Main Points :

- California passed AB 1052, amending its unclaimed-property law to include dormant crypto, with the requirement that assets not be forcibly liquidated but held in native form.

- A complementary law, SB 822, ensures that when assets are transferred to the state as “unclaimed,” they remain in cryptocurrency form, not sold to fiat.

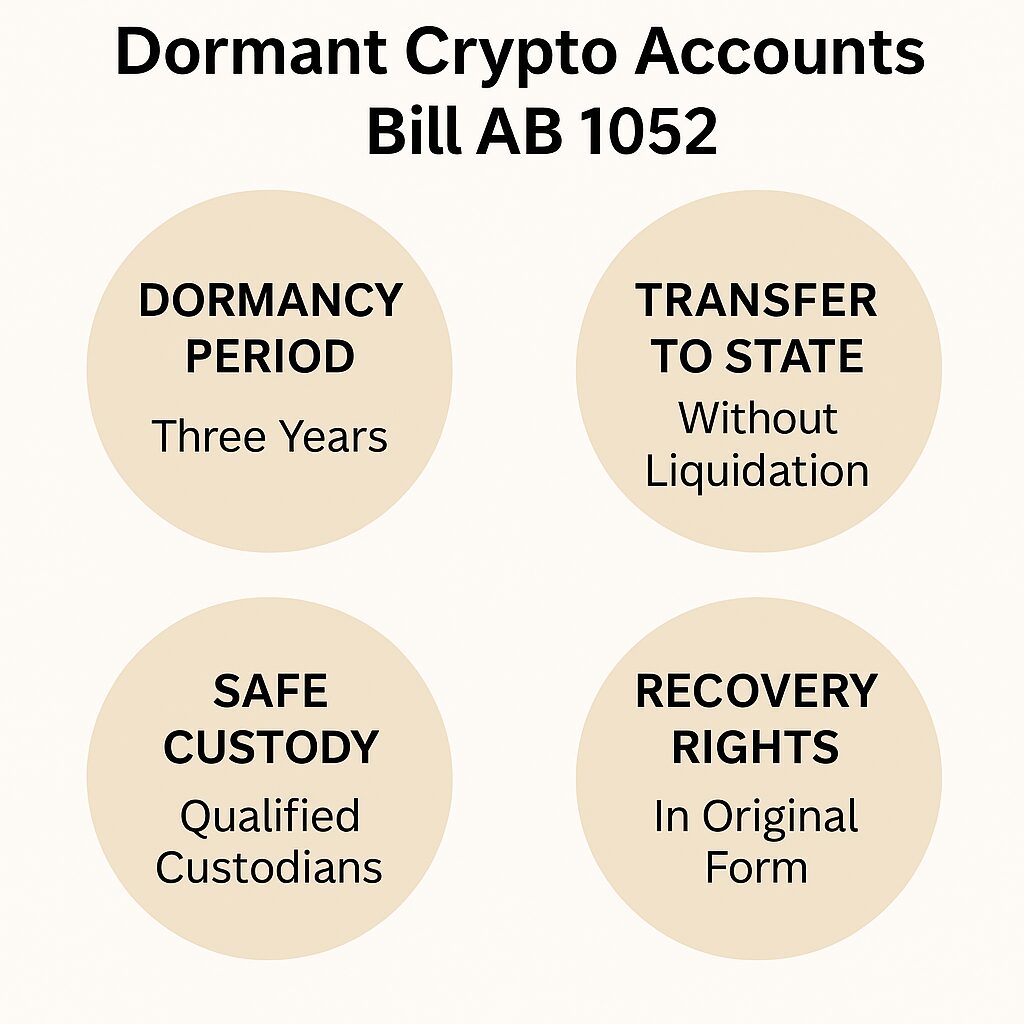

- The new laws define “acts of ownership interest” and set a three-year dormancy threshold; custodians must monitor and report.

- If no owner appears within 18–20 months after reporting, the state may liquidate into fiat under conditions.

- The moves are controversial: proponents argue they preserve upside for owners; critics warn of undermining “self-custody” and potential privacy or regulatory overreach.

- The law dovetails with broader U.S. and global trends: U.S. federal crypto policy is evolving (e.g. GENIUS Act, SAB 121 revocation), and jurisdictions (e.g. UK) push tokenization and integration of digital assets into regulatory regimes.

