Key Points :

- Institutional accumulation of Ethereum (ETH) has intensified, with large-scale purchases by treasury firms signaling a potential transition from bear market to new accumulation phase.

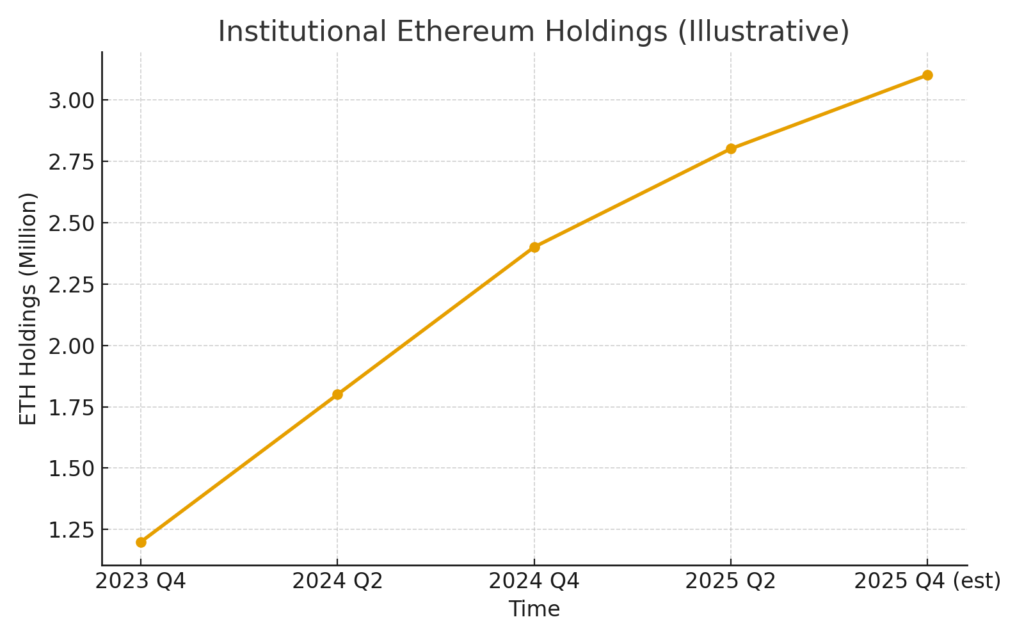

- BitMine Immersion Technologies (BMNR), led by Tom Lee, has now amassed over 3 million ETH (~2.5 % of total supply) at what it calls “substantial discounts to the future”.

