Main Points :

- The A7A5 ruble-pegged stablecoin is now explicitly sanctioned by the European Union under its 19th package targeting Russia’s war-financing mechanisms.

- This sanction marks the first time the EU has targeted a specific virtual asset issued to facilitate sanctions evasion.

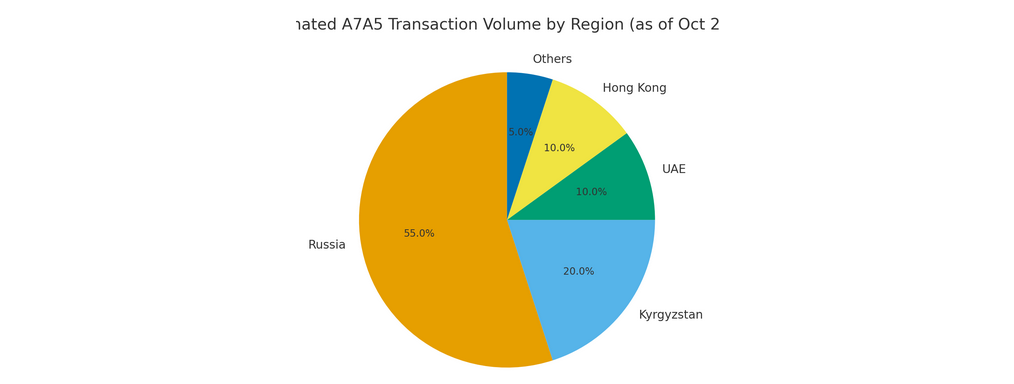

- The A7A5 system is embedded within a broader Russia-friendly crypto payment infrastructure involving banks, exchanges and jurisdictions such as Kyrgyzstan, Hong Kong and the UAE.

- For crypto investors and practitioners, the development underscores the increasing intersection of regulatory risk, geopolitics and asset flows in digital finance.

- Looking ahead, the case suggests both heightened regulatory scrutiny of stablecoins and new opportunities for compliant, transparent infrastructure to serve cross-border payments outside high-risk jurisdictions.

1. Background: What is A7A5 and why the EU moved

In October 2025 the European Union adopted its 19th sanctions package against Russia, which for the first time integrated substantial measures aimed at crypto assets and platforms. Among the targets is the ruble-backed stablecoin A7A5, described by EU authorities as “a prominent tool for financing activities supporting the war of aggression.”

