Main Points:

- The popular Stock-to-Flow (S2F) model has long been used to project Bitcoin prices, yet leading analysts are urging caution about relying on it alone.

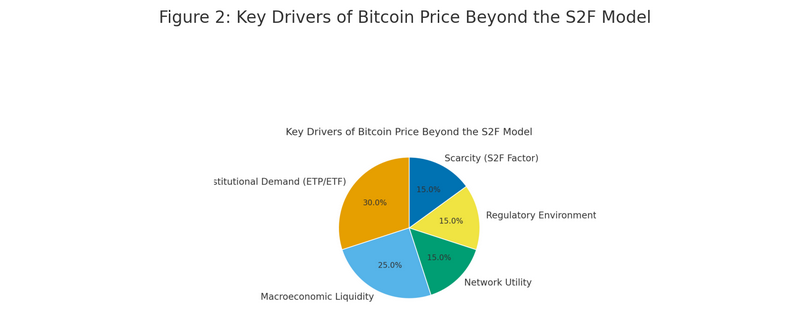

- The model focuses exclusively on the supply side—“stock” (existing supply) versus “flow” (new issuance)—and by design disregards demand dynamics.

- Some analysts argue that the rapid growth of institutional demand (ETPs, corporate treasury holdings) and macro-liquidity shifts have altered the market structure in ways the S2F model does not account for.

