Main Points :

- People’s Bank of China (PBOC) Governor Pan Gongsheng explicitly warned on October 27, 2025, that stablecoins pose a threat to global financial stability and monetary sovereignty.

- Stablecoins are accused of failing to meet core compliance standards such as KYC (Know Your Customer) and AML (Anti-Money Laundering), which creates risks of illicit fund flows and undermines regulatory frameworks.

- China reaffirmed its strict ban on cryptocurrency trading and mining domestically and signalled stronger enforcement of those measures.

- At the same time, China is accelerating the deployment of its central bank digital currency (CBDC), the e‑CNY (digital yuan), reinforcing state-led digital finance.

- Meanwhile, in other Asian jurisdictions (Japan, South Korea, Hong Kong) regulated stablecoins and fiat-pegged tokenisation are advancing, presenting a contrast in regional strategy.

- For investors, blockchain practitioners and crypto-asset strategists, these developments carry important implications for new asset opportunities, regulatory risk, and infrastructure design.

1. China’s Message & Regulatory Posture

In Beijing at the 2025 annual Financial Street Forum, PBOC Governor Pan Gongsheng delivered a stark message: stablecoins remain “in their early stages of development” and are “still unable to meet the basic requirements of financial supervision”. He stressed that these instruments have exacerbated weaknesses in the global financial system—pointing in particular to gaps in customer identification, AML/KYC, and oversight of illicit-fund flows.

He also flagged that stablecoins may undermine monetary sovereignty in less-developed economies, as dollars-pegged tokens become de-facto digital dollars and circumnavigate national monetary controls.

Domestically, the PBOC reaffirmed that the established ban on cryptocurrency trading, mining and exchange-operations remains firmly in place and will continue in coordination with law enforcement.

From a reading of the statements and additional reporting, the Chinese regime is signalling that:

- Private stablecoins (especially dollar-pegged, overseas-issued) are viewed as systemic risk vectors.

- Any digital currency ecosystem in China must remain firmly under state-control (via e-CNY or other state-approved instruments).

- Offshore and cross-border stablecoin developments will be closely monitored and potentially constrained.

For practitioners in the blockchain space, this means the Chinese market remains high-risk for independent stablecoin issuance or speculative crypto-asset projects unless aligned with state policy.

