Key Points :

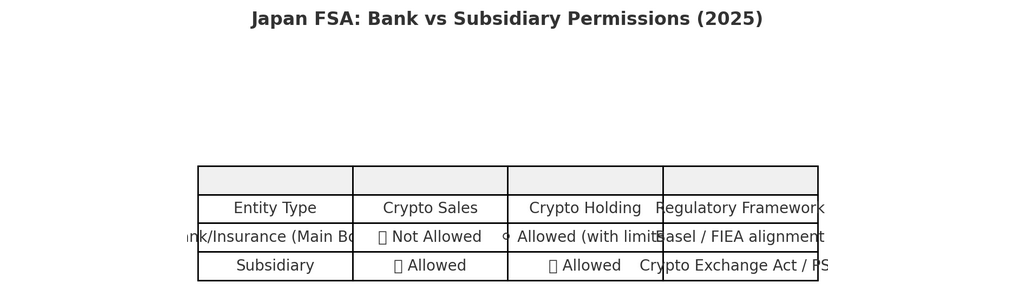

- The FSA has decided to ban crypto-asset sales by the main bodies of banks and insurance companies, while allowing such business activities to be conducted via subsidiaries.

- The regulation is being shifted from the Payment Services Act (PSA) to the Financial Instruments and Exchange Act (FIEA) in order to give crypto‐assets treatment akin to financial instruments.

- Banks may be permitted to hold crypto‐assets (e.g., bitcoin) on their own balance sheets under strict conditions, even though direct sales to customers from the bank entity remain prohibited.

- Additional rules being advanced include forbidding insider trading in crypto, requiring KYC for decentralised exchange (DEX) access, and toughening penalties for un-registered service providers.

- For practitioners and revenue‐seeking entrants: the regulatory shift signals both risks and opportunities—traditional financial players may enter crypto markets, potentially increasing competition, infrastructure, and legitimacy; but hurdles remain and timing is uncertain.

1. Tightening the Net on Banks & Insurers

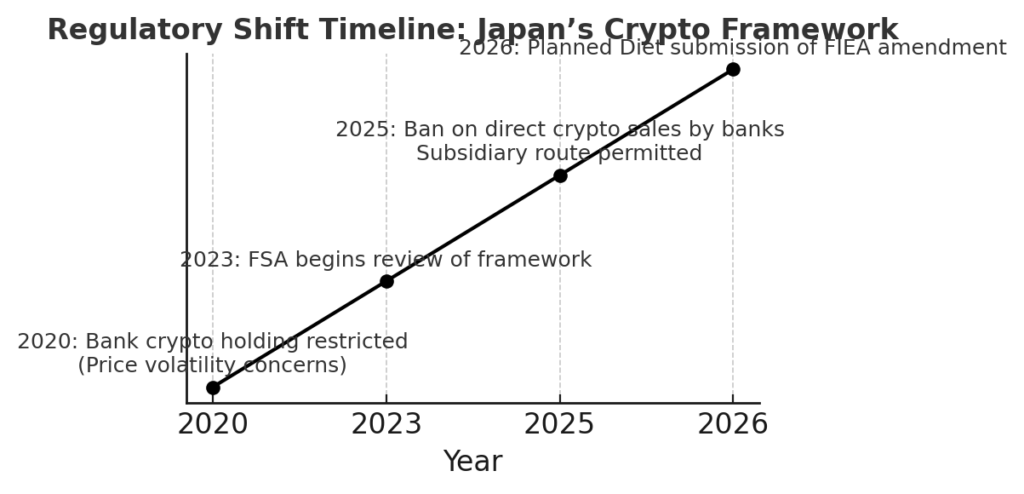

On October 22, 2025 the FSA announced that it plans to prohibit the main entities of banks and insurance companies from selling or issuing crypto‐assets, citing concerns around volatile price movements and the difficulty in ensuring customer protection.

The regulator judged that because crypto-assets can exhibit extreme volatility, banks and insurers may struggle to fully protect clients if they themselves market these assets. The decision means that their core business entities will no longer engage in crypto‐asset sales or issuance.

However, the FSA will permit the use of group‐affiliated subsidiaries (for example a separate exchange affiliate under a bank group) to engage in crypto‐asset trading, brokerage or intermediated services—so long as proper licensing and regulatory compliance is in place.

This arrangement aims to create a “firewall” between the highly-regulated bank/insurer core and the higher-risk world of crypto-assets, allowing financial groups to participate in the crypto ecosystem while preserving depositor protection and minimizing contagion risk.

2. From Payments to Financial Instruments: Shifting the Legal Framework

A key change: the FSA is working to migrate crypto-asset regulation from the Payment Services Act (PSA) to the Financial Instruments and Exchange Act (FIEA). The FIEA imposes stronger disclosure rules, investor protection regimes, and market supervision.

Under the current system (PSA), crypto‐assets were largely treated as payment instruments; the new direction treats them more like securities or other financial instruments, reflecting their evolution as investment assets.

With this shift, the FSA intends to submit a bill in the 2026 ordinary Diet session to amend the FIEA and officially give crypto-assets legal status as financial products.

Part of this migration includes bringing insider-trading rules into crypto markets (which have hitherto been lightly regulated in that respect) and extending KYC/AML provisions to decentralised platforms.

3. Subsidiary Model & Ongoing Restrictions for Parent Firms

Under the new policy, a bank or insurance company itself is not permitted to sell crypto‐assets to customers; instead, they must set up or use a subsidiary (often an “exchange affiliate”) that holds the registration under the crypto asset exchange regime.