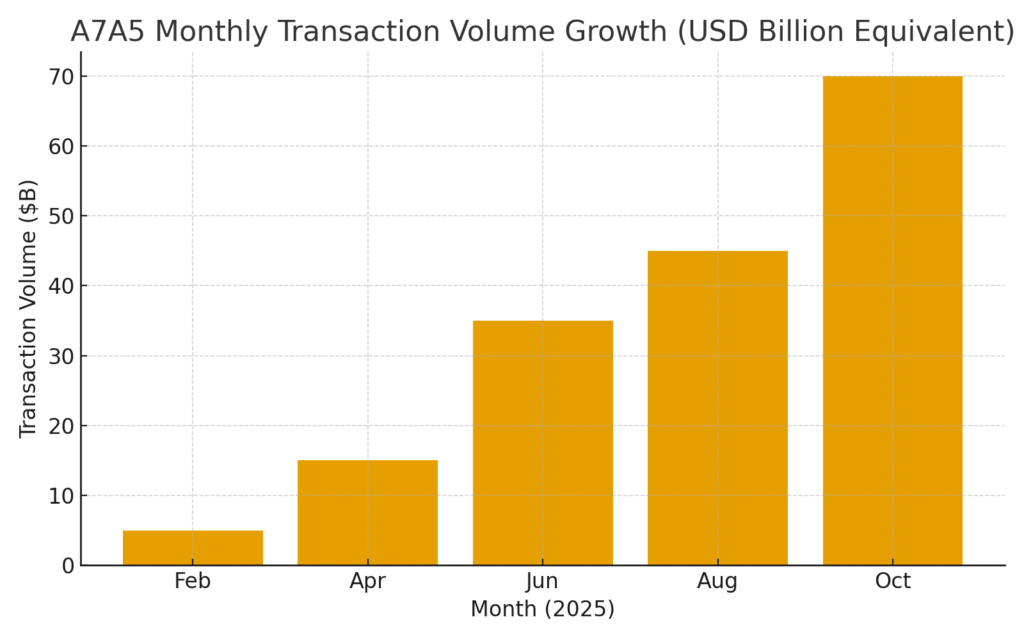

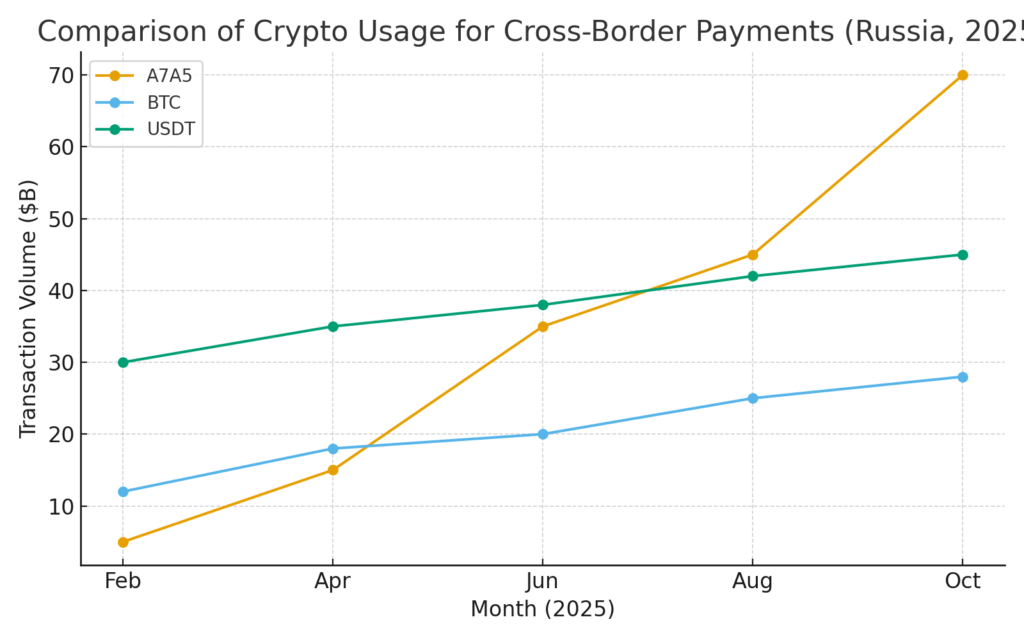

Launched in February 2025 in Kyrgyzstan, A7A5 is pegged to the Russian ruble and allegedly backed by deposits in the Russian state-owned defence-sector bank Promsvyazbank. By September it was reported to have processed tens of billions of dollars worth of transactions.

The EU responded by not only banning the token itself for transactions within its bloc, but also sanctioning the Kyrgyz issuer and platforms through which significant volumes of A7A5 are traded.

2. How A7A5 functions: a shadow-payment infrastructure

From the information available, the operational model for A7A5 appears to work as follows: A user converts rubles into A7A5 tokens via the issuer’s network, which can then be traded for dollar-based stablecoins (e.g., USDT) or other cryptocurrencies on exchanges, thereby facilitating cross-border transfers and circumventing conventional financial channels.

Because many Russian financial institutions are excluded from the SWIFT network and other standard payment rails, this kind of mechanism offers an alternative route for cross-border flows. For example, researchers reported that A7A5 processed more than $40 billion by July 2025 and more than $70 billion by October.

The jurisdictions involved — Kyrgyzstan for registration, the UAE, Hong Kong, Tajikistan for correspondent banks or traders — illustrate how such systems rely on geographically diverse layers to achieve opacity and resilience.