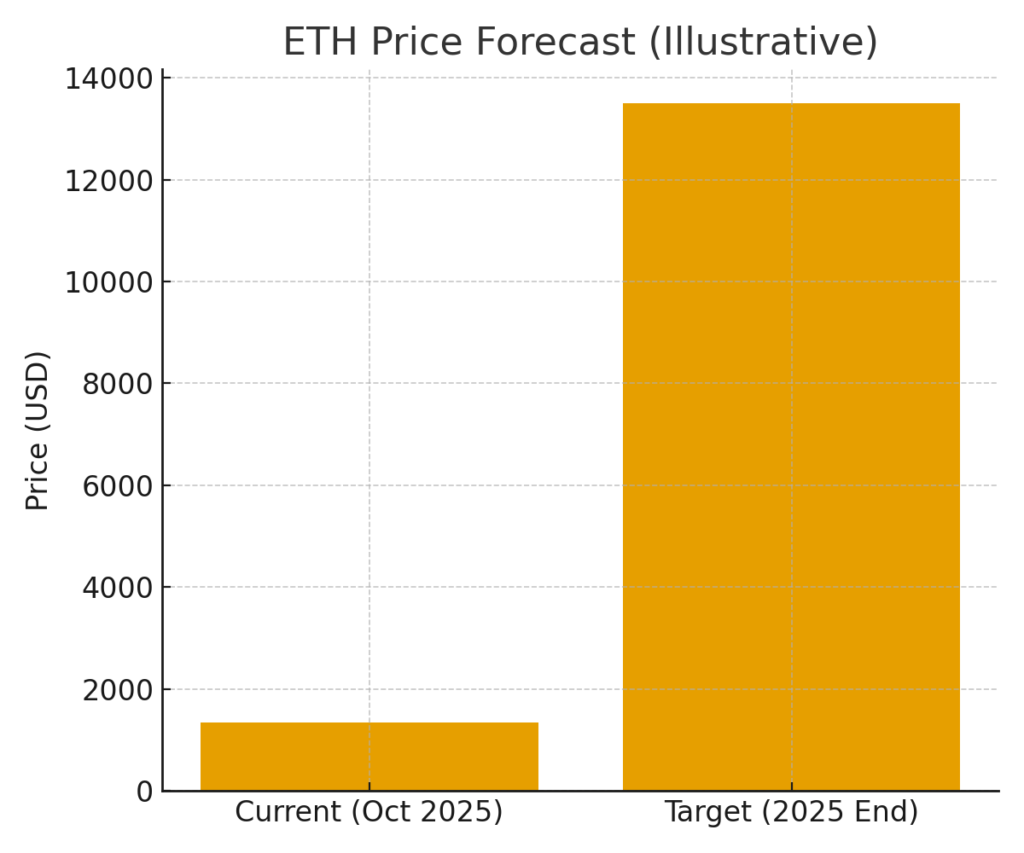

- Lee maintains a bullish outlook on Ethereum, forecasting a year-end 2025 price of US$12,000–15,000, and even suggesting Ethereum could flip Bitcoin in market-cap dominance akin to how equities overtook gold.

- Despite the accumulation hype, Lee warns that the broader “digital asset treasury” (DAT) sector is experiencing a valuation bubble collapse, with many firms trading below their net-asset-value (NAV).

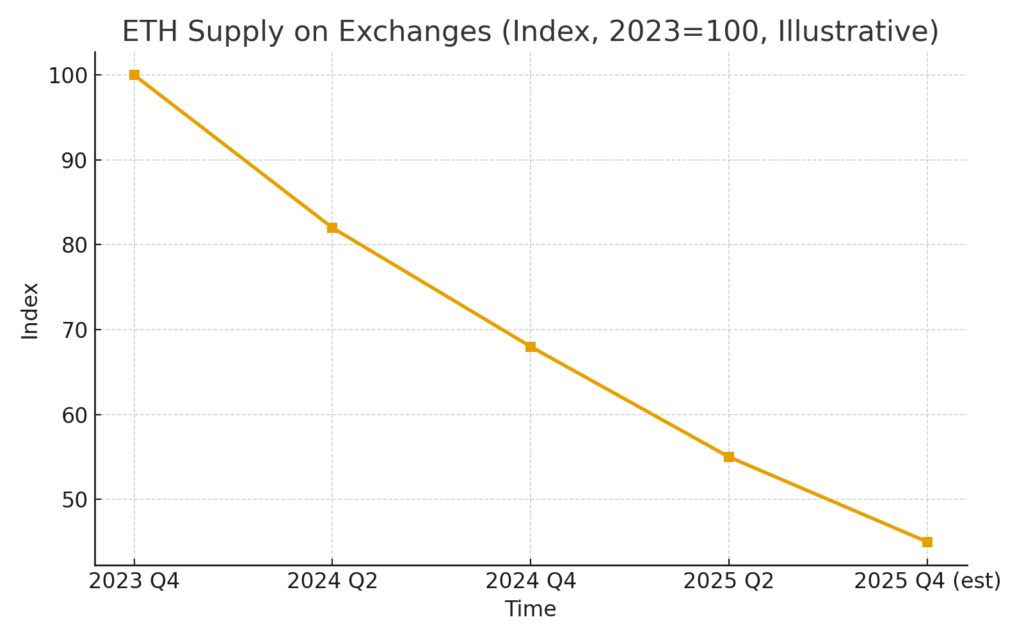

- On-chain metrics reveal exchange reserves of ETH are at a three-year low, supporting the thesis that long-term holders are hoarding rather than liquidating, which may tighten supply and support future upside.

