Main Points :

- Citi plans to launch a crypto asset custody service in 2026, combining in-house technology and third-party partnerships.

- The move illustrates growing confidence by legacy financial institutions in digital assets under evolving regulatory regimes.

- Institutional demand for secure, regulated custody services is rising sharply, with many investors pledging significant allocation to crypto.

- The competitive landscape includes established crypto custodians, other banks entering the space, and innovations in tokenization and real-world assets.

- For crypto explorers and blockchain practitioners, understanding the design tradeoffs, regulatory constraints, and institutional buyers will be key for spotting the next opportunities.

Citi’s Crypto Custody Ambition: What Has Been Announced

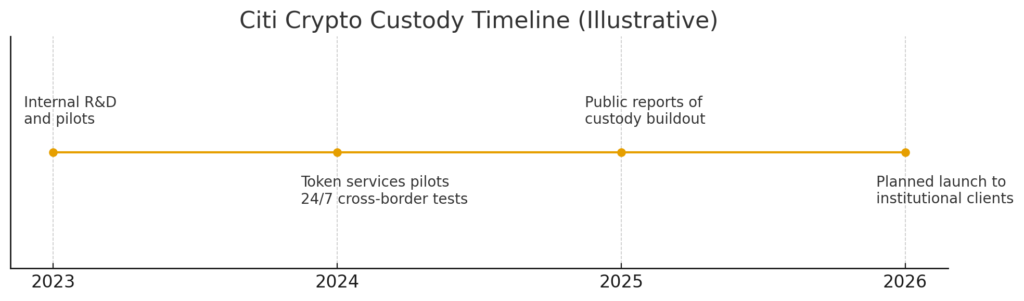

Citi, one of the largest legacy banks globally, has disclosed plans to launch a full crypto custody service in 2026. According to Biswarup Chatterjee, head of global partnerships and innovation, the bank has been quietly building this over the past two to three years.

The bank intends to offer the service to institutional clients—particularly asset managers and large financial players. Citi is reportedly considering a hybrid model: developing some core custody infrastructure in-house while also partnering with specialized third-party custodians to augment capabilities and assure security. In parallel, Citi continues to advance its tokenization and digital payments initiatives—for example, its “Citi Token Services,” which facilitate 24/7 blockchain-based dollar transfers across global branches.

Notably, Citi is also exploring issuance of its own stablecoin, and more generally its strategy seems to embrace digital deposits and tokenized real-world assets as adjacent domains of growth.

By entering this arena, Citi aims to compete more directly with major crypto-native players and position itself as an institutional bridge between traditional finance and decentralized infrastructure.

Citi’s announcement also contrasts with JPMorgan’s more cautious stance. While JPMorgan now permits clients to invest in crypto, CEO Jamie Dimon has publicly resisted offering custodial services. However, some analysts believe JPMorgan may revisit its stance in future years as institutional demand intensifies.

Rising Institutional Demand & Capital Allocation

One of the strongest tailwinds for custody is the accelerating adoption of digital assets by institutions. In 2025, surveys show that over 59 % of institutional respondents plan to allocate more than 5 % of their assets under management (AUM) into crypto or digital assets. Another report suggests that more than 75 % of institutional investors intend to increase digital asset allocations during the year.

This shift is not just speculative: many institutions view digital assets and tokenized instruments as strategic infrastructure plays, diversifiers, and sources of yield generation or liquidity.

State Street, a leading custody and fund services provider, recently published a report emphasizing that digital assets have matured beyond niche experimental tools and are now becoming part of the institutional playbook.