1. Background: Unclaimed Property Laws and Crypto Dormancy

In many U.S. states, unclaimed or “escheated” property is dormant financial or tangible property whose owner cannot be located or has not claimed it after a statutory period. Traditionally, this has applied to bank accounts, securities, unredeemed checks, gift cards, etc. California’s new step is to explicitly bring digital financial assets into that framework.

As of 2025, through AB 1052, California modifies its unclaimed property regime so that crypto assets held by custodial platforms (e.g. exchanges or other custodians) that have not shown “activity” for three years may be reported as “unclaimed.”

Before this, many dormant crypto holdings on exchanges could be forcibly liquidated by the platform (with only the cash turned over to the state) when declared unclaimed. This meant that if the asset later appreciated, the original owner lost upside gains. AB 1052 changes that dynamic.

The law also includes broader digital asset regulation: after July 1, 2026, any entity engaged in “digital financial asset business activity” in California must be licensed (unless exempt).

Thus, AB 1052 is not just about dormant crypto — it is part of a broader campaign to modernize state-level digital asset law.

2. Key Provisions of AB 1052 and SB 822

2.1 Dormancy threshold and “acts of ownership interest”

Under AB 1052 (as amended), a digital asset account is considered to “escheat” (i.e. become unclaimed property) if for three years the owner has not engaged in “specified acts of ownership interest.”

These acts include logging in, making a transfer, deposit or withdrawal, or other demonstrable engagement with the account.

If an electronic or written communication to the owner is returned undelivered OR no ownership act occurs for three years, the asset may escheat to the state.

2.2 Custodian obligations and reporting

The law mandates that custodians (exchanges, wallet providers, etc.) must monitor inactive accounts, attempt communication, and report holdings to the California controller’s office.

Upon escheat, the custodian must transfer the digital asset (in its native form) to a custodian appointed by the state controller, not convert it to fiat first.

2.3 SB 822: preserving crypto form

To reinforce AB 1052, California also passed Senate Bill 822. This bill clarifies that when dormant crypto is remitted to the state, it must remain in crypto form, not be converted to cash.

Effectively, SB 822 ensures that Bitcoin remains Bitcoin, Ethereum remains Ethereum, even while held as unclaimed property by the state.

2.4 Liquidation if owner remains missing

While the default is to preserve crypto, there is a caveat: if within 18 to 20 months (after reporting) the owner does not claim, then the state is permitted to liquidate (sell for fiat) under certain conditions.

Thus, assets do not remain indefinitely in limbo; there is a finite period after which conversion becomes allowed, presumably to reduce administrative burden or risk.

2.5 Limitations and scope

- The law applies only to custodial platforms / centralized exchanges, not to true self-custody wallets held off-exchange.

- It does not immediately cause confiscation, but rather states may “take custody” of unclaimed assets under the process.

- The law recognizes the digital assets as intangible property under California’s unclaimed property statutes.

3. Reactions, Risks, and Strategic Implications

3.1 Support and investor protection angle

Proponents argue that AB 1052 + SB 822 help protect owners from losing upside in long-dormant holdings. Under prior regimes, exchanges might liquidate dormant assets (especially during low valuation periods) and remit only cash, thereby forfeiting gains to the state or to implicit costs.

Coinbase’s Chief Legal Officer, Paul Grewal, publicly thanked Governor Newsom for signing SB 822, and called for California to extend legal backing to staking rights in line with SEC guidance.

Thus, the law is being positioned as a consumer protection measure in the crypto ecosystem.

3.2 Criticism: self-custody, privacy, and regulatory overreach

However, critics warn that requiring “acts of ownership interest” effectively pressures users to stay active on platforms or risk state custody—even if they intended to “set and forget” long-term holdings. Some see this as undermining the ethos of “not your keys, not your coins.”

There are also privacy and surveillance concerns: the state or custodians must monitor user activity or inactivity, which may conflict with privacy principles or attract regulatory overreach fears.

Another risk: ambiguity in defining what qualifies as an “act of ownership interest.” Could login activity, small balance checks, or API queries satisfy the requirement? The law leaves some room for interpretation, which may lead to disputes.

Finally, some worry about a slippery slope: once states are empowered to take custody of dormant digital assets, they may be tempted to expand that power or impose further constraints on digital property rights.

3.3 Strategic responses by users and platforms

- User self-custody becomes even more compelling. If tokens are held in one’s own private wallet (not on a third-party exchange), they would likely fall outside the regime.

- Platforms may change their dormancy policies, proactively notify customers, or require periodic reactivation.