The rationale: Services offered by the bank/insurer might give customers the false assurance that the group fully backs or knows the risks of crypto‐assets; by pushing the activity into a separate legal entity, the group can isolate risk and ensure the entity has specific regulation and licensing.

At the same time, the FSA is considering allowing the bank/insurer parent itself to hold crypto‐assets for its own account (i.e., as part of its own investment portfolio), subject to substantial risk management, capital requirements, and disclosure obligations.

This is a significant shift—as previously, banks in Japan were effectively barred from holding crypto due to volatility risks. The change suggests recognition that crypto may be more mainstream and publicly owned assets may benefit banks’ portfolios—but only under strict rules.

4. Strengthening Investor Protection & Enforcement

Beyond the structural rules, the FSA is also moving to tighten enforcement in the crypto-asset sector:

- Introducing insider-trading prohibitions for crypto-assets analogous to those for stocks and bonds.

- Extending regulatory oversight to decentralised exchanges (DEXs) — for example, requiring KYC (know-your-customer) for platforms that provide user-interfaces, and placing risk‐explanation obligations on operators.

- Raising penalties for unregistered crypto-asset service providers: the FSA has proposed elevating the maximum prison term for un-licensed operators from three to five years, and creating a “suspension power” for the securities surveillance agency to act against illegal operators.

Together these measures aim to build a more “institutional-grade” regulatory ecosystem for crypto in Japan.

5. Implications for Crypto Investors and Blockchain Practitioners

For those seeking new crypto assets or revenue opportunities, and for blockchain practitioners interested in practical use-cases, the regulatory changes in Japan present several noteworthy implications:

Opportunities:

- Traditional banks and insurance groups entering the crypto market via subsidiaries may increase overall liquidity, institutional infrastructure, and legitimacy of crypto services in Japan.

- With banks potentially being permitted to hold crypto as investments, new institutional flow into assets like Bitcoin and Ethereum may arise, which could positively affect market dynamics.

- From a blockchain-utilisation viewpoint, regulated participation by large financial firms may accelerate the roll-out of tokenised assets, custody solutions, and institutional settlement services—opening new revenue lines or project partnerships for practitioners.

- The shift to the FIEA framework may inspire global projects to view Japan as a more mature “crypto jurisdiction”—which could attract international talent, partnerships or token-listing opportunities via Japanese entities.

Risks & Considerations:

- Because the process is still under consultation, there is uncertainty around timing, detailed rules and transitional arrangements: for example, which subsidiaries qualify, what capital/risk standards will apply, and how existing firms will adapt.

- For crypto-asset developers: increased regulation may raise compliance burdens, especially where token-offerings or decentralised platforms seek Japanese users. KYC/AML and disclosures may limit “lightweight” approaches.

- Increased institutional involvement may bring greater market correlation, reducing the “decentralised frontier” feel of crypto and possibly leading to more regulated product structures (which might limit some speculative upside).

- For blockchain usability beyond trading, the conservative stance of the FSA suggests that plain retail access to highly speculative tokens may face greater scrutiny; thus practitioners may need to adapt use-cases (e.g., focusing on tokenised assets, enterprise blockchain, custody/infrastructure) rather than pure retail speculation.

6. Recent Developments & Market Context

Recent reporting confirms that the FSA is seriously considering allowing banking-group subsidiaries to register as crypto service providers and allow banks to invest in crypto under conditions.

Market commentary points out that Japan’s regulatory shift comes amid global institutional interest in digital assets, and that enabling banks may help Japan compete in the Asia-Pacific region’s digital finance ecosystem.

One market data point: in mid-October 2025 the crypto market cap briefly dipped around US $3.70 trillion with trading volume spiking to around US $224 billion.

From a timing perspective: while the FSA aims to submit a draft amendment to the FIEA by 2026, implementation may take longer and transitional rules will matter. Players should monitor the FSA’s working group announcements and proposed bill texts closely.

7. What Should You Do as an Investor or Practitioner?

- If you’re exploring new crypto-assets in Japan, recognise that the market may soon see stronger institutional infrastructure—so projects with institutional hooks (e.g., regulated exchanges, custody providers, tokenised real assets) may have advantage.

- Practitioners building blockchain solutions in Japan should consider aligning with regulated infrastructure (e.g., licensed crypto service providers) or focusing on use-cases that meet higher standards of governance, risk management and disclosure.

- For revenue generation: consider how banks or insurance groups may become clients rather than just competitors—offering blockchain-middleware, custody, tokenisation services, or integration with regulated entities within the banking group.

- Keep abreast of the regulatory bill’s progress and transitional rules (e.g., how existing banks convert or open subsidiaries, grandfathering of licences) and adjust your timeline and product strategy accordingly.

- Finally, maintain risk awareness: regulatory openness does not mean unrestricted access. The FSA is clearly emphasising investor protection, capital/risk controls, and governance—so speculative or unregulated models may face headwinds.

Conclusion

Japan’s FSA is signalling a significant shift in how crypto-assets will be treated in the Japanese financial system: from exclusion or severe restriction to regulated inclusion via banking and insurance groups (albeit through subsidiaries) and a legal framework more aligned with financial instruments. For investors and blockchain practitioners seeking new revenue sources and practical use-cases, this opens fresh pathways—but with caveats. Institutional infrastructure may accelerate, but regulatory guard-rails will tighten. Success in this market will depend not just on innovation, but on operating alongside regulated flows, aligning with risk and governance expectations, and choosing projects that anticipate both the upside and the responsibility of this next chapter in crypto adoption.