Main Points :

- Institutional financial-players deeply entering crypto: banks, fintechs and asset managers.

- Stablecoins becoming a global payment and settlement network, beyond trading utility.

- Blockchain infrastructure upgraded: >3,400 transactions per second, 100× improvement over five years.

- Regulatory clarity accelerating adoption — especially via the U.S. GENIUS Act and other frameworks.

- Real-world-asset (RWA) tokenisation, crypto × AI convergence, and privacy infrastructure emerging.

- For practitioners hunting “next crypto”, these trends point to ecosystems around stablecoins, institutions, tokenised assets and performant chains.

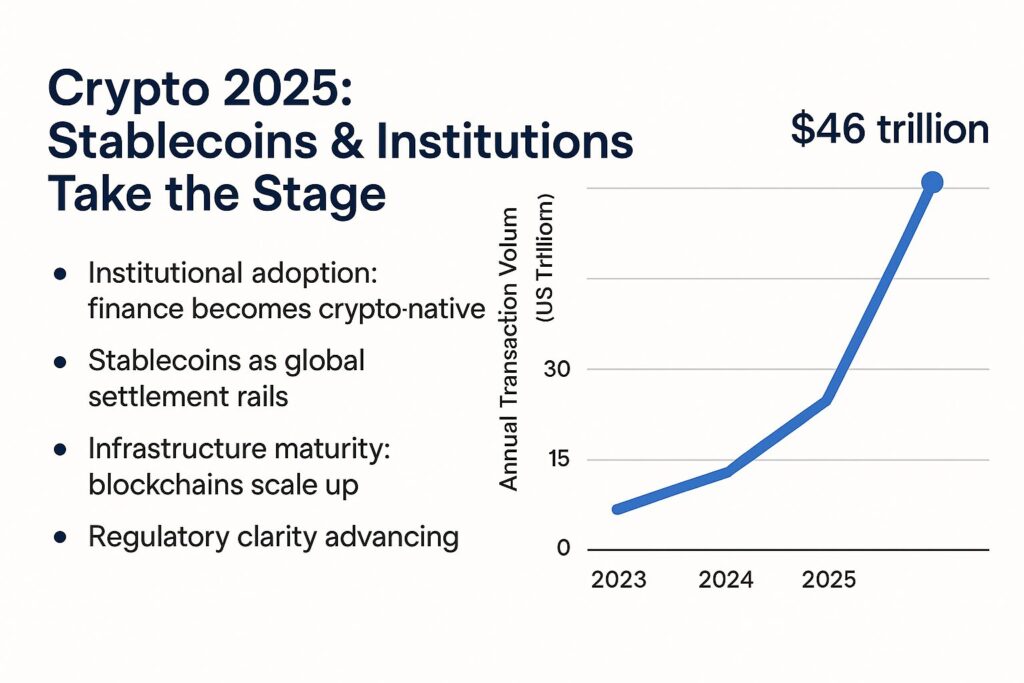

1. Institutional adoption: finance becomes crypto-native

According to the latest Andreessen Horowitz (a16z) report “State of Crypto 2025”, this year marks a transition: traditional financial incumbents like BlackRock, Fidelity Investments, JPMorgan Chase and fintechs such as Stripe, PayPal and Robinhood are actively embedding crypto-capabilities into their offerings.

For example, crypto exchange-traded products (ETPs) now hold over US$175 billion in on-chain holdings, up dramatically from roughly US$65 billion a year ago.

For practitioners looking at “where is money going”, this shift is critical: crypto is no longer a fringe “meme coin” territory, but is increasingly integrated into mainstream finance. That means new tokens, infrastructure and services will likely target institutional workflows: custody, settlements, tokenised assets, compliance layers.

2. Stablecoins as global settlement rails

One of the most striking developments is the elevation of stablecoins from “trading-pair utility” to robust global settlement rails. According to a16z, stablecoins accounted for US$46 trillion in annual transactions in 2025, with an adjusted figure of US$9 trillion, up ~87 % from the prior year.

They now rival legacy networks such as Visa or the ACH network in terms of throughput and speed: the report notes “less than one cent and less than one second” to send a dollar-equivalent globally.

Furthermore, these stablecoins hold more than US$150 billion in U.S. Treasuries, making them the approximate 17th–largest holder of U.S. debt if treated as a single entity.

What this implies for someone scanning for new revenue streams or crypto-projects: any token or infrastructure that plugs into this settlement ecosystem — stablecoin issuance, cross-border payments, compliant rails, treasury-management for stable issuers — may present significant opportunities.

