Key Takeaways :

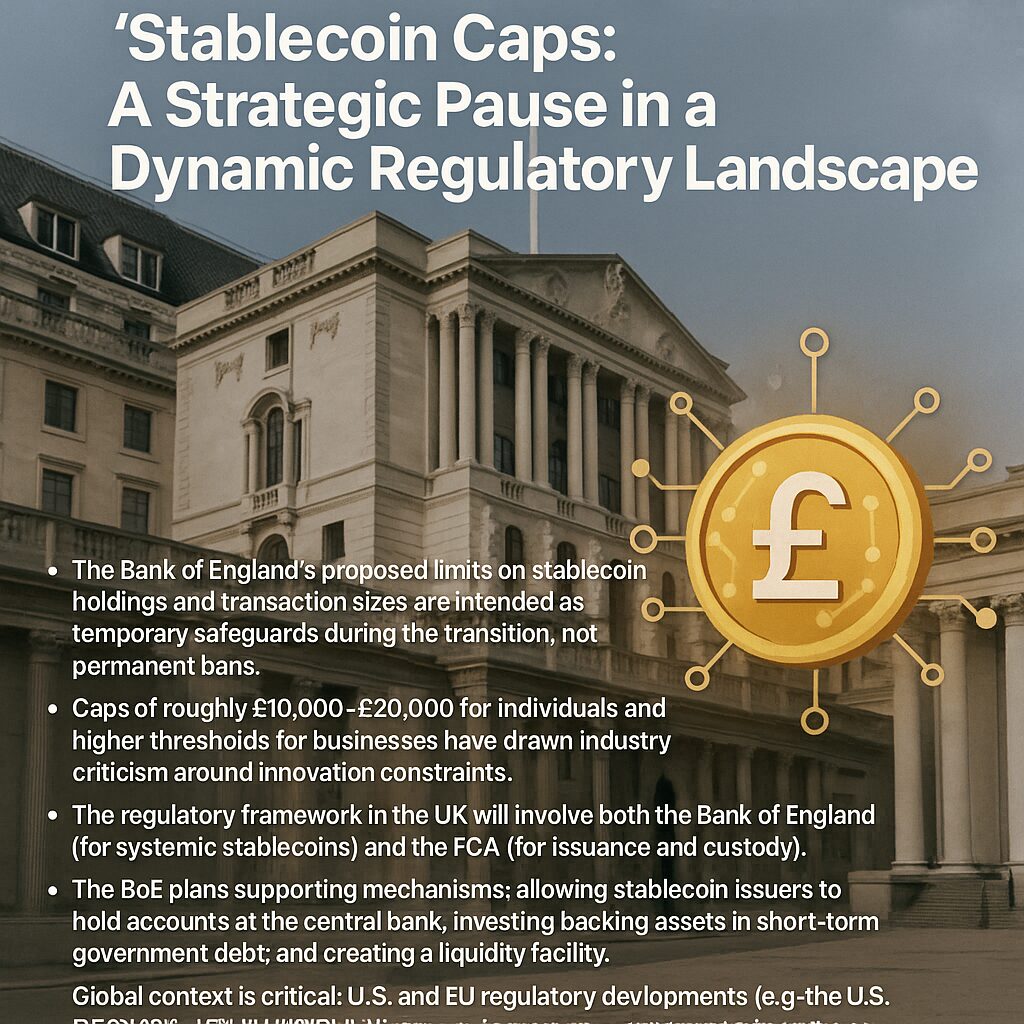

- The Bank of England’s proposed limits on stablecoin holdings and transaction sizes are intended as temporary safeguards during the transition, not permanent bans.

- Caps of roughly £10,000–£20,000 for individuals and higher thresholds for businesses have drawn industry criticism around innovation constraints.

- The regulatory framework in the UK will involve both the Bank of England (for systemic stablecoins) and the FCA (for issuance and custody).

- The BoE plans supporting mechanisms: allowing stablecoin issuers to hold accounts at the central bank, investing backing assets in short-term government debt, and creating a liquidity facility.

- Global context is critical: U.S. and EU regulatory developments (e.g. the U.S. GENIUS Act, EU’s MiCA) influence competitive positions and regulatory alignment.

- For innovators and investors, the UK’s phased approach offers both risks and opportunities—especially for compliant stablecoin models and blockchain use in financial services.

