Main Points :

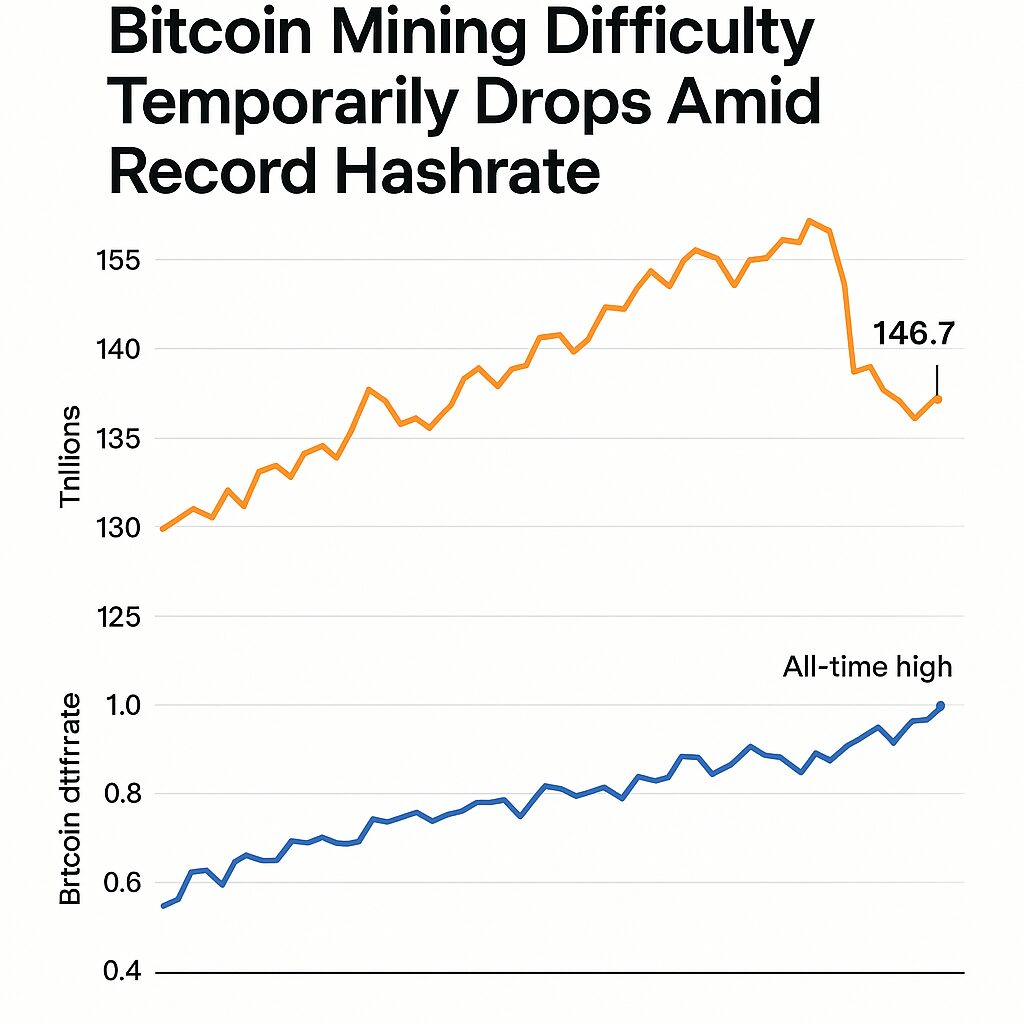

- Bitcoin (BTC) mining difficulty fell to ~146.7 trillion, down ~2.7 % from its previous all-time high.

- Network hashrate concurrently hit a new peak of over 1.2 trillion hashes per second (≅1,200 EH/s) and remains elevated.

- The next difficulty adjustment (estimated ~29 October 2025) is projected to raise difficulty to ~156 – 157 trillion.

- Miners face higher competition, hardware/energy pressure, and are increasingly diversifying into alternative revenue streams (AI data-centres, HPC).

- Supply-chain and trade-policy headwinds (e.g., tariffs, export controls) remain significant risks for mining operations.

1. Mining Difficulty Drop — A Short-lived Relief

In recent data the Bitcoin mining difficulty — the metric that gauges how hard it is to mine the next block in the proof-of-work chain — fell to approximately 146.7 trillion. This marks about a 2.7 % drop from the previous all-time high of ~150.8 trillion reached in the prior adjustment period.

This drop gives miners a brief window of slightly easier block production, potentially easing some of the pressure in a tough operating environment: falling BTC prices, rising energy/share costs and stiff competition. It signals that block generation had slowed slightly in the preceding epoch, triggering the network’s built-in difficulty downward adjustment.

However, this easing is likely temporary. The network is in fact seeing elevated activity, and forecasts point to another upward difficulty adjustment in short order. The drop in difficulty should not be mistaken for a structural shift in the mining business — rather a very short-term relief valve.

2. Hashrate at Record High — Competition Remains Fierce

At the same time that difficulty fell, the network’s hashrate — the total computation power deployed by miners worldwide — surged to new heights. Reports indicate readings above 1.2 trillion hashes per second (≈1,200 exahashes per second, or EH/s) in recent days.

This dual phenomenon — difficulty down while hashrate up — means that many new miners (or upgraded rigs) have come online, pushing the network’s processing power higher even if block production momentarily slowed. The higher the hashrate, all else equal, the more competition for the same block rewards, which typically drives down per-rig profitability.