3. Infrastructure maturity: blockchains scale up

A major barrier to crypto adoption has historically been scalability, cost, speed and reliability. The 2025 report highlights that certain networks now process over 3,400 transactions per second (TPS) — a more than 100× improvement versus five years ago.

As infrastructure improves, you see more “real-economy” activity on-chain: tokenised real-world assets (RWAs) now exceed US$30 billion in value, up nearly 4× in two years.

For practitioners, this means that building on blockchain is increasingly viable for payment rails, asset tokenisation, enterprise use-cases, not just speculative tokens. The “builders” now are less hobbyists and more enterprise-grade teams.

4. Regulatory clarity advancing

A key catalyst for all of the above is regulatory progress. In the U.S., the GENIUS Act was passed (signed July 2025) establishing clearer oversight for stablecoin issuers: full-reserve backing, transparency of reserves, and classification as financial institutions.

Other jurisdictions such as the UK are preparing frameworks to bring stablecoins into regulated regimes by end of next year.

Additionally, the report states that mentions of stablecoins in SEC filings have grown 64 % since the legislation passed.

This regulatory clarity means less uncertainty for institutional players, which in turn opens more capital, more services, more tokenised offerings. For someone interested in practical blockchain utilisation, this is the regime shift: now legal risk is better defined — though not eliminated.

5. New frontiers: Tokenisation, AI integration, privacy

Beyond stablecoins and institutions, the report identifies a handful of accelerating trends:

- Real-world asset tokenisation: traditional assets (U.S. Treasuries, credit, real estate) being brought on-chain.

- Crypto × AI convergence: builders are combining decentralised infra with AI models, especially around data, privacy and decentralised compute.

- Privacy and DePIN (decentralised physical infrastructure networks) gaining traction: crypto is pushing beyond mere finance into infrastructure layers.

For those looking to identify “the next token” or “the next infrastructure layer to build on”, these frontiers point to issuance platforms, privacy-tooling, tokenisation services, real-world-asset bridges, and AI-native crypto stacks.

6. What this means for the next crypto-opportunity seeker

Given the above, someone actively searching for new crypto/Blockchain revenue sources or use-cases should consider the following action-areas:

- Stablecoin ecosystem: issuance, tooling, cross-border payments, merchant adoption, treasury management. The volumes are enormous — US$9 trillion + adjusted annual transactions.

- Institutional services: custody, compliance, ETP/ETF infrastructure, tokenised securities issuance, DAO governance for large-scale players.

- Tokenisation of real-world assets (RWAs): tokenising traditional assets accelerates and is still early; providers of infrastructure here may capture meaningful share.

- Blockchain infrastructure with scale: chains that support >3,000 TPS and enterprise-grade use-cases might offer platforms for new application layers.

- Privacy / DePIN / AI integration: as crypto expands from purely financial into infrastructure and data-services, these niches could be under-explored yet high-potential.

7. Risks and caveats

リスクと留意点

Of course, this is not without risk. Some caveats to bear in mind:

- Even though regulatory clarity is improving, global regimes vary and enforcement remains uneven; tokens could face legal/regulatory shocks.

- Stablecoins dominating US Treasury holdings and money-flows may create macro-risks: for instance, large stablecoin adoption could impact the short-term treasury market and bank deposits.

- Infrastructure improvements are real, but still in progress; “scale” doesn’t guarantee decentralisation, security or product-market-fit.

- Competition will be fierce: many builders will move into the same spaces (stablecoin rails, tokenisation, institutional services) so execution, regulatory integration, trust will matter more than hype.

Conclusion

In summary, the 2025 edition of the a16z “State of Crypto” report signals that the crypto-industry is no longer just speculative — it is evolving into a credible part of the global financial and economic system. Stablecoins are moving from a niche tool to a backbone of on-chain finance; institutions are stepping in at scale; infrastructure is becoming enterprise-grade; and new frontiers like tokenised assets, privacy networks and AI integration are coming into focus.

For those of you actively looking for new crypto revenue sources or practical blockchain uses, this is the moment: the opportunities are shifting from “just a new coin” to “new rails, new issuance, new services, new infrastructure”. The winners will not just launch a token, but will plug into these structural shifts: stablecoin issuance and adoption, institutional-grade services, tokenisation of real-world assets, and high-throughput chain infrastructure.

The next phase of crypto is about utility, scale, regulation and real-world integration — if you align around those vectors, you may well identify the “next frontier”.