1. Introduction: Stability vs. Innovation in the Stablecoin Era

In October 2025, the Bank of England (BoE) made headlines by clarifying that its intention to impose limits on stablecoin holdings and transaction volume was a temporary measure meant to cushion the financial system during a transitional phase. Deputy Governor Sarah Breeden emphasized that these constraints will be eased or removed as soon as the BoE is confident that credit flow to households and businesses isn’t being undermined.

To those seeking new crypto ventures or practical blockchain use cases, this development raises immediate questions: How will these limits affect stablecoin-based businesses in the U.K.? What is the broader regulatory trajectory? And where do comparative regimes in the U.S. and EU stand today?

In this article, I summarize the BoE’s proposal, contextualize it with recent regulatory shifts globally, and explore what these changes mean for innovation, investment, and blockchain adoption in the financial sector.

2. BoE’s Proposed Temporary Stablecoin Caps

2.1 What the Proposal Says

- The cap proposal targets “systemic” sterling-pegged stablecoins used in payments.

- Suggested limits are in the range of £10,000 to £20,000 per individual user (≈ $13,400 to $26,800)

- For businesses or larger users, higher thresholds (potentially up to £10 million) are being considered.

- The BoE is clear that it intends these caps to be temporary—they will be lifted once the central bank believes the transition poses no threat to the supply of credit.

- The BoE also plans to consult publicly, solicit feedback from industry participants, and possibly exempt certain entities (e.g. those participating in “sandbox” programs or large corporate users) from the caps.

2.2 Central Bank’s Concerns

The BoE’s caution arises from the risk that a rapid shift of deposits from traditional banks into stablecoins might destabilize credit markets:

- In the U.K., much of the economy depends on bank-based lending. A large outflow toward stablecoins could hamper banks’ ability to extend credit.

- The central bank sees the caps as a way to monitor adoption rates, gauge systemic impact, and enable a smoother transition to a multi-money environment.

- To support the stablecoin ecosystem under control, the BoE proposes some novel measures (explained in the next section).

3. BoE’s Supporting Measures: Enabling as Well as Restricting

While imposing limits might seem restrictive, the BoE is also laying the groundwork to support regulated stablecoin issuance and adoption in a safer manner.

3.1 Direct Accounts at the BoE

Unlike many jurisdictions where stablecoin issuers must rely on commercial banks, the BoE proposes providing reserve accounts at the central bank to systemic stablecoin issuers. This gives issuers a stable anchor for their backing assets.

3.2 Investment of Backing Assets & Yield

To ensure that stablecoin issuers don’t suffer from opportunity costs, the BoE is considering allowing a portion of backing assets to be invested in short-term U.K. government debt (e.g. Gilts). That way, issuers can generate modest returns while still maintaining high liquidity and safety.

3.3 Liquidity Facility / Redemptions Backstop

The central bank is also exploring a liquidity facility to backstop solvent stablecoin issuers that may face temporary redemption pressures. This would enhance confidence in redemption stability.

These supporting measures suggest that the BoE is not merely restraining stablecoin growth, but actively shaping a controlled pathway for their integration into the financial system.

4. U.K. Regulatory Architecture & Ongoing Consultations

4.1 Dual Regime: BoE + FCA

Under the proposed regime:

- The BoE will oversee systemic sterling stablecoins and potentially act as banker to such issuers.

- The Financial Conduct Authority (FCA) will regulate issuance, custody, safeguarding of crypto assets, and ensure compliance with consumer protection, AML/KYC, etc.

- The FCA’s consultation paper CP25/14 is already exploring rules on “qualifying stablecoins” and cryptoasset custody, seeking feedback through July 2025.

- H.M. Treasury and Parliament will pass secondary legislation to bring stablecoin activities formally into the regulated perimeter.

4.2 Timeline & Exemptions

- The BoE intends to offer transitional arrangements and expects to release full consultative proposals in due course.

- The U.K. is considering exemptions for sandbox participants, large businesses, or certain transaction types to balance innovation and safety.

- The U.K. also proposes exempting overseas stablecoin issuers from requiring U.K. domestic regulatory registration, which is intended to maintain openness to global players.

