Main points:

- Major U.S. retailer Walmart’s consumer-fintech app OnePay is reportedly partnering with crypto infrastructure provider Zero Hash to integrate crypto trading, wallets and possibly on-chain deposits/withdrawals of Bitcoin (BTC) and Ethereum (ETH) into its checkout ecosystem.

- If external transfers are enabled (i.e., users can move crypto to/from the public networks rather than keep funds in a closed “walled-garden” system), the potential daily on-chain flows from retail could hit roughly US$1.7 million to US$2.5 million (or higher under more aggressive assumptions).

- Other players: Shopify (via its payments integration) now allows merchants to accept USDC on the Base network, and fast‐food chain Steak ’n Shake reported same-store sales up ~10.7% after launching Lightning‐network Bitcoin payments and cutting processing fees by ~50%.

- The practical hurdles for retailers remain: refund handling, accounting/back-office integration, price volatility (for non-stable‐coin crypto), and choosing which network/asset to adopt (BTC vs ETH vs stablecoins).

- For crypto investors and blockchain practitioners, this shift highlights a potential new demand channel: retail checkout flows entering the on-chain ecosystem, creating not only payments volume but network activity (and possibly upstream effects on liquidity, token flows, and infrastructure).

1. The Move to Crypto Payments in U.S. Retail

In recent months, the possibility that Walmart might launch crypto payments has moved from “theoretical” to something more concrete. The retailer’s in-house fintech app OnePay, already linked to debit, credit and savings products, is now reportedly partnering with Zero Hash to offer trading of Bitcoin and Ethereum, wallet services, peer-to-peer transfers and — crucially — on-chain deposits and withdrawals if full external transfer capability is enabled.

The key point: once a major retailer with a massive consumer base activates crypto flows at checkout, we move from niche merchant pilots into mainstream payments infrastructure. For new crypto investors or blockchain applications, this suggests a window into real‐world use-cases beyond speculation: crypto as payments rails, not just store‐of‐value.

2. Why This Could Matter: Scale and On-Chain Activity

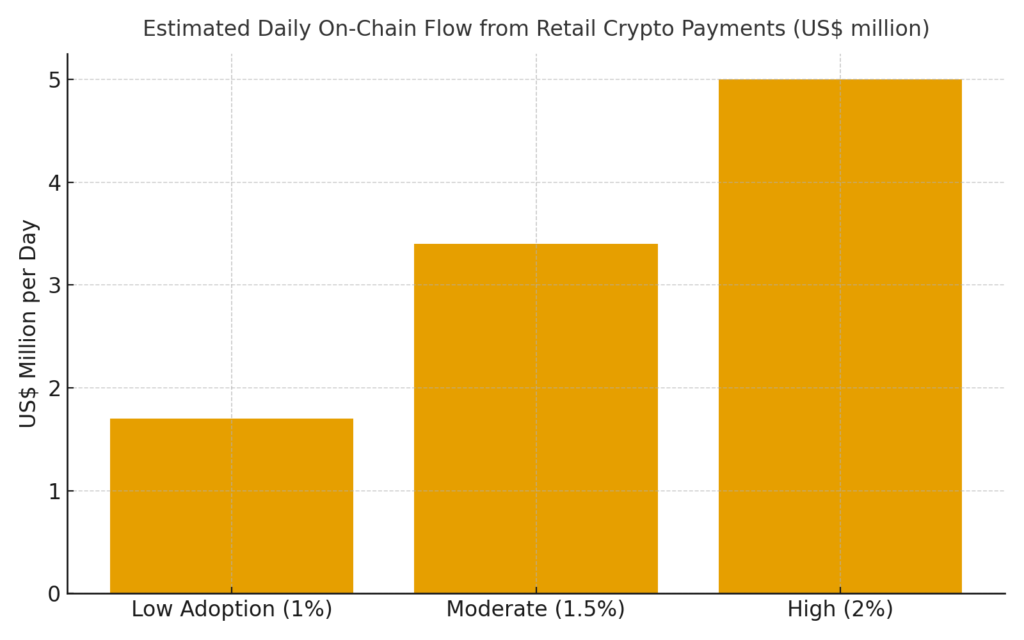

According to a report by CryptoSlate, if OnePay were to activate crypto payments at scale, the math is illustrative: assume 10 million eligible users, 50 % of them enabled for crypto, 1 % monthly purchase rate, average ticket US$150 → this yields ~US$1.7 million per day of Bitcoin purchases. If the rate rises to 2 % monthly, the number climbs to ~$5 million/day.

