Main Points :

- The Bank of Japan (BOJ) Deputy Governor Ryozo Himino publicly signalled that stablecoins are rapidly gaining significance and could partially replace bank deposits in a global payments system.

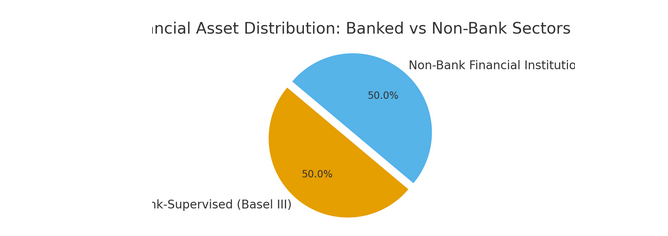

- He warned that roughly half of global financial assets now sit outside the traditional banking regulatory perimeter—particularly non-bank financial institutions not covered by the Basel III regime.

- Japan itself is moving toward institutional stablecoin issuance: a domestic startup is planning a yen-pegged stablecoin backed by Japanese government bonds, and major Japanese banks are preparing joint launches.

- Internationally, regulatory frameworks are evolving— for example, in the U.S., the newly signed “GENIUS Act” sets out federal rules for stablecoins.

- For blockchain practitioners and crypto-asset seekers, this signals new opportunity zones: stablecoins anchored by fiat or sovereign assets, institutional issuance, regulatory clarity, and blockchain-based payment rails gaining traction.

1. The Changing Financial Landscape

In his remarks at the GZERO Summit Japan 2025 held in Tokyo, Himino emphasised a fundamental shift: non-bank financial institutions (NB FIs) now hold approximately half of all global financial assets—yet these institutions fall largely outside the regulatory umbrella that covers banks via frameworks such as Basel III.

This is consequential for crypto and blockchain stakeholders because it means significant monetary-value flows are migrating to entities and networks not captured by traditional rules. Himino specifically pointed out that stablecoins, by offering 24/7 settlement, low-cost value transfer and interoperability, could play a disruptive role—especially in cross-border payments.

From a practitioner’s perspective, the signal is clear: the infrastructure of payments and value transfer is evolving. Blockchain-based rails and tokenised assets are no longer fringe—regulators are paying attention. For those scouting new crypto assets or blockchain applications, this means the favourable tailwinds may lie around institutions, stablecoins and portability rather than purely speculative tokens.

2. Stablecoins: From Niche to Strategic Payment Infrastructure

Himino asserted that stablecoins are not simply another crypto gimmick—they “might emerge as a key component of global payment systems, partially replacing bank deposits.”

Why? Because legacy payment systems (e.g., inter-bank systems, SWIFT, ACH) are increasingly mismatched to the speed, borderless nature and cost expectations of modern commerce. In contrast, blockchain-native stablecoins can offer near-instant settlement, global reach and programmability.

For blockchain practitioners, this alters the opportunity map: rather than simply building casino-style token projects, there is an incentive to build real-world payment rails, tokenised fiat or asset-backed stablecoins, cross-border settlement networks, and rails that sit between traditional finance and crypto. Institutional players will need interoperability, regulatory compliance, transparency, and blockchain-infrastructure that integrates easily with existing systems.

3. Japan’s Domestic Moves: Yen-Pegged Stablecoin and Institutional Issuance

Japan is not just watching from the sidelines. A domestic fintech startup, JPYC Co., Ltd., announced plans to issue a yen-pegged stablecoin (“JPYC”) later in 2025. The coin will be fully convertible to Japanese yen, backed by domestic savings and Japanese Government Bonds (JGBs). Initially the target is institutional investors, hedge funds and family offices, but the ambition is broader: international adoption as a digital yen.

Simultaneously, Japan’s major banks—Mitsubishi UFJ Financial Group (MUFG), Sumitomo Mitsui Financial Group (SMFG) and Mizuho Financial Group—are reported to collaborate on stablecoin issuance, starting with a yen-pegged coin with an eventual U.S.-dollar equivalent. The banks aim to build a uniform platform for corporate clients to transfer stablecoins seamlessly.

What does this mean for those in blockchain or searching for new crypto assets?

- Institutional issuance implies higher-compliance, higher-trust tokens rather than purely decentralized, speculative tokens.

- A stablecoin pegged to the yen backed by JGBs may create a novel asset class: tokenised government-bond-backed fiat-pegged units.

- Integration of such coins into banking payment systems suggests adoption of blockchain infrastructure will broaden—creating ecosystem opportunities (wallets, custody, settlement networks, cross-border rails).

- Given the yen-focus, there may be currency-arbitrage or partnership opportunities for non-Japan players aiming at Asia-Pacific corridors.