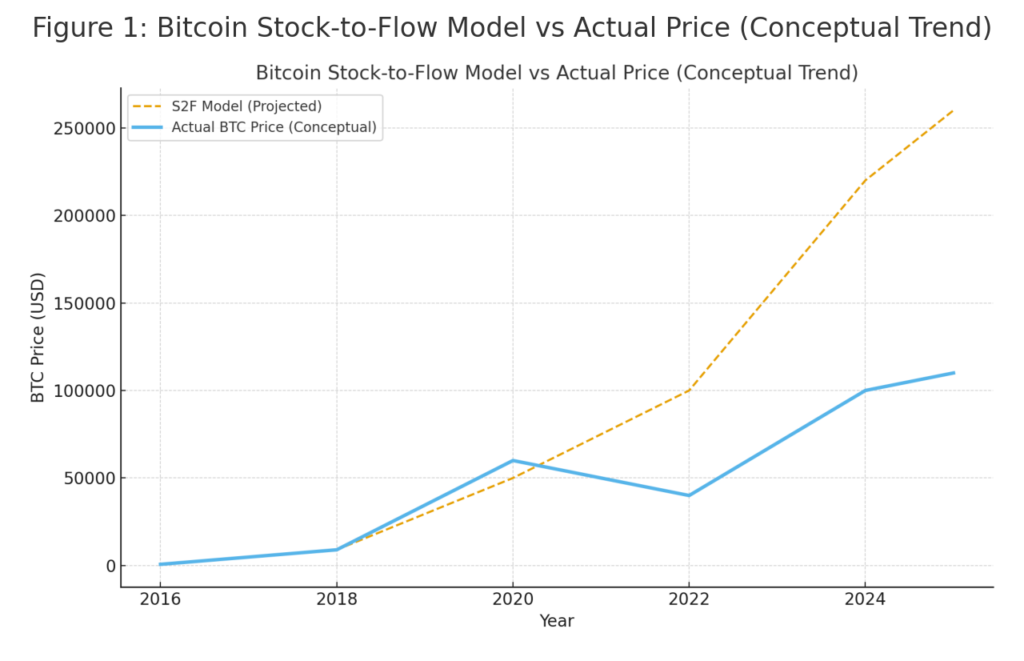

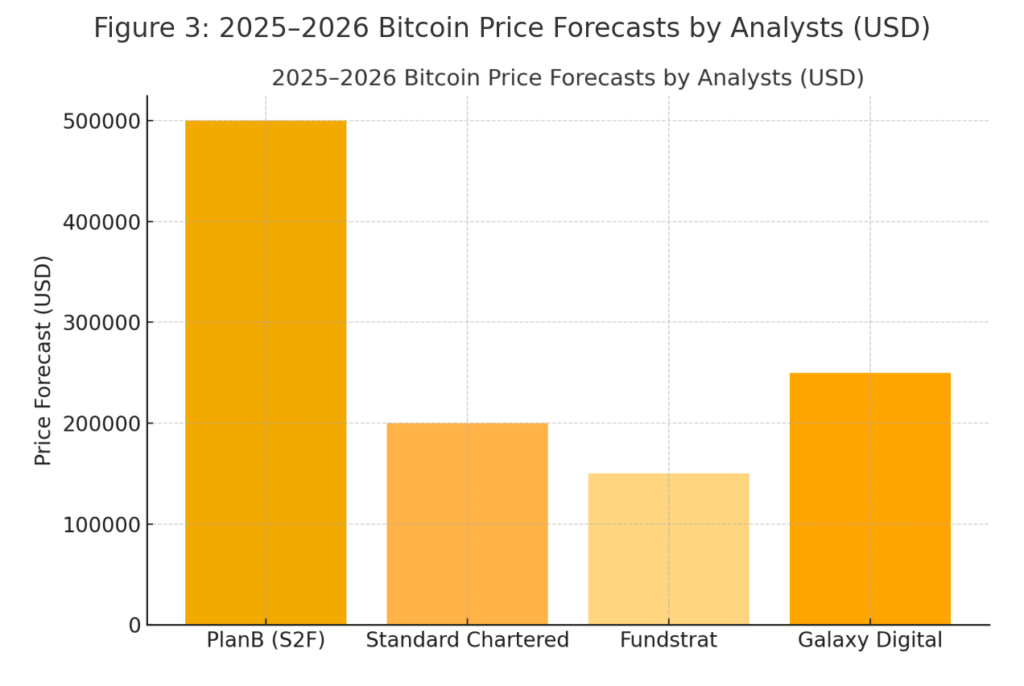

- As a result, while some still reference potential targets like $250,000-$500,000 or even up to $1 million, others warn that volatility, structural change, and demand dynamics could derail S2F-based projections.

- For crypto investors seeking new assets, income opportunities or real-world blockchain use cases, the implication is that reliance on a single model is dangerous—portfolio decisions should factor in demand, regulation, alternative metrics, and scenario risk.

1. Understanding the S2F Model

The S2F (Stock-to-Flow) model for Bitcoin is built on a simple premise: the rarer an asset (i.e., the higher the ratio of total stock to annual flow), the greater its value should be.

- Stock refers to the total number of bitcoins already mined.

- Flow refers to new bitcoins issued annually (and this is reduced around each halving event).

- Historical versions of the model showed a strong correlation between Bitcoin’s increasing stock-to-flow ratio and rising market capitalisation.

- At a high level: after each halving, flow falls, the S2F ratio rises, and in theory price should increase if scarcity drives valuation.

For many investors and analysts in the crypto space, the S2F model became a key reference: because Bitcoin’s supply schedule is known and transparent, the model offered a quantitative anchor for long-term forecasts.

2. Why Analysts Are Flagging Caution

It’s precisely because many used the S2F model so rigidly that some analysts now emphasise caution. Here are the major concerns:

2.1 Demand side is excluded

Critics note that S2F handles supply but ignores demand—yet valuation depends on both. For example: institutional inflows, ETPs, corporate balance-sheet holdings, regulatory changes and macro-liquidity all matter. One article states:

“Critics of the model often point to the lack of any calculations for demand in the equation.”

2.2 Market structure and institutional adoption have changed

Where once Bitcoin traded largely among retail and speculative investors, today major institutions, exchange-traded products (ETPs), and large corporate treasuries play a role. This structural shift means the behavior of supply + demand is different from prior cycles. Indeed, a commentator noted that “ETFs/ETPs and corporate holdings of Bitcoin demand currently exceed annual supply reduction by more than 7×”. (mentioned in the referenced article).

2.3 Model-specific limitations and historical deviation

The S2F model has been shown to deviate from reality at times. For example:

- The price of Bitcoin fell significantly in the 2022 crypto winter, diverging from S2F predictions.

- Some academic work found the model’s theoretical underpinnings were weak—i.e., that the assumed causality between scarcity and price is flawed.

2.4 Overfitting and tautology risk

Some analysts assert S2F amounts to “price predicts price” because the regression uses historical price data to calibrate scarcity to value, which can create tautological results.

2.5 External risks and non-scarcity factors

Bitcoin’s price dynamics are influenced by regulation (e.g., restrictions on mining, ETP approvals), macro-economics (e.g., money supply growth, central bank policy), innovation (competition from other assets), and network/utility factors (hashrate, use, ecosystem). These are largely unaddressed in the S2F model.