In brief: miner competition is more intense than ever. Even as difficulty gave a small respite, the hashrate backdrop suggests mining remains a battle for scale, cost-efficiency, access to cheap energy, and high-throughput rigs.

3. What’s Coming: Next Difficulty Adjustment & What It Implies

Looking ahead, the next difficulty change for Bitcoin is estimated for October 29-30, 2025 (UTC), with projections pointing to a difficulty increase from ~146.7 T to ~155-157 T (an increase in the order of ~6-7 %).

If this comes to pass, the “ease” provided by the recent drop will be reversed, and miners will face a tougher environment again. For prospective investors or operators this translates into several implications:

- Margins will continue to be under pressure unless BTC price and/or block reward flips beneficially.

- Hardware with lower efficiency may be squeezed out.

- Larger miners with access to cheap power, large scale, and efficient rigs may further consolidate advantage.

- For those exploring alternate revenue models (see next section): the urgency for diversification escalates.

4. Miners Diversify — From Mining to AI & High-Performance Computing

With margin pressure mounting, many mining firms are pivoting or expanding into adjacent business lines. According to recent analysis, companies such as Core Scientific, Hut 8 and IREN (previously Iris Energy) are reallocating resources toward AI data-centres and high-performance computing (HPC) in 2024 and beyond.

These moves make sense when considered through the lens of mining’s current cost structure: the key inputs are capital (for rigs), energy (for operation), cooling/infra and time. AI/HPC workloads likewise demand massive computing, cooling, power, and infrastructure — meaning mining operators can repurpose or co-locate gear, leverage their data-centre knowledge and power contracts, and thereby reduce exposure to pure-mining risk.

At the same time, this strategic shift comes with its own friction: AI and mining operations compete for the same cheap power sources, which means the energy supply environment (geography, regulatory, grid access) becomes even more crucial. As one article put it: “miners and AI-infra players are competing for cheap electricity.”

For investors in crypto/blockchain, this signals that mining firms may increasingly be viewed not purely as “Bitcoin miners” but as broader “compute infrastructure” companies — and blockchain investors might want to evaluate such firms beyond just hash-rate metrics.

5. Supply-Chain & Policy Risks — More Than Just Mining Costs

Broadly speaking, the mining ecosystem isn’t just buffeted by energy and competition, but also by geopolitical, regulatory and supply-chain factors. For example:

- US-China trade tensions, tariff regimes and export controls can raise the cost of mining hardware (ASICs, chips) in affected jurisdictions.

- Regions subject to equipment import tariffs face competitive disadvantage relative to regions without such duties.

- If export controls on processors/chips tighten further (e.g., for tech linked to cryptography or HPC), procuring rigs may become even more expensive or delayed.

For those considering entering mining, or investing in companies doing so, these policy/geo risks are real and should factor into capital-expenditure assumptions, time-to-profit, region of operation, and contingency planning.

6. Implications for New Crypto Assets & Blockchain Use-Cases

While the above is specific to Bitcoin mining, the ripples extend into broader blockchain/crypto investment and application layers:

- For investors hunting new crypto assets, the shifting dynamics of mining (difficulty increase, hashrate scale) mean that Proof-of-Work (PoW) blockchains may face higher entry barriers. This can favour those who invest early in low-difficulty chains, niche PoW coins, or alternative consensus models (Proof-of-Stake, Proof-Elapsed, etc).

- For practitioners interested in blockchain practical uses (beyond mining), these developments highlight the evolving infrastructure cost envelope for securing decentralised networks. As mining becomes more expensive and concentrated, decentralisation might erode unless offset by innovation (efficient consensus, layer-2 roll-ups, hybrid models).

- For alternative revenue/investment strategies: mining companies moving into AI/HPC infrastructure may represent “crypto-adjacent” opportunities for returns — especially if you see them as winning compute-infrastructure plays rather than pure crypto bets.

- For DeFi/or other blockchain networks considering launching or hooking into PoW systems: the above signals one should model realistically high hashrate growth, hardware cost escalation and regional energy constraints — going “cheap” may not be sustainable for network security.

7. Key Takeaways for Investors & Operators

- The current drop in difficulty is temporary relief, not a structural turnaround — expect difficulty to resume rising.

- Rising hashrate and intensifying competition means economies of scale and low energy cost will increasingly define winner-miners.

- Diversification (into AI/HPC or alternative use of infrastructure) is more important than ever for miners. Investors should check how mining firms are positioned.

- Policy and supply-chain risks are real and can materially affect profitability and asset-allocation decisions.

- For explorers of new coins/use-cases: mining economics matter — for PoW-based systems the underlying infrastructure cost is a strategic consideration, and for non-PoW systems the shifting context of crypto infrastructure offers insights.

- For blockchain practitioners: rising cost of decentralised security means it’s worth re-thinking consensus economics, network design and long-term viability.

Conclusion

In summary, the recent drop in the Bitcoin mining difficulty to ~146.7 trillion offers a fleeting respite to miners amid sustained record-hashrate levels. But the real story is the elevated competition, infrastructure demands and strategic pivots of miners as they navigate margin pressure, regulatory headwinds and hardware-capex challenges. For new crypto-asset hunters and blockchain implementers, the takeaway is clear: mining economics matter — whether you’re investing in the next alt-coin, building a decentralised network or simply analysing infrastructure companies in the crypto space. While mining may appear to offer a breather, the uphill climb of cost, competition and compliance remains very much intact.