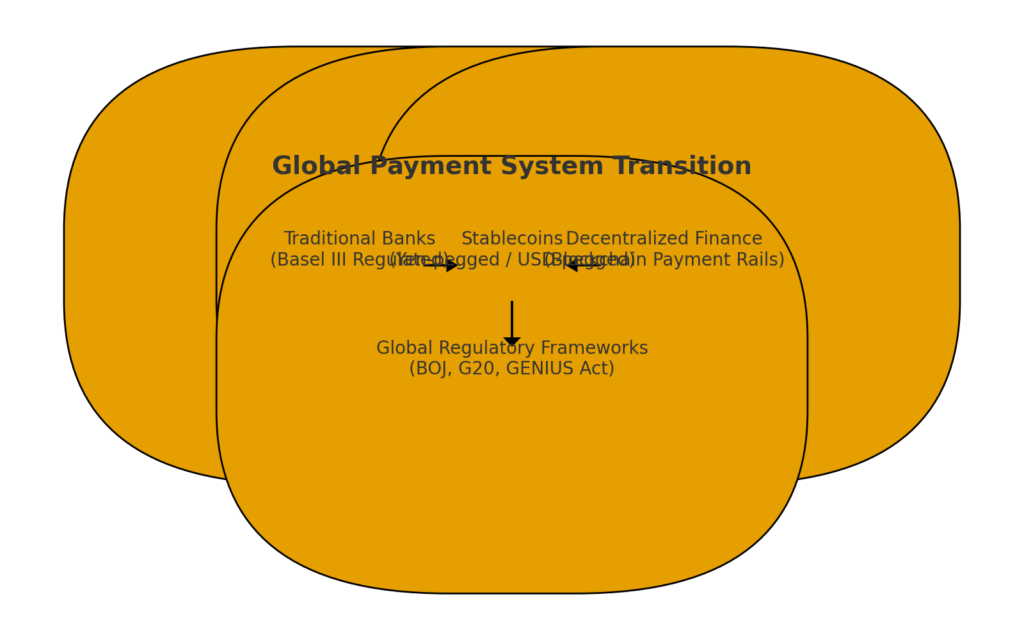

4. Global Regulatory Shifts: Harmonisation and Institutional Challenge

Beyond Japan, the regulatory environment is shifting. In the United States, the GENIUS Act (signed July 2025) established federal rules for stablecoins—an indication that governments are moving from laissez-faire to regulated infrastructure for digital assets.

Himino’s remarks underscored the need for modernisation of international prudential standards and cross-border coordination, warning that without unified frameworks the financial world faces “greater fragmentation.”

For crypto practitioners, this suggests a more policy-aware environment:

- Projects will increasingly need to comply with AML/KYC, capital-adequacy and governance frameworks.

- Issuers and developers may prefer permissioned/consortium blockchains (or hybrid models) to satisfy institutional/governance requirements. Experts already talk about banks issuing stablecoins on permissioned networks rather than public blockchains.

- Cross-border interoperability: as stablecoins gain adoption, the need for connectivity between national frameworks, banking rails, and blockchain networks becomes paramount.

- Tokenised fiat/stablecoin segments may grow faster than purely speculative utility-tokens—so the opportunity for new revenue streams lies in infrastructure, APIs, rails, custody, compliance tooling, rather than pure “coin launches”.

5. Implications for Crypto-Asset Seekers and Practitioners

Given the above, what should you, as someone looking for new crypto assets, revenue streams or blockchain real-world use cases, consider?

- Stablecoin-adjacent assets: Rather than chasing high-volatility tokens, consider platforms that enable issuance, custody or infrastructure for stablecoins (e.g., chain protocols, layer-1/2 chains, custody providers, compliance tooling).

- Tokenised asset vehicles: A yen-pegged stablecoin backed by government bonds points to a broader trend of tokenised debt/FI assets. Projects that enable tokenised bonds, tokenised fiat, or cross-border settlement may grow.

- Cross-border payments rails: With banks pushing for interoperable stablecoins and global regulators watching, there is growth potential in cross-border payment solutions leveraging blockchain or DLT.

- Regulatory-compliance service providers: As issuance and institutional adoption grow, demand rises for KYC/AML, regulatory reporting, auditing, governance, smart-contract security – all ripe for services to capture.

- Geographic arbitrage and corridor focus: With Japan emphasising yen stablecoins, there may be corridor-specific opportunities: Asia-Pacific remittances, yen-USD cross-border flows, Japanese banks’ blockchain integration.

- Token utility shift: Coins with real-world utility (e.g., stablecoins used for settlement, treasury operations, tokenised commercial flows) may offer more durable value than speculative tokens lacking such anchoring.

6. Risks and Caveats

- Regulatory risk remains high. Even though frameworks are evolving, many jurisdictions are still crafting rules; mis-steps, bans or sudden rule-changes remain possible.

- Market fragmentation: As Himino warned, without coordinated global standards fragmentation could raise cost and complexity for cross-border flows. This could slow adoption or create siloed ecosystems.

- Stablecoin design matters: Peg-backing, reserve transparency, governance, blockchain choice (public vs permissioned) — all matter for risk/reward.

- Institutional adoption doesn’t guarantee immediate returns for retail token-holders: institutional stablecoins may not trade or behave like speculative tokens; revenue streams might be more subtle (fees, interest, settlement).

- Technology risk: Integration of blockchain with banking systems is non-trivial; legacy system inertia and regulatory compliance could slow rollout timelines.

7. Summary

In summary, the speech by BOJ Deputy Governor Ryozo Himino marks a clear signal: stablecoins and blockchain-based payment infrastructure are moving from niche to mainstream, and regulators globally are waking up. For those in crypto searching for the next major theme or revenue stream, the structural shift away from purely speculative tokens toward institutional, tokenised-fiat assets and blockchain rails is significant.

Japan’s push—with a yen-pegged issuing plan and major banks collaborating—underscores this shift, and global regulatory developments (such as the GENIUS Act) show the environment is maturing.

If you are exploring new crypto assets or blockchain use cases, now is a good time to look at stablecoins infrastructure, tokenised assets, institutional rails, compliance-friendly blockchains and cross-border payment applications. The game may not just be about “what token will moon”, but “which infrastructure will underpin the next generation of value transfer”.