- Practical implications for blockchain and crypto practitioners: the accumulation tide may set the stage for renewed infrastructure deployment in DeFi, tokenisation and secondary use-cases on Ethereum, making ETH not just a speculative asset but a foundational layer.

Institutional Accumulation: From Bear Market to Strategic Build-Up

Over the past few weeks, a notable shift has emerged in crypto markets: large-scale institutional players are accumulating Ethereum at the fringes of what appears to be a prolonged correction. This is not mere retail FOMO, but coordinated accumulation by treasury-style firms.

For instance, BitMine — under Tom Lee’s stewardship — purchased at least 202,037 ETH during a recent downturn, paying around US$828 million at the then‐prices. The company’s total Ethereum stash has now climbed to more than 3.03 million ETH, which represents roughly 2.5 % of the total supply. The timing is notable: accumulation occurred immediately after a major liquidation event which erased more than US$19 billion of crypto leveraged positions.

Why is this important? Because it suggests that major actors are using weakness to build infrastructure positions rather than chasing momentum. As Lee put it, “volatility creates deleveraging … this creates advantages for investors, at the expense of traders”. n essence, the narrative is shifting: instead of trading the swings, some are acquiring long-term stakes.

From the perspective of someone scanning for the next income-stream or infrastructure play, this matters. Accumulation by institutional actors often precedes broader uptake in use-cases (staking, tokenisation, DeFi) which can generate real yield or utility beyond mere appreciation.

Tom Lee’s Bullish Ethesis: Ethereum as the Future Financial Layer

Tom Lee remains one of the most vocal institutional bulls on Ethereum, and his thesis spans multiple axes of blockchain utility and macro narrative.

First, Lee argues that Ethereum could flip Bitcoin in market cap, much as equities overtook gold after the Nixon shock in 1971. In an interview, he said:

“Ethereum could flip Bitcoin similar to how Wall Street and equities flipped gold post-71.”

The logic: as “everything becomes tokenised” (stablecoins, securities, real‐world assets), the infrastructure of choice will be Ethereum, given its first-mover status, smart-contract ecosystem, and institutional tooling. Lee emphasises that he remains bullish on Bitcoin as well, but that the asymmetric upside skews to Ethereum in the next phase.

Second, Lee forecasts a year-end 2025 price target of US$12,000 to US$15,000 for ETH, driven by three key factors:

- Declining interest rates and risk-premium compression leading to increased risk-asset appetite.

- A shrinking effective supply of Ethereum due to staking, off-exchange holdings, and on-chain burn mechanics (e.g., EIP-1559). Though not explicitly quantified in the referenced articles, the off‐exchange accumulation accounts for a supply-tightening narrative.

- Large-scale institutional adoption (treasuries, tokenised assets, DeFi infrastructure) raising the floor of value and participation.

For someone in practical blockchain/crypto usage: this is an important call-to-action. If infrastructure deployment and institutional adoption increase, then access to Ethereum’s staking rewards, participation in tokenised asset protocols, or leveraging its role in finance could become relevant revenue streams rather than pure speculation.

Market Metrics & Supply Signals: Moving From Hand-to-Mouth Trading to Hodling

Beyond narrative, the on-chain data supports the view that we may be entering a structural regime shift in Ethereum’s holder base.

According to CryptoSlate, exchange reserves of ETH have fallen to their lowest level in three years, a sign that major actors are removing supply from liquid trade and parking it in cold wallets. n parallel, institutional holdings (corporate treasuries + Ethereum ETF-type vehicles) are estimated to hold more than 12.8 million ETH, or over 10 % of total supply.

Why does this matter? Because when large portions of supply move off‐exchange (less available to be sold quickly) and custodians hodl for long periods, it tends to reduce market liquidity and increase sensitivity to new inflows/outflows. This dynamic can favour sustained up-moves, especially if utility (staking, DeFi activity, tokenisation) also begins to scale.

