Main Points :

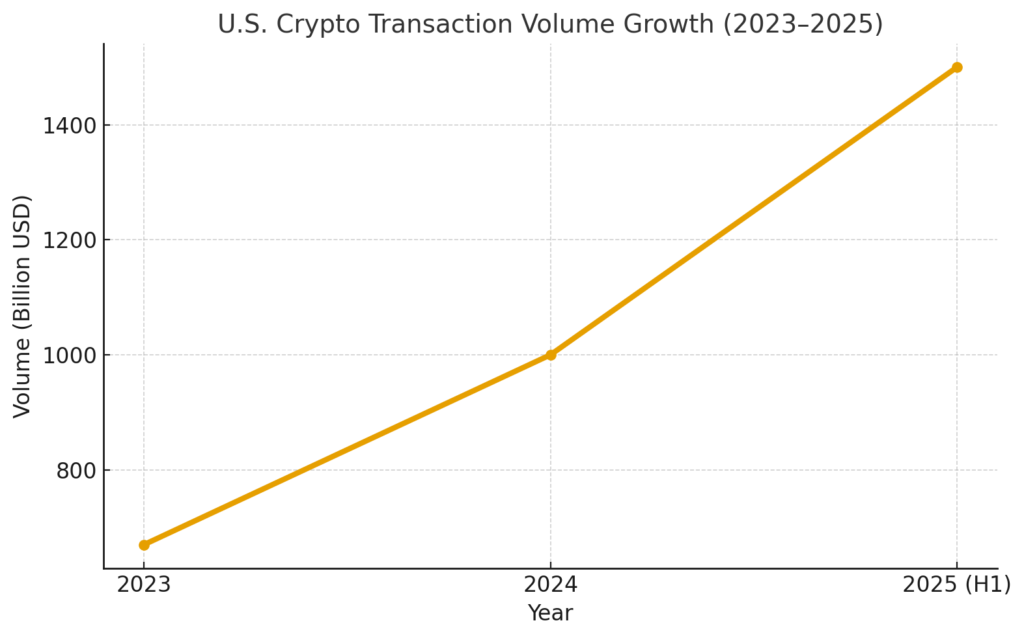

- U.S. crypto transaction volume in H1 2025 surged by about 50% year-on-year to over US $1 trillion, reinforcing the United States’ status as the largest crypto market globally.

- The regulatory environment in the U.S. has shifted substantially: clearer institutional pathways, stablecoin regulation moving forward, and a flurry of crypto-ETF filings.

- The surge is driven by institutional inflows (especially via ETFs and regulated products), improved regulatory clarity, and increased confidence among both institutional and retail participants.

- At the same time, crime and illicit flows in crypto remain a small but still relevant factor: overall illicit volumes on-chain dropped to about US $45 billion in 2024 (≈0.4% of total) according to TRM Labs.

- For practitioners seeking new crypto opportunities or blockchain use-cases, the evolving U.S. environment suggests both opportunity (institutional adoption, regulated products) and caution (regulatory shifts, compliance demands).

1. A Market Boom: U.S. Transaction Volumes Explode

According to TRM Labs’ “2025 Crypto Adoption and Stablecoin Usage” report, crypto transaction volume in the U.S. between January and July 2025 increased roughly 50 % compared with the same period in 2024, crossing the US $1 trillion mark.

This rise builds on a multi-year trend: in 2024 global transaction volume reached over US $10.6 trillion (up 56 % on 2023).

For those exploring new crypto assets or blockchain deployment, the sheer size of the U.S. market means that regulatory clarity and institutional entry matter more than ever: products that cater to institutional standards gain credibility, while purely speculative coins may face headwinds.

2. Regulatory Shift: From Uncertainty to Clarity

In the earlier years, US regulatory policy toward crypto was fragmented, with key agencies such as the Securities and Exchange Commission (SEC), Commodity Futures Trading Commission (CFTC), Office of the Comptroller of the Currency (OCC) and others issuing patchy guidance that often deterred institutional participation. However, 2024-25 marked a turning point: TRM’s policy review shows that across 24 jurisdictions roughly representing 70 % of global crypto exposure, about 70 % made progress implementing regulatory frameworks in 2024.

In the U.S., Chainalysis notes that “the year 2025 has ushered in a more favourable U.S. regulatory environment for institutions seeking exposure to crypto-assets”.

This shift matters for two reasons: one, it reduces the “regulatory risk premium” that companies had to price in. Two, it enables new product formats (such as ETFs) and institutional channels, increasing liquidity and signalling legitimacy.

Stablecoin & ETF Milestones

A key regulatory milestone: The U.S. Senate passed the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins) in June/July 2025, laying out a federal regulatory framework for stablecoins.

Also, the SEC approved generic listing standards on September 18, 2025, significantly speeding up crypto‐ETF approvals.