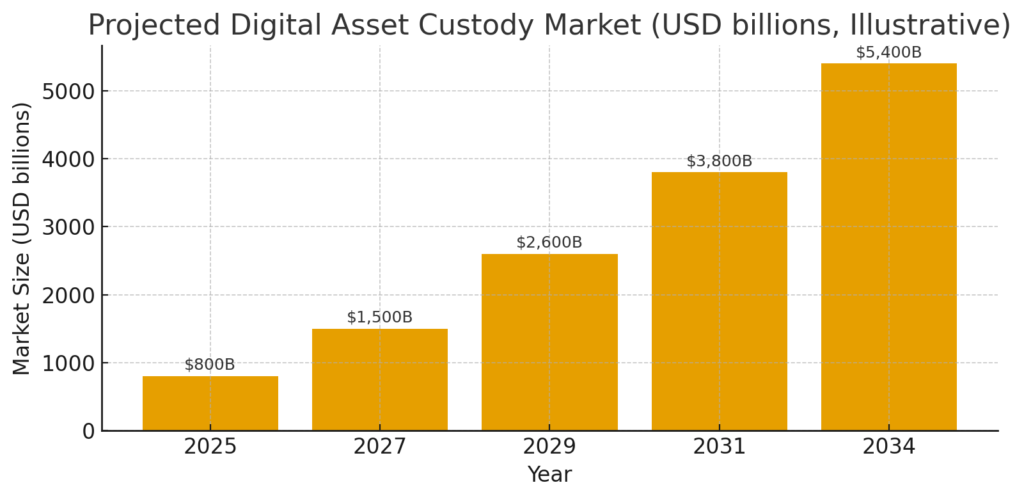

In parallel, the digital asset custody market is projected to expand massively: one estimate forecasts it could reach USD 5,436 billion (i.e. over 5.4 trillion USD) by 2034, driven by institutional demand, regulatory clarity, and technical maturation.

Regulatory Shifts and Legitimacy

Citi’s entry is buoyed by evolving regulation. In the U.S., the passage of the GENIUS Act has opened opportunities for regulated stablecoin issuance by banks, which may strengthen the case for financial institutions to internalize digital asset infrastructure. In the European Union, MiCA (Markets in Crypto-Assets Regulation) has already come into force (as of mid-2024), creating a harmonized regulatory regime for many crypto asset classes. These regulatory frameworks reduce counterparty risk, increase legal clarity, and lower friction for mainstream entities entering crypto custody.

What’s more, in Europe Deutsche Börse’s Clearstream recently announced that it will begin offering Bitcoin and Ether custody and settlement services for institutional clients. That move signals that legacy financial infrastructure providers are embracing crypto custody as part of their service expansion.

Competitive Field: Crypto Native Custodians and Hybrid Players

The custody space already features established crypto-native players such as BitGo, Coinbase Custody, and others. BitGo, in particular, is notable because it recently filed for a U.S. IPO—the first crypto custodian to do so. Its offerings include multi-signature wallets and combinations of hot and cold storage configurations, with robust risk controls.

Crypto firms also specialize in innovations such as multi-party computation (MPC), threshold signatures, hardware security modules (HSMs), and on-chain proof-of-reserve to enhance transparency. The best custodians now seek to meet institutional grade audits, insurance coverage, segregated asset accounting, and compliance with KYC/AML regimes.

Thus, Citi must differentiate itself in a space that already prizes security, performance, transparency, and regulatory compliance. The hybrid strategy (mixing in-house infrastructure with third-party partnerships) is likely intended to accelerate time-to-market and pool best-of-breed capabilities.

Key Technical, Business & Design Considerations for Institutional Custody

For practitioners and those seeking the next crypto opportunity, the inner workings of custody matter—beyond mere headline announcements. Below are some core dimensions to watch:

1. Custody Architecture: Hot, Cold, MPC, Threshold Signatures

- Cold storage (offline, air-gapped hardware) remains the gold standard for securing large, long-term holdings.

- Hot wallets provide liquidity and transaction speed, but with greater exposure to attack vectors.

- Multi-party computation (MPC) and threshold signature schemes allow distributing signing authority across nodes without reconstructing the full private key. These architectures balance continuous operation with cryptographic safety.

- The choice among these modes involves designing for tradeoffs among security, uptime, latency, governance, and cost.

Citi’s decision to keep parts in-house likely concerns controlling the key operations infrastructure. At the same time, partnering with existing proven custody providers can mitigate risk and accelerate deployment.

2. Proof-of-Reserve, Auditability, and Transparency

Institutions demand verifiable assurances that their assets are held securely and are not commingled or misreported. Thus, proof-of-reserve systems, on-chain attestations, and independent audits are increasingly considered non-negotiable.

Citi, launching into a more regulated environment, will likely adopt robust auditing standards, index asset segregation, and transparent reporting to build trust with clients and regulators.

