Main points :

- China’s central regulators have intervened to pause stablecoin project plans by major tech firms such as Ant Group (Alibaba-backed) and JD.com in Hong Kong.

- The intervention reflects Beijing’s concern about private‐sector issuance of digital currencies and the potential challenge to the state‐issued digital yuan (e-CNY).

- Hong Kong’s new stablecoin licensing regime—intended to position the city as a digital‐asset hub—now faces headwinds due to mainland regulatory caution.

- For blockchain practitioners and crypto investors, the shift signals an increased regulatory risk in private stablecoins in China’s orbit, and highlights the strategic importance of state-backed digital currency initiatives.

- The global stablecoin landscape remains dominated by U.S.-dollar–pegged tokens, and China’s stance may further cement alternative trajectories (i.e., state-controlled vs. private innovation).

1. Background: Private Tech Firms Eye Hong Kong Stablecoin Launches

Over the summer of 2025, private Chinese technology and e-commerce firms began signalling intentions to enter the stablecoin and tokenisation space via Hong Kong. China’s regulatory context had already seen domestic crypto trading banned since 2021, yet the broader blockchain ecosystem still carried appeal, particularly for cross‐border financial innovation.

Specifically, Ant Group announced participation in Hong Kong’s pilot stablecoin programme; JD.com also publicly discussed plans for issues such as tokenised bonds and offshore stablecoins.

Meanwhile, Hong Kong’s legislative body passed the stablecoin regulation in May 2025 (effective May 30), creating one of the first comprehensive legal frameworks enabling fiat-backed stablecoin issuance by regulated entities.

From a practitioner’s perspective: this represented a potentially fertile ecosystem for blockchain utilities—tokenised assets, payment rails, corporate stablecoins—and for investors, it seemed like a meaningful frontier beyond the usual U.S.-centric stablecoin world.

2. China’s Intervention: Why the Pause?

In October 2025, multiple credible outlets reported that the People’s Bank of China (PBoC) and the Cyberspace Administration of China (CAC) had instructed Ant Group, JD.com and other firms to halt or delay their stablecoin initiatives in Hong Kong.

2.1 Central concern: “Who issues money?”

One of the core regulatory questions posed internally: “Who has the ultimate right of coinage—the central bank or any private companies on the market?”

Chinese regulators appear to view privately issued stablecoins (even offshore) as a potential challenge to monetary sovereignty, payment system control, capital-flow management, and the strategic rollout of the digital yuan (e-CNY).

2.2 Risk of capital flight and financial instability

Concerns aren’t only theoretical. Chinese authorities previously flagged stablecoins as enabling speculative activity, fraud, and financial‐system instability. For example, in August 2025 the PBoC and regulators asked brokers and think-tanks to stop promoting stablecoins.

In this light, the private stablecoin push could undermine domestic capital‐flow controls and circumvent official channels, particularly given China’s capital-account constraints and monitoring frameworks.

2.3 Strategic positioning: digital yuan and renminbi internationalisation

While private firms were seeking to launch offshore yuan-pegged or Hong Kong dollar-pegged stablecoins, China’s leadership has been focusing on the internationalisation of the renminbi and the promotion of the state-sponsored digital currency.

By intervening in private initiatives, Beijing is signalling that private technology companies will not lead the issuance of key digital money instruments—it will remain under state direction.

3. Implications for Hong Kong and Global Stablecoin Infrastructure

3.1 Hong Kong’s Licence Regime Under Pressure

Hong Kong launched its stablecoin licensing regime in August 2025, expecting to become a regulated hub for fiat-backed digital tokens.

However, the withdrawal or pause of major potential issuers like Ant Group and JD.com casts doubt on the momentum of the initiative. Without backing from the largest domestic tech firms, the ecosystem may struggle to attract the critical scale and institutional trust required to compete globally.

3.2 Private stablecoins versus state-backed models

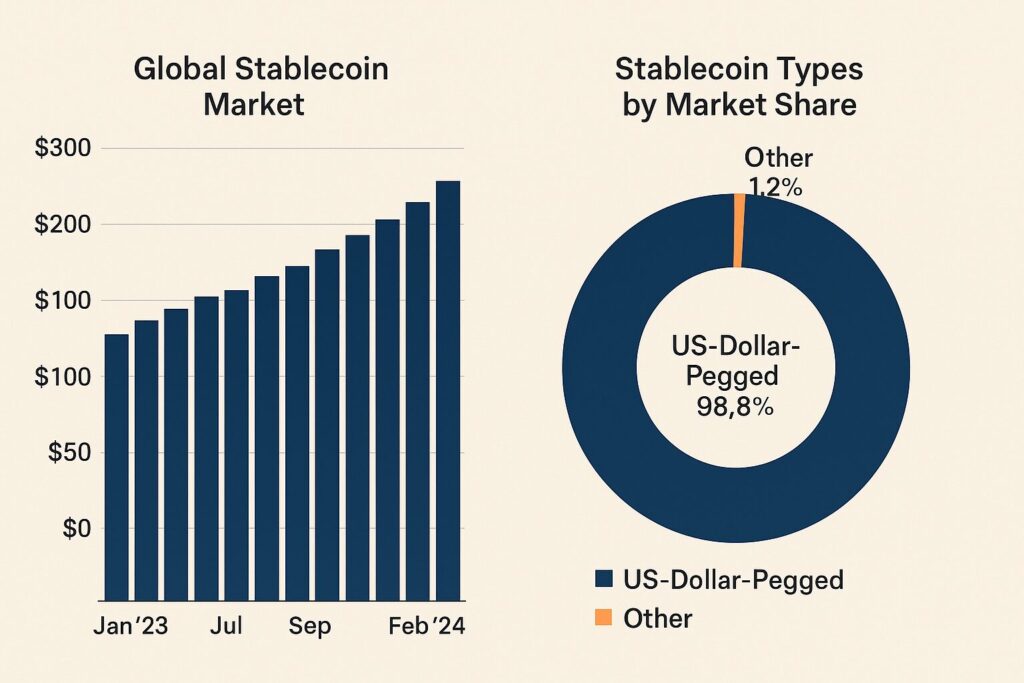

Globally, the dominant stablecoins are U.S.-dollar-pegged and privately issued (e.g., USDT, USDC). China’s move reinforces a bifurcation: private innovation permitted in some jurisdictions, but in China’s orbit the state insists on leadership over currency issuance and digital payment rails.