2. Global Stablecoin Landscape & Cross-Border Dynamics

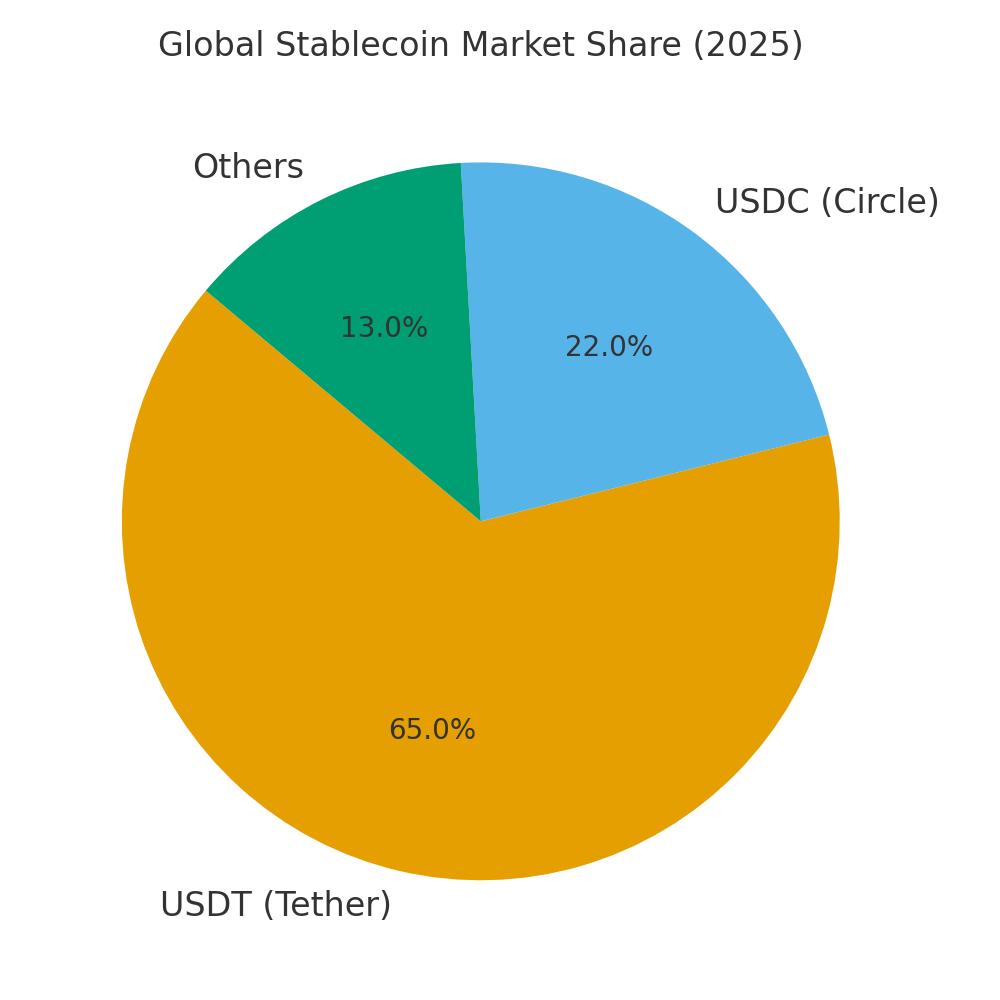

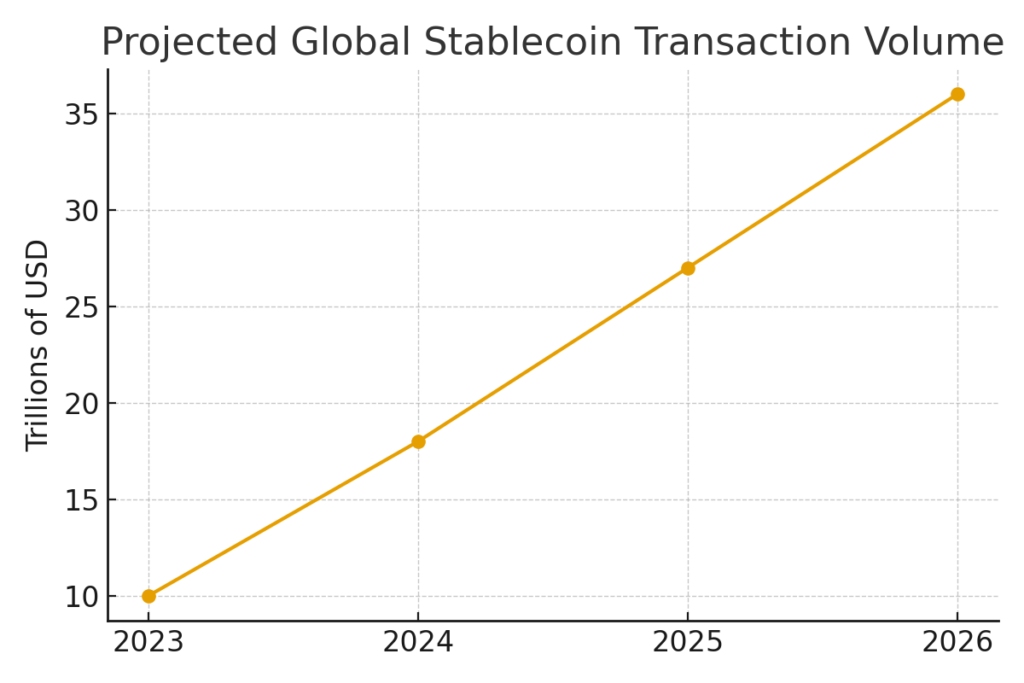

The PBOC’s concerns echo broader global regulatory anxiety: the market cap of stablecoins stood at about US $308 billion, with the largest issuers accounting for ~87 % of supply. Moreover, transaction volumes in the sector (including DeFi and off-chain uses) reached tens of trillions of dollars annually.

Notably, the dominance of U.S.-dollar-pegged stablecoins is seen by Chinese economists as a strategic challenge to the internationalisation of the renminbi (RMB).