Consequently, institutional interest is rising: CFRA reports that crypto ETFs had inflows of US $29.4 billion through August 11, 2025.

For blockchain practitioners and asset-seekers this means: regulated wrapper products and institutional on-ramps open up new channels. If you’re developing a token, protocol or service aimed at the U.S. market, aligning with regulatory compliance and institutional structures is increasingly essential.

3. Trump Era Influence & Strategic Positioning

The referenced article underscores that during the Donald J. Trump administration, the U.S. has seen an accelerating role in crypto: the president vowed to make the U.S. the “crypto capital of the world”, and the national transaction volumes reflect that ambition.

The article notes that in H1 the U.S. trading activity jumped by about 50 % to over US $1 trillion, an increase partly attributable to “a more favourable political and regulatory environment”.

For the audience of new crypto-assets or blockchain service developers, the implication is that U.S. policy direction matters. A supportive or at least pragmatic federal posture can catalyse innovation, but it also means regulatory expectations will rise (especially around institutional participation, transparency, auditing and compliance).

4. Institutional Entry, Stablecoins & New Products

A central driver of the U.S. boom is institutional engagement. The article points out that institutions are entering via regulated products such as ETFs and stablecoins, and the regulatory clarity is helping investor confidence.

Data supports this: the CFRA study highlights the wave of ETF inflows.

Stablecoins too are increasingly foundational: TRM says stablecoins accounted for ~30 % of all crypto transaction volume in Q1 2025.

For crypto-asset seekers and blockchain implementers, this suggests strategic directions:

- Designing tokens or protocols with stablecoin integration or interoperability may unlock wider flows.

- Products eligible for ETF wrappers (or designed to feed into such structures) may have a clearer institutional path.

- Institutional service providers (custody, compliance, KYC/AML, reporting) will be in demand as the sector grows.

5. Illicit Activity: Declining but Not Eliminated

The article also touches (via TRM Labs) on regulatory frameworks and the sense of increased “confidence” in the U.S. market. Underlying this is a broader trend: illicit volumes in crypto are shrinking in relative terms.

TRM reports that illicit crypto transaction volume in 2024 was about US $45 billion, representing ~0.4 % of total on-chain volume—a drop from 0.9 % in 2023.

This declining share is positive for institutional risk-perception: if crypto is increasingly perceived as cleaner and more regulated, more capital may flow in. But the absolute size remains non-trivial and for any service provider or protocol the compliance and monitoring burdens are real.

6. What This Means for You—New Crypto-Assets & Blockchain Use-Cases

For readers interested in discovering new crypto-assets, seeking next-generation revenue sources, or deploying blockchain in business, the above trends suggest several strategic take-aways:

- Focus on U.S.-aligned compliance: Given the U.S. market size and regulatory momentum, aligning token design, listing strategy or protocol service with U.S. regulatory expectations increases chance of institutional adoption.

- Think about institutional wrapper compatibility: If the asset or protocol can feed into ETF/ETP structures, or stablecoin ecosystems, the investable “bucket” expands dramatically.

- Stablecoins remain central: Whether your project interacts with stablecoins (as settlement medium, integration layer or via programmability) you are tapping into one of the largest flows.

- Layer in services around monitoring and transparency: Even though illicit flows are a small share, the market’s emphasis on compliance means service providers (custody, transparency dashboards, audit logs) are valuable adjuncts.

- Stay abreast of fast-moving regulation: The U.S. regulatory regime is evolving rapidly (ETF approvals, stablecoin law, task-forces), and projects that anticipate regulation rather than react may gain first-mover advantage.

7. Recent Developments to Note

Beyond the core article, recent signals worth monitoring:

- The SEC’s generic listing standards (Sept 18, 2025) fast-track crypto-ETF launches.

- The GENIUS Act stablecoin law sets the U.S. on a formal stablecoin regulatory path, reducing structural uncertainty.

- Firms like Ripple are applying for U.S. national bank charters, indicating deeper crypto-finance integration.

- Despite growth, a non-profit watchdog warns of “profound risks” from crypto funding in U.S. politics and deregulation under the Trump era—important context for compliance and reputational risk.

Conclusion

The U.S. crypto market is in the midst of a structural shift: volumes are soaring (≈50 % + y-o-y in H1 2025), institutional engagement is accelerating, regulatory clarity is improving, and stablecoins and ETFs are becoming mainstream. For practitioners searching for new crypto-assets, revenue streams or blockchain use-cases, the key takeaway is that compliance and institutional readiness matter just as much as innovation. Projects or tokens that are protocol-robust, regulation-aware and institution-compatible are increasingly advantaged in the U.S. ecosystem. At the same time, the shrinking share of illicit flows improves confidence but does not eliminate risk: service providers must still embed strong transparency and monitoring practices. In short, the opportunity is large—potentially transformational—but success increasingly depends on bridging innovation and institutional/regulatory infrastructure.