For a crypto practitioner looking for income streams: lower supply liquidity + increasing utility = potential for staking/earnings to increase. If fewer tokens are circulating, the yield from staking becomes more attractive in relative terms, assuming protocol economics remain stable.

Treasury Sector Warning: Many DATs Are Under Pressure

While Lee and BitMine are bullish, Lee also sounded a cautionary note about the broader DAT (digital asset treasury) sector. In his words, the bubble has already burst: many DAT companies are trading below the net asset value (NAV) of their crypto-holdings.

This dichotomy is worth noting:

- On one hand, accumulation of Ethereum by credible institutional actors is growing.

- On the other, many treasury vehicles chasing speculative crypto positions are faltering, raising questions around valuation, sustainability, and business model viability.

For practitioners, the takeaway is: not all “crypto yield streams” built on treasury accumulation are created equal. It’s important to distinguish between entities with critical mass, institutional structure, and infrastructure (like BitMine) versus smaller speculative vehicles that may be vulnerable to liquidation or valuation collapse.

This sentiment underscores an important criterion when seeking new revenue sources: focus on protocols or entities with strong fundamentals, real-world utility, and institutional backing — not just speculative treasury allocations.

Practical Implications for New Crypto Income Sources & Blockchain Utilisation

Given the above dynamics, what does this mean in actionable terms for someone exploring new crypto assets, revenue sources or blockchain-driven business/operational models?

1. Staking participation on Ethereum:

With institutional accumulation increasing and supply being locked, staking ETH (or partaking indirectly via liquid staking tokens) may offer relatively attractive yields, especially if utilisation of the network continues to grow.

2. Tokenisation and DeFi infrastructure:

Lee’s thesis assumes that tokenisation (real-world assets, securities, receivables) and DeFi will expand atop Ethereum. Practically, that means opportunities in:

- Protocols issuing tokenised assets on Ethereum.

- Service providers building infrastructure (wallets, custody, compliance) for institutions entering Ethereum ecosystem.

- Yield strategies bundling tokenised assets + staking + lending on Ethereum.

3. Monitoring supply and holder dynamics:

Tracking on-chain metrics (exchange reserves, cold-wallet accumulation, institutional holdings) can help evaluate when a token is moving from speculation to infrastructure asset. ETH’s recent drop in exchange reserves is a useful indicator.

4. Cautious approach to treasuries/vehicles:

While some treasury firms are strong, many others may face valuation risk. If you’re allocating capital or selecting a yield vehicle, diligence around business model, underlying assets, custody risk, regulatory compliance matters.

5. Altcoin/infrastructure arbitrage under new regime:

If Ethereum is entering a “super-cycle” as Lee suggests, there may be opportunities not just in ETH but in protocols enabling Ethereum’s infrastructure expansion (layer-2 solutions, staking derivatives, tokenised real‐world-asset platforms). That said, these carry higher risk and one should carefully evaluate.

Recap and Conclusion

In sum: the recent heavy accumulation of Ethereum by a major institutional actor (BitMine under Tom Lee) signals potential structural change in the crypto ecosystem. Rather than a purely speculative move, this appears to be strategic infrastructure positioning. Concurrently, on-chain metrics (low exchange reserves, large institutional holdings) back the thesis that Ethereum is migrating from a trading asset to a foundational infrastructure asset.

Lee’s bullish forecast (US$12,000–15,000 by year-end) and his narrative about Ethereum potentially flipping Bitcoin stem from the belief that tokenisation, DeFi and real-world-asset issuance will increasingly live on Ethereum. For anyone seeking new crypto revenue streams or blockchain applications, the implication is clear: this is a moment to consider participation not only in the token (ETH) itself, but also in the supporting infrastructure (staking, tokenisation, institutional access). At the same time, caution is warranted: many treasury vehicles are under pressure, and not every yield opportunity is created equal.

Ultimately, whether you’re exploring new crypto protocols, building blockchain-driven business models, or simply looking for meaningful participation in the shift, the Ethereum narrative today is less about short‐term trading and more about long‐term structural adoption — and institutional accumulation may be the early signpost.