- Estate planning and on-chain activity may become more important: users might plan to “touch” holdings periodically to avoid dormancy.

- Exchanges and custodians in California will need to build compliance systems: inactivity monitoring, reporting pipelines, and secure transfer protocols for dormant assets.

- The new regulatory burdens might encourage platforms to avoid operating in California or to limit services to nonresidents.

4. Broader Context: U.S. and Global Regulatory Trends

California’s law is a pioneering move at the state level, but must be viewed in the context of evolving federal and international regulatory shifts.

4.1 U.S. federal crypto policy moves

In 2025, the U.S. SEC revoked its 2022 accounting guidance (SAB 121), under which custodians had to treat crypto held on behalf of others as liabilities—a change welcomed by many in the industry.

Also relevant is the GENIUS Act, passed in mid-2025, which sets rules for stablecoins—including backing, reserves, auditing, and dual federal/state oversight.

Earlier in 2024, the FIT21 Act (Financial Innovation and Technology for the 21st Century Act) passed the U.S. House, intending to allocate regulatory authority between the SEC and CFTC for digital assets.

However, as of late 2025, comprehensive federal rules remain in flux. Some Senate bills are stalled in partisan contention.

Taken together, California’s approach may serve as a testbed or model for how states can handle digital assets in tandem with evolving federal law.

4.2 International moves and comparisons

- The European Union has fully implemented MiCA (Markets in Crypto-Assets), which provides a unified regulatory structure for crypto in EU member states.

- In the UK, the Financial Conduct Authority (FCA) is proposing the tokenization of investment funds (i.e. representing fund shares as blockchain tokens) to appeal to younger investors.

- In Kenya, parliament passed a Virtual Asset Service Providers Bill to regulate cryptocurrencies, designate authorities, and attract investment.

These global trends show that legislatures and regulators are actively adjusting to integrate digital assets into legal regimes, not leaving them in a Wild West state.

5. What to Watch and Implications for New Crypto Projects

For innovators, investors, and blockchain practitioners, California’s law and the broader regulatory landscape suggest several strategic considerations:

5.1 Dormancy mechanisms as a design factor

If you design a new token or platform, consider how “dormancy” might be defined, and whether tokens might ever fall under unclaimed property regimes. Build in periodic utility (e.g. staking, governance action) or “heartbeat” transactions to avoid inactivity.

5.2 Custody models and compliance

Projects that act as custodians or wallets must anticipate compliance burdens—reporting, tracking, dormant-asset transfer capabilities, and working with regulators or state custodians.

5.3 Jurisdiction planning

If a platform wants to avoid or limit exposure to these rules, jurisdictions matter. A California-only rule may not apply elsewhere, but precedent is powerful. Consider where your platform is domiciled, where users are based, and whether you accept operations in states with similar laws.

5.4 Legal clarity and ambiguity

Many ambiguities remain (e.g. “act of ownership,” timing, obligations). Legal challenges or judicial interpretation will matter. Monitoring emerging case law or administrative guidelines is crucial.

5.5 Opportunity in tokenization and compliance infrastructure

Because jurisdictions are institutionalizing digital asset regulation, there’s a growing need for compliance middleware, auditing, custody systems, and legal abstraction layers. Projects that help exchanges or custodians implement these state regimes may find market demand.

Summary & Outlook

The enactment of California’s AB 1052 (and companion SB 822) marks a momentous step: it is the first U.S. state to legislate that dormant crypto assets on custodial platforms may be claimed by the state but kept in crypto form rather than forcibly liquidated. The law balances investor protection (by preserving upside) and state authority (by enabling custody and eventual liquidation if unclaimed for long).

Critics warn of privacy risks, erosion of self-custody ethos, and uncertain interpretations. For innovators and investors, the law adds a new dimension to strategy: how to “touch” assets, how to design inactivity-resilient protocols, how to choose jurisdictions, and how to build compliance tools.

In the broader picture, this law is part of a wave: U.S. federal frameworks (e.g. GENIUS Act, FIT21) are evolving, and globally, regulatory regimes are integrating crypto (e.g. MiCA in EU, tokenization proposals in UK, regulation in Kenya).

As the field matures, we may see more states emulate California’s approach, or federal law impose a unified scheme. For anyone searching for the “next crypto” or evaluating revenue models, understanding the interaction between dormancy, custody, and regulation is essential.

If you like, I can also craft a visual infographic summarizing the workflow of dormant crypto under AB 1052, or send you a ready-to-publish version with graphs. Would you like me to prepare that?