5. Global Context: U.S. and EU Developments

5.1 U.S. – The GENIUS Act

In July 2025, the U.S. passed the GENIUS Act, the first federal law establishing a clear regulatory framework for payment stablecoins. It mandates:

- 1:1 backing of stablecoins with high-quality liquid assets (e.g. U.S. dollars or equivalent)

- Regular audits, transparency, and oversight by federal regulators.

- Dual oversight by federal and state authorities in some instances.

The GENIUS Act increases certainty for stablecoin issuers in the U.S. and may lead to stronger alignment or competition with U.K. and EU regimes.

5.2 EU – MiCA and Pan-European Structure

- The EU’s Markets in Crypto-Assets (MiCA / MiCAR) regulation became fully applicable in stages by late 2024.

- MiCA classifies “e-money tokens” and “asset-referenced tokens” under a unified regulatory umbrella, setting reserve, redemption, and supervision rules.

- If a stablecoin issuer operates both in the EU and outside, cross-border redemption pressure is a risk—some EU watchers warn of gaps in MiCA’s cross-jurisdictional resilience.

- Notably, stablecoin issuers in Europe (e.g. Circle) have already sought compliance with MiCA by obtaining local licenses (e.g. EMI license in France) to issue USDC/EURC.

5.3 Interplay and Competitive Pressure

- The U.K. and U.S. created the Transatlantic Taskforce for Markets and the Future in September 2025 to explore regulatory convergence, particularly on stablecoins.

- The Financial Stability Board (G20 risk watchdog) recently issued a warning that global crypto regulation is inconsistent and fragmented, specifically flagging stablecoin gaps.

- Because stablecoin markets are inherently cross-border, inconsistent rules may incentivize regulatory arbitrage and pose systemic risks.

6. Implications for Innovators, Investors & Use Cases

6.1 Opportunities in the U.K.

- Firms building “qualifying stablecoins” in compliance with U.K. rules could gain first-mover advantage in a regulated environment.

- The BoE’s plan to provide account facilities and liquidity support could reduce infrastructure risk for issuer startups.

- Tokenization of real-world assets (e.g. funds, real estate) and integration with stablecoins may be more feasible in a robust legal framework. The U.K. government has already signaled support for tokenised funds.

6.2 Risks and Challenges

- The caps may deter users or push them into unregulated stablecoins or offshore products. Some industry voices argue these caps could harm the U.K.’s crypto competitiveness.

- Startups may incur compliance costs, complexity, and uncertainty until the final rules are enacted and tested.

- Cross-border redemption stress is a real concern: if a stablecoin is global but domestic regulation limits redemption, then mismatch pressures may arise.

- Until regulatory certainty is reached, some business models may be constrained—especially high-frequency, micro-payment, or DeFi-native applications.

6.3 Use-Case Signals

- Payment rails, stablecoin-enabled remittances, and programmable money may be strongest near-term use cases under stablecoin regimes.

- Tokenized funds, securities, and on-chain collateralization will likely gain traction where stablecoins act as settlement layers or “bridge money” between blockchain and legacy systems.

- Issuers focusing on low-friction compliance, transparency, and reserve quality may emerge more trusted and scalable than speculative or unbacked models.

7. Conclusion

The Bank of England’s announcement that the proposed stablecoin caps are temporary reflects a calculated, cautious approach to integrating digital money into a bank-centric financial system. Rather than a rejection of innovation, the move suggests a transitional buffer: ensuring that the adoption of stablecoins does not destabilize credit markets or undermine the lending capacity of banks.

Simultaneously, the BoE is not merely restraining growth, but actively enabling a more robust foundation—through central bank accounts for issuers, investment flexibility, and liquidity backstops. Alongside the FCA’s consultative process, the U.K. is laying the groundwork for a stablecoin regime that seeks balance between innovation and systemic safety.

Yet the U.K. doesn’t operate in a vacuum. The U.S. GENIUS Act is already providing clarity for U.S.-based stablecoin issuers, and the EU’s MiCA regime sets stringent standards across Europe. For innovators and investors, this is a moment to watch where regulatory clarity converges with competitive advantage.

If you are looking to build or invest in next-generation stablecoin or blockchain-enabled financial services, this period in the U.K. may present both constraints and openings: the constraints of caps and compliance, and the opening of a legal, supported, and somewhat predictable operating environment.

Let me know if you’d like me to dig deeper into reserve models, governance, or specific legal strategies tailored for U.K.- or EU-based stablecoin launches.