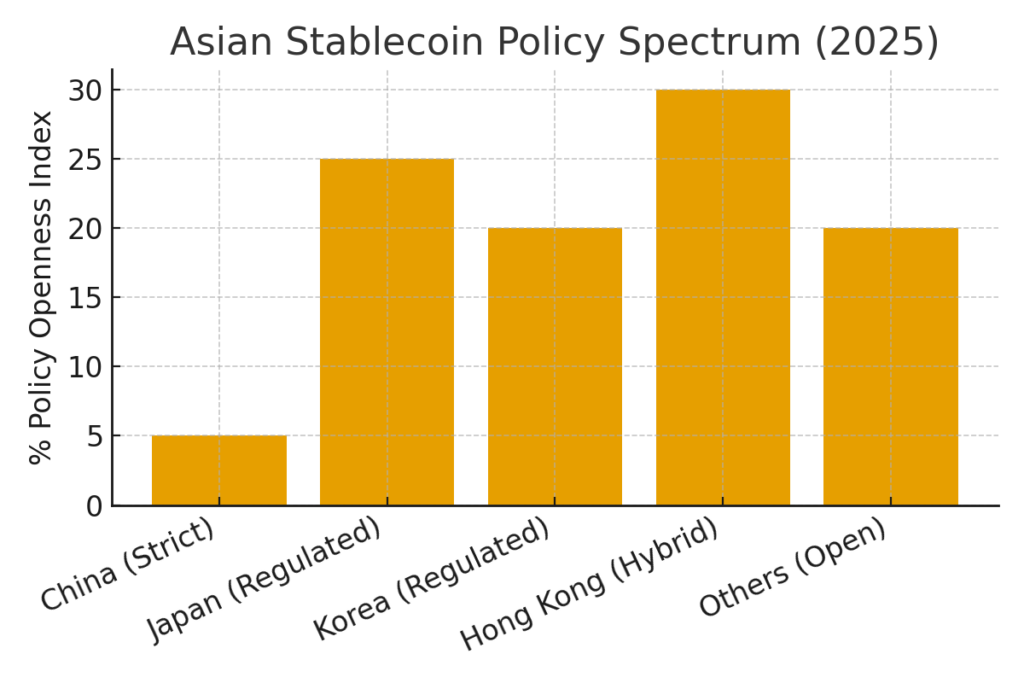

At the same time, other Asian markets are making regulatory and infrastructure moves:

- Japan: issuance of a yen-backed stablecoin (JPYC) has launched.

- South Korea: regulatory approval of a won-pegged stablecoin (KRW1) on Avalanche.

- Hong Kong: developing licensing regime for stablecoin issuers and tokenised assets, potentially serving as an offshore hub even as China remains strict domestically.

These developments set up a regional bifurcation: China strict and state-led, versus neighbouring jurisdictions more open and market-oriented in the stablecoin/tokenisation space. For investors and developers, this means opportunity zones may lie outside mainland China even for projects targeting Asian markets.

3. Implications for Crypto Assets, Blockchain Projects & Revenue models

For readers seeking new crypto assets, revenue sources and blockchain applications, the above developments yield several actionable considerations:

3.1 Regulatory Risk as a Strategic Filter

The PBOC’s warning underscores that stablecoins (and broadly crypto projects) carry regulatory tail-risk. Projects that rely heavily on dollar-pegged issuance, ambiguous governance or cross-border flows might be vulnerable. For example, if a stablecoin is used in a jurisdiction with weak controls, or for cross-border remittances circumventing capital-flows controls, regulators may step in. Developing markets could face currency-flight issues.

As a practical tip: when evaluating a new crypto asset or revenue stream—particularly stablecoins or tokenised securities—one should assess the issuer’s regulatory jurisdiction, reserve auditing, compliance architecture (KYC/AML), and cross-border flow exposure.

3.2 Stablecoin Infrastructure & Payment Rail Opportunities

Despite the regulatory headwinds in China, other geographies are pushing stablecoin/payment-rail innovation. For example, the global stablecoin system is increasingly used for low-friction cross-border payments and remittances, especially in emerging markets. As a report by Standard Chartered notes: stablecoins could pull US $1 trillion out of emerging-market banks in the next three years as users shift deposits into digital wallets.