3. What Recent Developments Tell Us

Given the caution flags above, what are we seeing in the market now that influences how we should interpret S2F and its output?

3.1 Institutional demand and ETP flows

Institutional participation—through ETFs, ETPs, corporate holdings—is increasingly significant. That means the “demand” side is far from passive. Some analysts suggest that this elevated demand relative to supply reduction may compress upside or change cycle dynamics.

3.2 Macroe-liquidity and money supply

Some bullish scenarios for Bitcoin reference broader money-supply expansion (such as M2) as a tailwind for crypto. This brings unique drivers outside pure scarcity.

3.3 Peak price range reconsiderations

While earlier S2F projections pointed toward six-figure (e.g., $100k) or even $500k+ levels in a halving cycle, more recent on-chain metric studies suggest a more conservative bull-peak in the $150k-$200k range for 2025.

3.4 Model recalibrations by its proponents

The originator of the S2F model (often referred to as PlanB) still maintains high targets (e.g., $250k to $1 million), but the wide range and acknowledgement of uncertainty illustrate a softer stance.

4. Implications for Crypto Investors Seeking New Assets & Revenue Streams

For your audience—those exploring new crypto assets, looking for next-gen revenue sources, and practical blockchain applications—the following points matter:

4.1 Avoid placing all faith in one model

The S2F model, while appealing for its simplicity, should not be the sole compass. Combine supply-scarcity logic with demand analytics (volume, flows, institutional adoption), network health (hashrate, developers, ecosystem), and macro context (liquidity, regulation).

4.2 Consider emerging assets beyond BTC

If Bitcoin’s structural change (institutional adoption, ETP flows) is altering its dynamics, analogous assets (Layer 1s, utility tokens) may offer different risk/reward profiles. Models for altcoins need to integrate utility, token-omics, protocol adoption, not just scarcity.

4.3 Think in scenario terms, not crystal-ball terms

Construct scenarios: e.g., if Bitcoin hits $250k by end-2025 under strong institutional demand and benign regulation; or if it plateaus near $150k due to competition/regulatory headwinds; or if a macro shock pulls it lower. Use these scenarios to position your portfolio accordingly.

4.4 Revenue streams: consider utility + ecosystem growth

For income opportunities (staking, DeFi, token launches), scarcity-based assets offer asymmetric returns but high risk. Assets with real-world utility—payments, tokenised assets, enterprise chain adoption—may offer diversified exposure. As Bitcoin’s market moves toward a “digital gold” narrative, newer assets may present more growth potential.

4.5 Don’t ignore network/market structure changes

The rise of ETPs, corporate treasuries, mining pools, regulatory frameworks means that supply scarcity is no longer the only game changer. For example, outflows from exchanges, size of institutional flows, regulatory approvals matter. Several recent on-chain studies highlight these as key.

5. Reassessing the S2F Model: Where It Still Works, Where It Doesn’t

Works:

- Provides a transparent, deterministic supply-side baseline. Since Bitcoin’s mining schedule is known, the S2F ratio can be precisely calculated.

- Has historically correlated with Bitcoin’s price increases during earlier halving cycles (2012, 2016, 2020).

- Offers a conceptual lens: scarcity matters. Even if imperfect, scarcity is one component of value.

Doesn’t Work / Needs Adjustment:

- Fails to incorporate demand-side: institutional flows, utility, network effect, regulation.

- Assumes market dynamics remain stationary (i.e., that past cycles map onto future cycles). In a maturing market, that may not hold.

- Cannot adjust for external shocks: regulatory clampdowns, macro liquidity swings, competition from other protocols.

- It may give a false sense of certainty: models that forecast precise target prices risk overconfidence.

Conclusion

In the evolving crypto-asset landscape, the S2F model remains a useful tool, but no longer a complete playbook. For Bitcoin, the thesis of increasing scarcity still holds water, but the reality of institutional demand, product innovation, regulatory dynamics and macro liquidity means we must think more broadly.

For investors and innovators seeking new crypto assets, income sources, or practical blockchain applications, the takeaway is clear: diversify your modelling toolkit. Combine supply-based insight (scarcity) with demand-side measures, network fundamentals and scenario planning. Treat the S2F model as one input in a richer equation.

In doing so, you position yourself not just to ride cycles of scarcity, but to detect emerging opportunities and structural shifts. And in a world where innovation and adoption evolve rapidly, that may be the edge you need.