Main Points :

- S&P Global Ratings assigned a B- rating (non-investment grade) to Strategy Inc. (formerly MicroStrategy) due to its heavy reliance on Bitcoin, narrow business focus, weak dollar-liquidity and structural currency mismatch.

- The company holds approximately 640,808 BTC, acquired via equity and debt issuance, but the rating reflects that Bitcoin holdings are excluded from adjusted-capital calculations under S&P’s methodology.

- Despite the “junk” (B-) rating, the outlook is “stable,” based on the company’s access to capital markets and management of convertible debt maturities.

- This is the first time a major credit-rating agency has formally rated a company whose business model is essentially a Bitcoin treasury company — marking a precedent for how traditional finance may evaluate crypto-treasury models.

- For investors seeking new crypto assets and revenue opportunities, the case highlights both the opportunities and downside risks of companies built around blockchain assets rather than diversified operating businesses.

1. Context & Background

The credit-rating decision by S&P Global comes at a pivotal time in the evolving relationship between traditional finance (TradFi) and the crypto economy. Until now, companies publicly accumulating Bitcoin as a treasury asset were largely outside the scope of mainstream credit evaluation. Strategy Inc. (ticker MSTR), under Executive Chairman Michael Saylor, metamorphosed from a business-intelligence and analytics software firm into what many analysts call a corporate Bitcoin-holding vehicle.

In its October 27 2025 review, S&P assigned Strategy an issuer credit rating of B-, placing it firmly in speculative-grade (junk) territory — well below the lowest investment-grade rating of BBB-.

Why is this significant for blockchain practitioners and new asset seekers? Because it signals that the credit-markets infrastructure is now beginning to treat crypto-treasury firms seriously — albeit with caution. For those evaluating new token projects, stable-coin operations, or corporate treasury models built around blockchain, understanding how such firms are judged by credit-raters matters: liquidity, asset composition, business diversification, and currency mismatches now form part of the lens.

2. Why the “Junk” Rating?

2.1 High Bitcoin Concentration and Narrow Business

S&P’s analysis cites Strategy’s high concentration in Bitcoin as both a defining strength and its greatest vulnerability. The firm’s assets are dominated by Bitcoin holdings, while its operating business (legacy software) contributes marginally to cash flow. For H1 2025 the software business posted about –US$37 million in operating cash flow.

That narrow business focus compounded with the non-yielding nature of Bitcoin (i.e., it does not generate operating cash flow like a typical business) leaves the company with weak “risk-adjusted capital” under S&P’s methodology. The agency excludes Bitcoin (and similar volatile, non-operating assets) from equity when calculating adjusted capital, leaving Strategy with a negative risk-adjusted capital ratio.

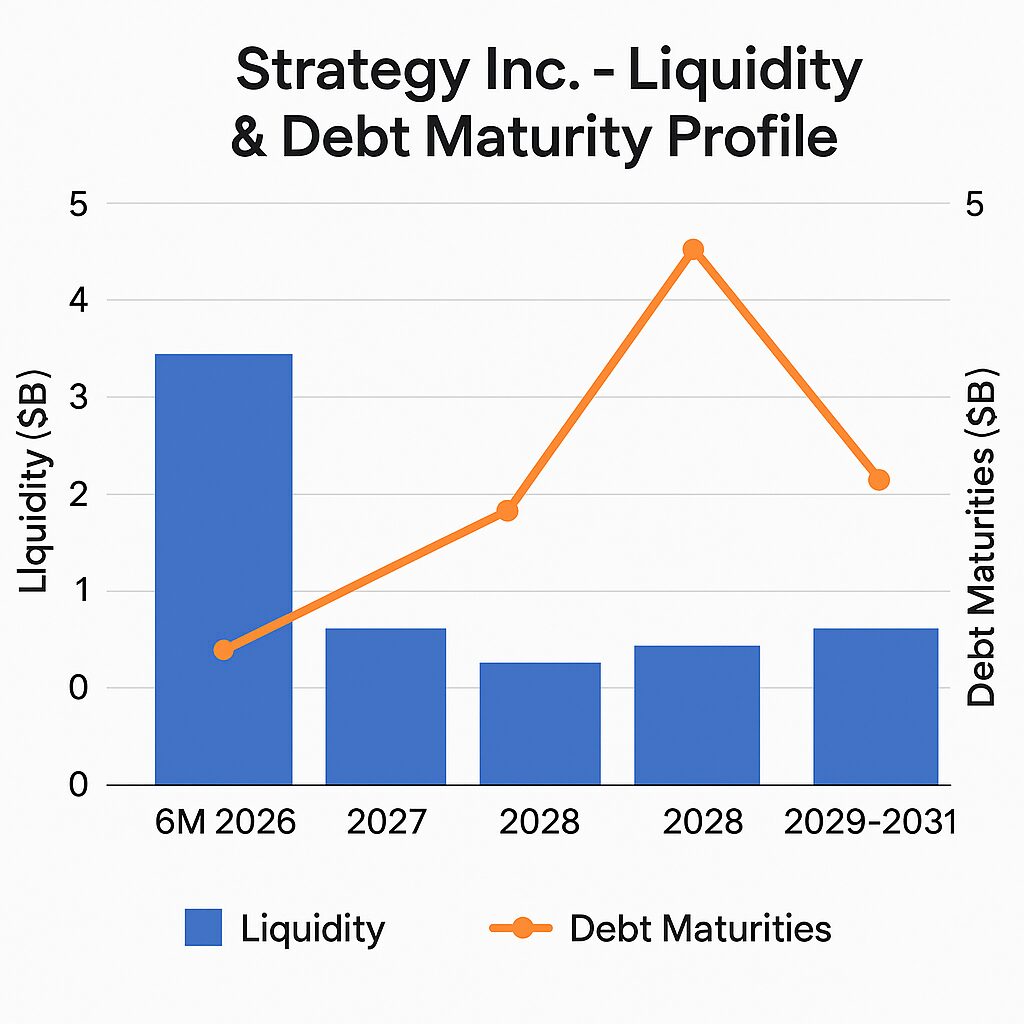

2.2 Low U.S. Dollar Liquidity and Debt Mismatch

Another concern flagged by S&P: although Strategy holds large Bitcoin reserves, its actual dollar-liquidity (i.e., cash or reliable liquid assets) is low. Meanwhile, many of its obligations — convertible notes, preferred stock dividends, other debt — are denominated in U.S. dollars. In effect, the company has what S&P called a “structural currency mismatch” (assets largely in BTC, obligations in USD).

