Key Takeaways :

- Ripple has formed a strategic partnership with Absa Bank, marking its first large-scale institutional custody deal in Africa.

- Absa will leverage Ripple’s custody infrastructure to offer secure, compliant digital asset storage for cryptocurrencies and tokenized assets.

- This move aligns with Ripple’s earlier African initiatives, such as stablecoin rollout (RLUSD) and payments partnerships (e.g. Chipper Cash).

- Institutional and regulatory momentum in Africa is accelerating: clearer laws, rising demand, and growing institutional interest in digital assets.

- For crypto investors or builders, Ripple’s African expansion underscores new opportunities in emerging markets for custody, tokenization, and financial infrastructure.

1. A New Custody Frontier: Why Ripple–Absa Matters

In mid-October 2025, Ripple officially announced a strategic partnership with Absa Bank, one of South Africa’s leading financial institutions, to provide institutional-grade digital asset custody for Absa’s customers. This marks Ripple’s first major custody client in Africa, expanding its global custody network into the continent.

Through the partnership, Absa will deploy Ripple’s custody technology to securely hold cryptocurrencies and tokenized assets, with safeguards aimed at meeting high standards of security, compliance, and operational robustness. Ripple frames this as a response to growing demand among financial institutions in emerging markets for reliable digital asset infrastructure.

Ripple’s leadership describes the deal as a signal: “Africa is experiencing a major shift in how value is stored and exchanged,” and their collaboration with Absa underscores a deepening commitment to unlocking digital asset opportunities on the continent.

1.1 Why Absa? Strategic Fit and Reach

Absa Group is among Africa’s largest and most established banking institutions, with a diverse footprint across multiple African markets. Its reputation and client base make it an ideal partner for Ripple’s ambition of mainstreaming regulated digital asset services.

Absa’s internal leadership has highlighted the necessity of evolving with the financial ecosystem. In a statement, Absa’s Head of Digital Product, Custody, Robyn Lawson noted that leveraging Ripple’s custody solution allows the bank to provide “secure, compliant, and robust” infrastructure that meets the highest standards.

Thus, the partnership does more than just enable custody: it positions Absa as a pioneer in regulated crypto services in Africa, potentially influencing other banks to follow suit.

2. Ripple’s Growth Playbook in Africa

This custody announcement is part of a broader, multi-pronged strategy by Ripple to deepen its footprint in Africa.

2.1 From Payments to Stablecoin to Custody

Earlier in 2025, Ripple had already signaled its commitment to Africa:

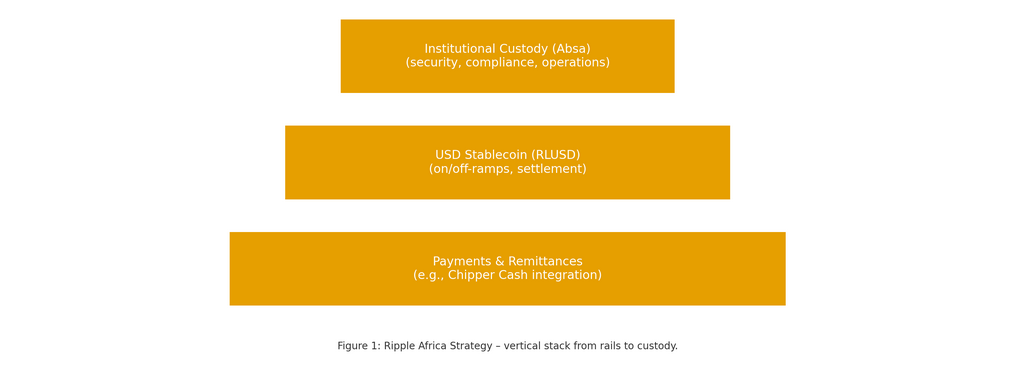

- Payments & remittance support: Ripple partnered with Chipper Cash, a pan-African payments provider, to enable crypto-enabled cross-border transactions on the continent.

- Stablecoin rollout: Ripple’s USD-backed stablecoin, RLUSD, has been introduced in African markets through regional partners such as Chipper Cash, VALR, and Yellow Card.

- Custody expansion: The Absa deal brings custody into the African narrative, effectively completing a backend infrastructure stack—payments, token issuance, and secure storage.

This vertical integration—from transaction rails to stablecoins to custody—gives Ripple the ability to offer comprehensive infrastructure to financial institutions in emerging markets.

2.2 Global Consistency, Local Sensitivity

Ripple’s custody ambitions are not limited to Africa. The company has been steadily building its global custody network across Europe, the Middle East, Asia-Pacific, and Latin America.

Notably, this expansion is backed by compliance, licensing, and regulatory readiness. Ripple claims over 60 regulatory licenses and registrations globally and positions its solutions as scalable, secure, and standards-compliant.