While ~$2 million/day is modest compared to the hundreds of millions flowing into Bitcoin spot ETFs on institutional side, the difference is in behaviour and origin: this is retail consumers spending or buying crypto, not large model‐based allocators. Also key: if those flows convert into on-chain transfers (rather than staying in non‐custodial pools), then network activity and transparency increase.

Retail checkout adoption thus has the potential to augment crypto demand and on‐chain usage, and possibly shift the balance of retail vs institutional flows.

3. Infrastructure, Assets and Rails: What’s Being Used?

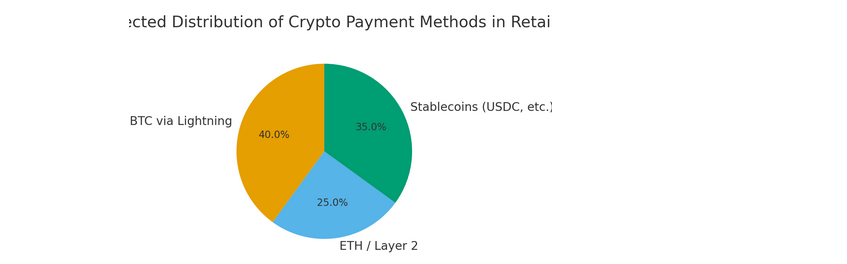

There are three major “rails” or asset choices for retailers integrating crypto checkout:

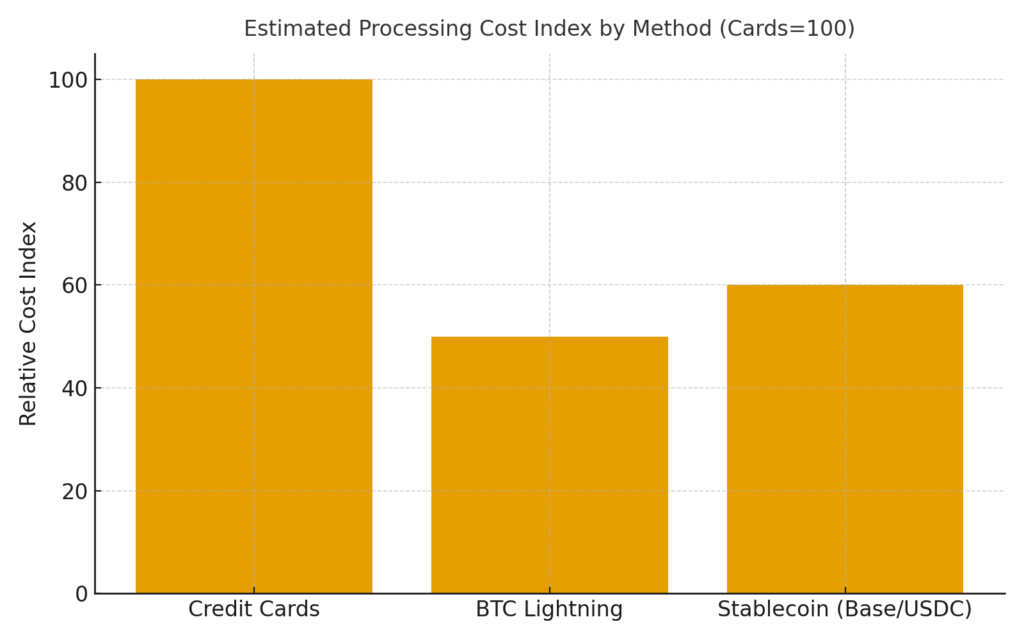

- Bitcoin via Lightning Network: fast and low fee relative to on-chain, suited for point-of-sale payments. In the Steak ’n Shake case, the chain reported a ~10.7 % same‐store sales boost after adopting Lightning, and about 50 % reduction in processing cost versus cards.

- Ethereum / Layer-2 or USDC/stablecoins: for merchants concerned about volatility, stablecoins like USDC accepted on platforms such as Base inside Shopify Payments provide fiat‐denominated value, with support for refunds, delayed capture, receipts which make the system closer to traditional payments.

- Closed‐garden vs open external transfers: The difference between an app that keeps balances inside its internal ledger (walled-garden) and one that allows withdrawals to the public chain is profound. If external transfers are enabled, then each purchase/deposit might translate into on‐chain activity, mempool load, address growth and more transparent flows. But if not, then it’s just a payments veneer without true decentralised chain integration.

4. Practical Challenges and Considerations

While the potential is real, retailers face several operational hurdles:

- Refunds and reversals: Payment cards have mature systems for chargebacks, refunds, reconciliation; crypto rails must replicate or integrate into existing systems. The article notes the readiness of merchants now shifts from “can crypto work at checkout” to “can crypto integrate into the back‐office”.

