportunities:

Private credit tokens, tokenised funds, tokenised debt may provide new sources of revenue (interest payments, yield), if the underlying structures are reliable and transparent. As the market matures, being early in infrastructure (wallets, custody, platforms) may confer advantage.

c) Infrastructure becomes important:

As you build or integrate with wallet platforms like “dzilla Wallet”, considerations of how RWA tokens will be handled — compliance workflows, asset-token standards, chain choice, bridging, settlement finality — become highly relevant. The bridge between TradFi and DeFi is widening.

d) High potential but high risk:

Given the early stage, there is both upside and risk. Entry barriers for investors may be higher (accreditation, whitelist, KYC), secondary market volumes may be thin, regulatory shifts could stall growth. Hence, strategies must weigh both reward and risk.

7. What to Watch & Next Steps

To turn this high-level trend into actionable investment or development steps, here are some watch-points:

- Regulatory clarity: Track major jurisdictions (US, EU, Singapore, Switzerland) for progress in defining tokenised securities, RWA frameworks and KYC/AML.

- Platform adoption: Monitor which platforms, blockchains or protocols emerge as standard for RWA issuance and settlement; those may become network effect winners.

- Liquidity metrics: Beyond issuance volume, observe whether secondary trading volumes improve, bid-ask spreads tighten, genuine liquidity develops.

- Asset types: Focus on tokenisation of asset classes that have clear benefits from blockchain adoption (private credit, securitised debt, illiquid commodities) rather than tokenising assets that are already highly liquid and efficient off-chain (e.g., major listed stocks).

- Developer/infrastructure opportunities: For wallet or DeFi builders, think about integration of RWA tokens, bridging TradFi assets to DeFi rails, enabling settlement, collateralization, tokenized fund access.

8. Conclusion

The tokenization of real-world assets represents one of the most promising intersections between crypto/blockchain and traditional finance. For the audience seeking new crypto assets, income opportunities and practical blockchain applications, RWA tokenization offers a compelling narrative: asset-backed tokens which can expand access, improve efficiency and capture value from previously illiquid market segments.

However, while the long-term forecasts (US$ 20–30 trillion) are eye-catching, the path there is not smooth. Watching for regulatory maturity, infrastructure build-out, and genuine liquidity will be critical. For developers and investors alike, engaging early — but with discipline — may yield significant competitive advantage as the RWA wave gathers momentum.

As you build your wallet, your projects and your investment strategy, consider how tokenised real-world assets might play a role in your ecosystem: as integrated assets, as yield carriers, as bridge between TradFi and DeFi. This is a practical opportunity, not just theoretical.

Stay alert, stay informed, and position yourself to ride the next frontier of blockchain finance.