3. Why this matters for the crypto market and blockchain practitioners

For those interested in new crypto assets, income opportunities, and practical blockchain applications, several implications stand out:

(a) Regulatory risk is no longer peripheral

The sanction of A7A5 signals that regulators regard certain digital assets as not merely speculative tokens, but as tools in geo-financial warfare. The clearance of a stablecoin for the purpose of sanctions evasion opens a new dimension of legal and compliance risk for issuers, exchanges and service providers.

(b) Stablecoins come under intensified focus

Stablecoins pegged to non-dollar currencies (in this case the Russian ruble) are now explicitly in the regulatory cross-hairs. Builders, issuers and service providers looking at alternative-currency pegged or cross-border payment stablecoins will need to invest in compliance, jurisdictional clarity and auditability to avoid similar scrutiny.

(c) Infrastructure matters: payments, rails, jurisdictions

The A7A5 case emphasises that the rails and jurisdictions behind a token are as important as the token code itself. For practitioners building blockchain wallets, cross-chain swaps, multi-asset settlement platforms or cross-border payments, understanding the full stack of service providers, jurisdictions and regulatory touch-points is essential.

(d) Opportunities for innovation in compliant cross-border settlement

If regimes such as the EU or US take aim at opaque, sanctions-evasion-oriented crypto flows, there remains room for legitimate, regulatory-aligned digital asset infrastructure that enables cross-border business, remittances and settlement. Given the user’s interest (in new crypto assets, income and practical blockchain use), this juncture could represent an inflection point: those who design compliant, transparent tokenisation/settlement systems may gain a competitive advantage.

4. Recent developments and wider context

Beyond the EU’s action, other jurisdictions and developments reinforce the trend:

- In August 2025 the United Kingdom Treasury sanctioned entities tied to A7A5’s infrastructure, such as Kyrgyzstan-based networks, marking a coordinated effort.

- The token’s meteoric volume growth (e.g., $70 billion in transfers) underscores how quickly a stablecoin-based network can scale when designed for sanctions-evasion.

- Analysts note that Russia’s crypto usage is no longer purely retail speculation: large transfers (>$10 million) rose by 86% in Russia between the middle of 2024 and the middle of 2025, versus 44% in the rest of Europe.

- For investors and builders, the signal is clear: digital asset infrastructure intersects with geopolitics and regulation in high stakes.

5. Strategic take-aways for blockchain builders and crypto investors

Given the above, here are actionable considerations:

- Due diligence is paramount: Token issuers, exchanges, wallets or any VASP (Virtual Asset Service Provider) must conduct rigorous KYC/AML, sanctions-screening and source-of-fund assessments—especially if their asset or counterparty has cross-border settlement or non-domestic pegging.

- Jurisdiction selection matters: Choosing issuer jurisdictions or service rails in low-governance or opaque jurisdictions may create downstream compliance risk or attract regulatory targeting.

- Stablecoin architecture must be transparent: For tokens pegged to alternative currencies (non-USD), issuers should consider auditor-verified reserves, on-chain transparency, and proactive regulatory engagement.

- Cross-chain design opportunities: The user’s interest in practical blockchain use (e.g., wallet design, swaps) aligns with the idea of building infrastructure that supports compliant, multi-asset swaps (e.g., BTC ↔ ETH) and cross-border settlement while avoiding legal landmines like sanctions-evading tokens.

- Investor lens: risk vs opportunity: For investors seeking new assets or income sources, the A7A5 case underlines the importance of not only the asset’s technical promise but its regulatory hygiene and counterparty risk. A token with great yield but dubious jurisdictional backing or sanctions exposure may carry latent tail risk.

Conclusion

The EU’s sanctioning of A7A5 marks a significant milestone: it demonstrates that digital assets, especially stablecoins and cross-border payment networks, are now centre-stage in global financial sanctions and geopolitics. For you—seeking new crypto assets, income opportunities, and practical blockchain applications—this development is both a warning and an invitation. On one hand, it warns that opaque tokens and jurisdictions can face sudden regulatory closures. On the other, it invites innovation: by building compliant, transparent infrastructure and by vetting assets not only on yield or novelty but also on governance and jurisdictional risk, you position yourself ahead of the curve.