- Accounting and volatility risk: For merchants accepting non-stable crypto (e.g., BTC, ETH), the price volatility introduces business risk unless converted promptly into fiat or hedged. Many businesses may prefer stablecoins for this reason.

- Custody and settlement: Whether a wallet is custodial, non-custodial, integrated with liability limits, abiding by KYC/AML, or allows external transfers influences network effect and user control.

- Network/asset choice trade-offs: BTC has community pull and brand recognition; Ethereum offers smart-contract capability and broader ecosystem; stablecoins offer fiat‐linked utility. Retailers may adopt a mix of these depending on merchant type, ticket size, and user base.

- Regulatory, compliance and risk: Retailers and wallet providers must navigate crypto regulation, consumer protection, potential chargeback risk, and fraud detection.

5. What This Means for Crypto Investors and Blockchain Practitioners

For those hunting new crypto assets or looking for yield/utility opportunities, the retail payments trend signals several actionable possibilities:

- New demand vector: Retail checkout flows (via apps like OnePay) represent a relatively untapped channel for crypto demand. If users are buying BTC/ETH inside a wallet integrated with checkout, this could feed ecosystem and network activity.

- Network activity & on-chain metrics: The degree to which such flows become on-chain (versus staying off-chain) will impact metrics like transaction count, address activity, mempool load, and may offer signals for asset health beyond price.

- Infrastructure build-out: Wallet providers, layer-2 networks, stablecoin rails, merchant integration stacks become interesting ecosystem play-areas. If payments adoption scales, infrastructure underlying it may become valuable.

- Asset selection: From a token ecosystem perspective, stablecoins might not excite from a speculative yield angle, but the infrastructure supporting them (payments, wallets, rails) may gain. Meanwhile, BTC/ETH continue to appeal for brand and ecosystem reasons, but merchant adoption may favour low-fee-rails (Lightning, layer-2 stablecoins) rather than base-layer high‐fee chains.

- Business model innovation: Merchants cutting processing fees (Steak ’n Shake cut ~50% relative to cards) signals cost arbitrage opportunities for crypto payments. Companies that can integrate crypto payments and wallet flows may open business models (loyalty, tokenised rewards, micropayments) beyond pure checkout.

6. Latest Developments Beyond the Original Article

Since the original article:

- Square (via parent Block, Inc.) announced in October 2025 zero-fee Bitcoin payment processing for U.S. merchants until the end of 2026 (and Lightning integration via POS terminals starting November 10) — free “Pay with Bitcoin” signs and merchant onboarding for millions of businesses.

- Meanwhile, data suggests U.S. consumers using crypto just for everyday payments remains quite low (~1 % of users) though stable since 2021–24. That highlights that while infrastructure is gearing up, the behaviour shift may lag.

- Across the board, merchant payment rails incorporating crypto (Lightning, stablecoins, on-chain rails) are increasingly viable from a technology standpoint; the remaining barriers are business/operational.

7. Strategic Implications and What to Watch

For your audience—those exploring new crypto assets, revenue sources, or practical blockchain use‐cases—the following strategic vantage points emerge:

- Watcher #1: Does OnePay enable external on-chain transfers (not just trading inside the app)? That threshold determines whether flows hit public networks.

- Watcher #2: Adoption rate: what percentage of active wallet users enable crypto, what monthly purchase incidence occurs, and what average ticket size. Even low % can aggregate to millions a day.

- Watcher #3: How merchants reconcile and report crypto transactions: if integration into ERP/back-office is smooth, adoption accelerates; if not, friction persists.

- Watcher #4: Which rails/assets become dominant in retail: BTC/Lightning? ETH/layer-2? USDC/stablecoin? The outcome affects which blockchain ecosystems benefit.

- Watcher #5: Infrastructure build-up: Wallet providers, payment rails, network scaling, custody providers—all invest early for the growth phase; these may offer investment or project opportunities beyond the coins themselves.

- Watcher #6: Data signals: On-chain metrics may begin to reflect retail checkout flows (transaction counts, address growth, smaller ticket transfers) — this may become a new category of crypto analytics.

Conclusion

The integration of crypto payments into mainstream U.S. retail — exemplified by Walmart’s OnePay/Zero Hash rumoured partnership — marks a potential inflection point from speculative holding to transactional utility. For blockchain practitioners and crypto investors, this shift brings fresh relevance: not just token price movements, but real‐world flow, checkout behaviour and payment infrastructure become part of the landscape. While still early and modest in scale today (daily flows in the low millions of dollars), the precedent is meaningful: retail payment rails are opening to crypto. The winners may not only be coins like Bitcoin or Ethereum, but also the ecosystems, wallet providers and payment rails enabling them. For those seeking new assets, new revenue streams, or practical blockchain applications, monitoring this retail crypto payments wave is key.