By integrating local banks such as Absa, Ripple gains local credibility and distribution, allowing its infrastructure to anchor in each market rather than operating purely as an offshore provider.

3. African Institutional Momentum and Regulatory Developments

The Absa partnership arrives amid accelerating institutional and regulatory momentum across Africa’s crypto space.

3.1 Regulatory Clarity is Emerging

Several African countries have recently introduced or passed laws to define and regulate digital assets:

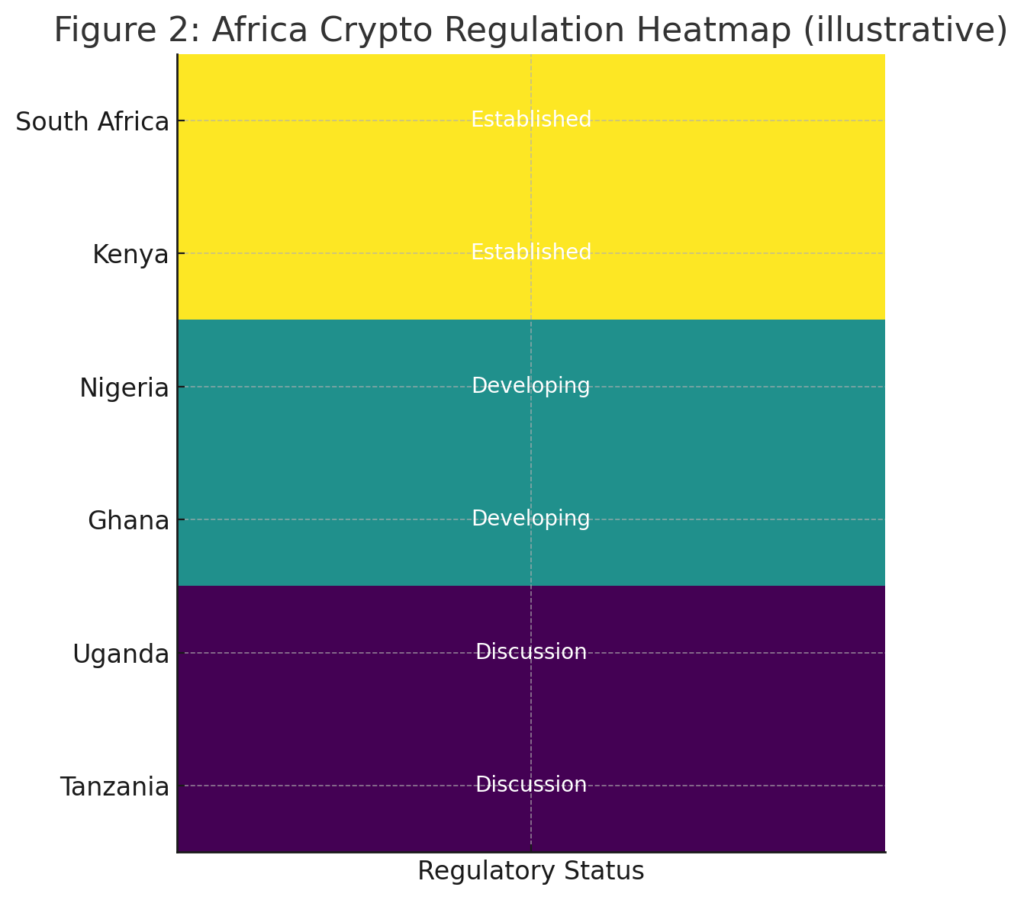

- Kenya: As of October 13, 2025, the Kenyan parliament approved the Virtual Asset Service Providers Bill. The bill places the Central Bank in charge of licensing stablecoins and virtual assets, while crypto exchanges and trading platforms fall under the purview of the Capital Markets Authority.

- South Africa (already relatively more mature): The country has existing regulatory frameworks that allow for crypto services under controlled settings, making it among the more favorable environments in Africa for fintechs.

- Other jurisdictions: Across Africa, governments and regulators are increasingly clarifying rules for digital assets, recognizing both the risk and economic potential of blockchain-based finance.

This regulatory maturation reduces one of the major barriers to institutional adoption—regulatory uncertainty.

3.2 Rising Institutional Demand

With clearer regulation, institutional players—such as banks, asset managers, and fintechs—are showing greater appetite for blockchain-enabled services.

- The Absa deal itself is a testament to demand: traditional banks are no longer merely observing but actively integrating digital asset infrastructure.