For the blockchain ecosystem, this means that business models relying on privately issued stablecoins in or from China may face higher regulatory tailwinds (or headwinds).

3.3 Opportunity for tokenisation, but under state oversight

Despite the halt on private stablecoins, tokenisation of real-world assets (RWAs) and blockchain utilities may still progress—but likely under state-linked control or through institutions aligned with official objectives. For example, tokenisation of a $3.8 billion money market fund by a Hong Kong unit of a Chinese bank was reported concurrently.

For practitioners, this means pivoting strategies: rather than designing private stablecoin ecosystems targeted for China, consider state-sanctioned models, partners with institutional oversight, or applications outside China’s jurisdiction.

4. What It Means for Crypto Investors & Blockchain Builders

4.1 For New Crypto & Stablecoin Investors

- Regulatory risk around stablecoins in China and Hong Kong is materially elevated: investors seeking yield or innovation around Chinese tech-linked stablecoins must incorporate state intervention scenarios into their risk models.

- In contrast, U.S.-dollar-pegged stablecoins and jurisdictions with clearer private issuance frameworks (but regulated) may appear relatively more favourable for innovation and liquidity.

- The partial global bifurcation suggests stablecoins issued under state control (e-CNY, yuan-pegged tokens) may become strategic tools rather than open-market alternatives. That means investor expectations of decentralised, privately-issued stablecoins challenging state-money may need to be revised.

4.2 For Blockchain Infrastructure and Practical Use-Cases

- Builders planning token-economies, payment rails, or decentralised finance (DeFi) applications with a Chinese dimension must factor in that private issuance of stablecoins may be off the table—leading to partnerships with regulated entities or pivoting to non-China jurisdictions.

- For enterprise use-cases—treasury management, cross-border settlement, tokenised assets—there may still be opportunity, but with stronger regulatory guardrails and likely fewer “permissionless” levers.

- The distinction between “stablecoin” as a product category (privately issued) versus “digital fiat token” (state-issued or sanctioned) is becoming sharper. Practitioners should design for both axes: technological maturity and regulatory alignment.

5. Recent Developments & Emerging Trends

- In September 2025, China backed the launch of an offshore yuan-linked stablecoin (AXCNH) in Kazakhstan via a Hong Kong-based fintech firm and a Chinese government-backed blockchain network (Conflux). This shows China still exploring stablecoin/tokenisation, but in a tightly-controlled, strategic manner.

- Earlier in the year (July 2025) a Shanghai regulator held a meeting to explore policy responses to stablecoins, signalling a possible softening or re-calibration of stance—but the overarching state control imperative remains.

- Globally, the total stablecoin market is surging past $300 billion, reinforcing the structural dominance of private, dollar-pegged tokens and the scale barrier facing alternatives.

- Meanwhile, the U.S. and other Western jurisdictions are moving toward clearer regulation of stablecoins, increasing the regulatory cost of regulatory arbitrage and reinforcing the value of regulatory-compliant architecture.

6. Strategic Take-aways for Your Crypto/Blockchain Playbook

- Risk modelling: In projects involving China or Chinese tech/finance players, include the overlay of state policy reversal (not just markets).

- Jurisdiction selection: Hong Kong may retain a regulatory framework for stablecoins, but the loss of major tech partners may reduce scale and first-mover advantage. Explore alternate hubs (Singapore, Switzerland, U.S.) for stablecoin issuance.

- Stablecoin design: Consider whether your use-case necessitates private issuance (with flexibility) or if a state‐trusted token (even if less innovative) gives you a regulatory runway.

- Tokenised assets vs stablecoins: Since private stablecoin issuance is constrained in China, pivoting to tokenised asset models (RWAs, tokenised bonds) may be more viable—so long as they partner with regulated financial institutions.

- Currency strategy: If targeting Asian cross-border flows, consider the interplay of e-CNY, offshore yuan tokens, and the dominant U.S. dollar-pegged stablecoins—in other words, build for multi-currency token models rather than assuming a yuan “alternative” disruption.

Conclusion

The recent decision by China’s regulators to intervene and pause private stablecoin initiatives by major tech firms marks a pivotal moment for the crypto-blockchain landscape—especially for those seeking “the next stablecoin” or exploring new blockchain-driven revenue sources. What once seemed like a possible frontier—Chinese tech-led stablecoin issuance in Hong Kong—has encountered a hard regulatory boundary.

For practitioners and investors, the message is clear: state monetary sovereignty still trumps private innovation when it comes to money issuance. The implications of that are two-fold. On one side, opportunities in state-approved tokenisation and digital fiat initiatives may grow (albeit with regulatory constraints). On the other, the viability of privately issued stablecoins in the Chinese sphere is now far more uncertain.

For those building the next wave of blockchain solutions, success will increasingly depend on regulatory alignment, jurisdictional agility, and a clear mapping between technological innovation and monetary policy realities. The era of “permissionless stablecoin issuance anywhere” is not over—but it is definitely more complex, especially when the world’s second-largest economy is involved.