If Bitcoin were to decline sharply, or if capital-market access were constrained, Strategy might be forced to sell Bitcoin at depressed prices to meet dollar-denominated liabilities — raising liquidity and credit-risk concerns.

2.3 Dependence on Capital Markets and Convertible Financing

Strategy has repeatedly issued convertible debt, preferred shares and equity to fund its Bitcoin accumulation strategy. While this has allowed the company to amass significant BTC holdings (~US$70 billion value mid-2025) relative to debt (~US$15 billion convertible debt + preferred equity) , the reliance on refinancing and capital markets poses risk if market conditions sour. S&P notes that access to capital markets and the maturity profile of debt give the company breathing room — but that if access is lost, downgrade risk increases.

3. A New Precedent for Crypto-Treasury Firms

This rating is important beyond Strategy itself. According to S&P, this is the first time a major credit-rating agency has rated a corporate entity whose primary business is accumulating Bitcoin as treasury assets.

For investors and blockchain project developers, this represents a turning point: institutions (pension funds, fixed-income investors) often require rated debt before allocating. A rating opens doors for institutional flows into a space previously dominated by equity/speculative investment. Strategy can now access debt markets with a formal rating (albeit B-).

However, its status as a “junk-rated” entity (six notches below investment grade) means caution remains. For newer token issuers, stable-coin firms or treasury-model firms, this exemplifies that rating agencies will treat crypto-balance-sheet risk, liquidity, business diversification and currency exposures much as they treat traditional firms — perhaps even more stringently given the novel risk profile.

4. Implications for Crypto Investors & Practitioners

4.1 For Asset-Seekers and New Crypto Projects

If you are seeking new crypto assets, exploring blockchain applications or designing revenue models, the Strategy case offers multiple lessons:

- Treasure-asset business models carry inherent balance-sheet and liquidity risks. Just because asset value is sitting in Bitcoin doesn’t mean operating liquidity or capital-resilience is strong.

- Diversification matters — A pure-treasury model, without reliable revenue or cash flow, will be judged more harshly.

- Dollar-liability exposure is a key risk. Even if assets are denominated in crypto, many obligations remain in fiat: currency-mismatch risk is real.

- Institutional credit pathways are emergent but challenging. A rating may open access, but only after strong risk-controls, liquidity buffers and business rationales are established.

4.2 For Blockchain Use-Cases and Treasury Integration

From a practical blockchain application standpoint, a few key implications follow:

- Business models that treat blockchain assets as strategic reserves (e.g., corporate treasuries, token-holding entities) must embed clear risk-management frameworks: how assets will be monetised, how liabilities are structured, how liquidity is maintained.

- Projects designing token-issuance or token-treasury mechanisms (for example, issuing a token and using proceeds to hold Bitcoin) should anticipate how rating agencies, lenders or institutional investors may view the model: heavy asset concentration, limited operating diversification, and mismatch of currency tenors will weigh negatively.

- On the flip side, institutional credit recognition of crypto-treasury models (as exemplified by this rating) could improve access to capital for well-structured firms — potentially reducing cost of capital and increasing credibility.

5. Recent Developments & Forward Look

- While the rating is “stable,” S&P indicated that an upgrade in the next 12 months is unlikely unless Strategy materially improves its dollar-liquidity, reduces reliance on convertible debt, expands diversified business operations and mitigates the currency-mismatch risk.

- Conversely, downgrade risks are present: if Bitcoin collapses, or if the firm faces refinancing difficulty, forced liquidation of BTC holdings at depressed prices could trigger rating action.

- From a broader crypto-market viewpoint, some analysts (e.g., J.P. Morgan) interpret the exclusion of Strategy from the S&P 500 index earlier in 2025 as a warning sign for corporate models built on crypto accumulation rather than operating businesses.

For token designers, wallet developers, non-custodial protocols and new crypto-assets, what lies ahead is a deeper integration of traditional finance sensibilities (liquidity, capital-structure, currency-risk) into blockchain business models. The rating serves as a benchmark.

6. Conclusion

The S&P Global B- rating of Strategy Inc. marks a landmark moment: the first formal credit-rating of a Bitcoin-treasury-centric firm by a major agency. For blockchain practitioners, token issuers, digital-asset investors and wallet innovators, this development underscores that the line between “crypto business” and “traditional business” is increasingly blurring — and with it, the same risk-factors (liquidity, liability currency, diversification) apply.

If you are seeking the next revenue source or exploring blockchain assets, consider this key takeaway: asset accumulation alone is not enough. Business models anchored in Bitcoin or tokens must also think in terms of credit-worthiness, liquidity pathways, liability management and institutional acceptability. The Strategy case offers both a roadmap and a cautionary tale.

Would you like me to build a dedicated chart outlining the liquidity & debt maturity profile for Strategy (and analogous crypto-treasury firms)? I can prepare a visual diagram.