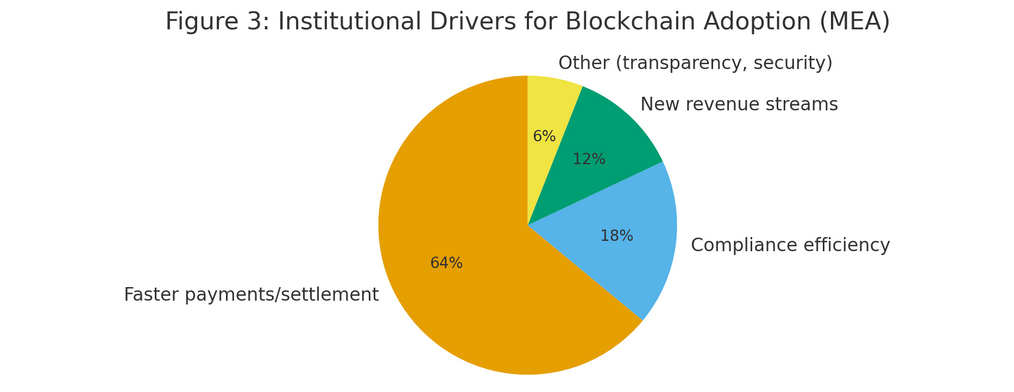

- Ripple cites a statistic: 64 % of finance leaders in the Middle East and Africa believe that faster payments and settlement are key drivers for adopting blockchain-based currencies.

- Institutional-grade custody is especially important because security, compliance, auditability, and regulatory assurance are prerequisites for large players to move capital into crypto.

As these institutional players come online, demand for reliable custody, tokenization platforms, and regulatory-compliant rails will grow.

4. Implications for Crypto Investors, Builders, and New Projects

For those searching for new crypto projects, yield opportunities, or practical blockchain use cases, the Ripple–Absa partnership (and its context) offers several lessons and potential plays.

4.1 Custody as Infrastructure Opportunity

Secure institutional custody is a key infrastructural bottleneck. Many promising asset tokenization, DeFi, and digital securities platforms struggle with custody integration in regulated environments. The fact that a major crypto firm like Ripple is pushing hard into custody underscores the business potential in this domain.

If you are developing a tokenized asset, security token offering, or digital finance product in emerging markets, partnering or integrating with institutional custody solutions (Ripple’s or others) can be a differentiator.

4.2 Tokenization and On-Chain Financial Products

With stablecoins (like RLUSD), reliable custody, and payments rails in place, the next frontier is the creation of on-chain financial instruments tailored for African markets—such as tokenized bonds, asset-backed tokens, on-chain lending, regional stablecoins, or cross-border trade finance tokens.

Because infrastructure is being built out, there is room for niche projects focused on regional compliance, liquidity aggregation, or bridging local fiat systems to on-chain ecosystems.

4.3 Regional First Movers Will Capture Value

Projects that can localize—for instance, adapting token models to South Africa or Kenya, partnering with local banks, or bridging regulatory gaps—may have a head start. Many global crypto projects compete for the same sandboxed audience; but projects able to tailor to Africa’s legal, cultural, and institutional landscape could gain a lasting edge.

4.4 Risks and Considerations

- Regulatory shifts: While clarity is improving, sudden regulatory changes (e.g. bans, taxation, capital controls) remain possible in many African jurisdictions.

- Execution complexity: Integrating custody, compliance, and local banking systems is nontrivial. The Ripple–Absa partnership will need robust governance, auditing, security, and legal alignment.

- Market depth & liquidity: For tokenized assets to be viable, they must be tradable. Many African markets still lack deep liquidity in crypto instruments.

- Operational/technical risk: Custody services must maintain high uptime, security, disaster recovery, and key management. Any lapses would harm trust.

5. Looking Ahead: Trends & Forecasts

- More bank–crypto partnerships in Africa: Ripple’s deal with Absa may inspire other African banks to seek custody or fintech tie-ups, creating a snowball effect.

- Expansion to adjacent African markets: Countries like Nigeria, Kenya, Ghana, and others may see local custody-enabled banking or tokenization pilots.

- Rise of local stablecoins and CBDCs: As stablecoins like RLUSD gain usage, local fiat-pegged tokens or central bank digital currencies (CBDCs) may integrate with custody infrastructure.

- Cross-border tokenized trade: With better custody and payments rails, tokenizing trade finance, letters of credit, or remittances across African borders becomes more feasible.

- New yield and DeFi models adapted to regional settings: DeFi protocols might localize lending, staking, or structured products for African users, leveraging custody-backend systems.

Conclusion

Ripple’s custody partnership with Absa Bank marks a major inflection point in crypto adoption in Africa. By anchoring digital asset custody in one of the continent’s largest banking institutions, Ripple is integrating into the institutional fabric of African finance, not merely overlaying crypto on the sidelines.

For builders, investors, and crypto-native teams, this development signals that the “plumbing” for institutional digital finance is being laid. Custody, tokenization, and compliant rails are no longer abstract ambitions—they’re being deployed in real markets.

If you’re exploring new projects or investments, consider how your concept might leverage or integrate with emerging institutional custody infrastructure. Partnering early, localizing your approach, and aligning with regulatory momentum could position you to ride the next wave of blockchain adoption across Africa—and perhaps in other emerging markets.