3. Compliance, Regulation & Legal Safeguards

Custodians must comply with anti-money-laundering (AML), know-your-customer (KYC), sanctions screening, and data privacy regimes. The regulatory environment — including differing rules per jurisdiction — is a key challenge.

Banks like Citi have advantages here: they already operate under heavy regulatory oversight, have compliance infrastructure, and possess established relationships with regulators. This can make them more credible as custodians. But domain-specific controls (crypto-specific custody risk, smart contract risk, cross-chain risk) must be layered on top.

4. Integration & API Ecosystems

One selling point for institutional clients is the ability to integrate custody APIs, reporting systems, and operational automation into their workflow (trading systems, fund accounting, treasury systems). Custody providers increasingly compete on the quality, stability, and composability of their APIs and dev tools.

Citi entering this space may also enable clients to manage custody and transaction flows seamlessly within a broader banking and treasury context—a potential competitive edge.

5. Tokenization, Real-World Assets (RWAs), and Embedded Financial Services

Beyond pure “crypto,” many institutions and banks are looking toward tokenization of real-world assets—such as tokenized securities, debt instruments, real estate, or commodities—as the next frontier. Custody infrastructure that supports tokenized asset standards (e.g., ERC-20, ERC-404, asset-backed tokens), cross-chain interoperability, and compliance with securities regulations could unlock additional value.

Thus, a bank like Citi might deploy custody as a foundational service, but layer on tokenization issuance, marketplace integration, and perhaps secondary trading. This positions custody not just as a cost function, but as a strategic platform.

6. Risk, Insurance & Operational Resilience

Operating as a custodian introduces exposure to hacking, theft, operational errors, protocol bugs, and counterparty risk. Advanced custodians maintain multi-layered risk controls, intrusion detection, key ceremony security, redundancy, and insurance coverage (both internal and third-party).

Citi will likely aim for high levels of insurance backing and rigorous internal controls to match institutional standards.

What This Means for Crypto Investors, Builders, and Seekers of New Opportunities

Given these developments, what should people like you—investors hunting crypto opportunities or technologists building blockchain solutions—pay attention to?

- Look for custody APIs & modular infrastructure: As banks like Citi enter, they’ll need to compete on ease of integration. This could open up white-label custody modules, plug-and-play custody services, or custody-as-a-service offerings you can build on top of.

- Layered services on custody platforms: Tokenization, yield-bearing instruments, programmable assets—these are value-adds that can differentiate a custody platform. Builders might build on custody platforms as application layers.

- Interoperability & cross-chain capability: A custodian that can safely manage cross-chain assets and support bridging will be more compelling in a multi-chain world.

- Legal & regulatory domain expertise: As custody becomes more regulated, expertise in securities, stablecoins, token standards, and compliance will be in high demand.

- Insurance, audits, and proof-of-reserve: Custody providers and protocols that standardize transparent audit schemes or open proof-of-reserve systems may gain trust and adoption.

- Emerging entrants and niche custodians: While large banks are entering, there is room for nimble, domain-specialist custodians (e.g. for DeFi-native assets, privacy coins, or specialized geographic markets).

For investors hunting new revenue sources, custody as infrastructure may offer opportunities in adjacent layers—building APIs, offering compliance, developing insurance, or innovating tokenization models that ride on custody backbones.

Conclusion

Citi’s planned launch of a crypto custody platform in 2026 marks a milestone: one of traditional finance’s giants is now placing a major bet on digital assets as part of its core infrastructure offering. This signals increasing alignment between legacy banking and blockchain-native architectures.

The timing is favorable: institutional demand for regulated custody is surging, regulatory environments are evolving in alignment, and technological maturity in custody mechanisms is advancing. Yet the challenge is steep: competing against seasoned crypto custodians, managing security risk, remaining compliant across jurisdictions, and delivering world-class integration and service.

For crypto explorers, investors, and builders, this shift offers a window. Custody platforms may become the rails on which many future decentralized finance, tokenization, and financial infrastructure applications are built. Positioning yourself in or around this infrastructure layer—API, compliance, tokenization, interoperability—may be one of the more promising paths toward discovering the next breakout crypto revenue stream.