For blockchain practitioners (such as you, building wallets or swap infrastructure), this means the rails and protocols supporting stablecoins remain fertile terrain—provided regulatory architecture is respected. For instance:

- Designing swap flows between stablecoins and native tokens (e.g., ETH, SOL) with transparency of reserves and compliance.

- Exploring tokenised fiat-pegged assets in jurisdictions with clearer regulation.

- Building UX/engineering for transparency (proof-of-reserve, on-chain settlement) that aligns with risk-averse regulatory expectations.

3.3 Tokenisation and Sovereign Digital Currencies

China’s acceleration of the e-CNY rollout signals increasing state competition in the digital currency domain. For blockchain developers, this means that state-backed digital currency infrastructure may reduce the addressable market for private stablecoins within certain jurisdictions—but also opens up opportunities in interoperable token-ecosystems, e.g., tokenised trade-finance, cross-border CBDC interoperability, programmable money.

Another practical takeaway: Projects that emphasise governance, transparency, reserve backing, on-chain auditability and compliance will likely gain favour in a world where regulators emphasise “meeting core financial supervision requirements”.

3.4 Emerging-Market Arbitrage & Diversification

Given the regulatory crackdown in China but stablecoin growth in other parts of Asia and the world, there may be opportunities in adjacent markets: for example, emerging-markets where fiat currency instability is high, digital payments gaps remain large and regulation is evolving positively. The Standard Chartered estimate mentioned earlier highlights this.

For investors seeking new assets: Consider stablecoins or utility tokens anchored in jurisdictions with clear regulation, strong collateral backing, transparent operations and purpose in payments/remittance. Also consider modelling scenarios where regulatory crackdown occurs and having exit/risk-management strategies.

4. What This Means for Your Domain: Wallets, Swaps & Building Blocks

Given your interest in building a non-custodial wallet (dzilla Wallet) with BTC↔ETH swaps and good UX transparency, here are domain-specific implications:

- Compliance and reserve transparency: If you allow stablecoin integration in your wallet (e.g., USD-pegged tokens), ensure your UI communicates reserve backing, issuer compliance (KYC/AML) and jurisdictional risk.

- Chain/Token selection: Avoid reliance on tokens issued in high-risk regulatory jurisdictions (e.g., mainland China). Instead, partner with issuers registered in regulated locales (Japan, Korea, Singapore, HK) or with clear global compliance.

- SDK/API design for transparency: Your swap UX should show users when a token is a stablecoin, where its reserves are held, how redemptions work, and any regulatory disclosures. This builds trust and positions you for institutional/regulatory comfort.

- Contingency planning: Given regulatory shocks (as China has just demonstrated), build in modularity: ability to disable certain tokens if they become flagged, swap routing that can adapt to jurisdiction-blocking events.

- Cross-border remittance features: Given the emerging-market remittance use case for stablecoins, integrate features optimized for cross-border flows, minimal friction, clear charge/fee disclosure, but built with compliance in mind so as not to facilitate illicit flows.

5. Broader Trend Analysis & Quick Outlook

- The regulatory pendulum is swinging: Where earlier crypto innovation may have progressed with minimal oversight, we now see major central banks like the PBOC emphasising sovereignty, compliance and systemic risk.

- The dominance of U.S.-dollar-pegged stablecoins remains a strategic concern. China perceives a dual threat: stability risk and monetary-sovereignty risk.

- Asia is bifurcating: China stays tight; Japan, Korea, Hong Kong move ahead with regulated models. This opens investment and project-opportunity zones outside China.

- For revenue models: the role of stablecoins in remittances, tokenisation of real-world assets and programmable money is becoming more credible—but will require strong compliance architecture.

- For new crypto-asset discovery: tokens aligned with regulated stablecoin ecosystems, blockchain infrastructure enabling transparent swaps, or jurisdictions with regulatory clarity may present better risk-reward profiles.

- Risk remains high: regulatory clampdowns (as seen in China) can hit trading volumes, user sentiment, cross-border flows and token liquidity. Hence diversification, liquidity risk-management and jurisdictional assessment are critical.