Main Takeaways :

- Kenya’s Parliament has passed the Virtual Asset Service Providers Bill 2025, placing all crypto-service providers under a licensure regime.

- The Central Bank of Kenya (CBK) will license stablecoin/issuance, while the Capital Markets Authority (CMA) will oversee exchanges and trading platforms.

- The law mandates strong operational, custody, audit, and AML/KYC requirements for VASPs.

- This move aims both to protect consumers and to attract institutional and global crypto players.

- Kenya seeks to position itself as a fintech / crypto hub in East Africa, joining peers like South Africa and Nigeria.

- The real test will be in the implementation of the rules, enforcement, and balancing innovation with regulation.

- In the wider African context, projects like COMESA’s digital payments platform and grassroots crypto adoption in informal communities show how regulation, payments infrastructure, and inclusion are intertwining.

Below is a deeper dive by section, followed by a summary and outlook.

1. Background: Why Kenya Now Moves to Regulate Crypto

Kenya has long been viewed as a frontier for fintech innovation in Africa, especially given its historic leadership in mobile money (e.g. M-Pesa). That infrastructure and financial inclusion mindset have created fertile ground for digital asset use, especially among youths and informal sectors. The absence of a clear legal framework, however, has left the crypto sector in regulatory limbo, vulnerable to fraud, lack of oversight, and potentially stumbling into conflicts with existing financial law.

By passing the Virtual Asset Service Providers Bill 2025, the Kenyan Parliament has attempted to close that gap. The bill, having cleared legislative hurdles, has now been sent to President William Ruto for assent (i.e. signature) before it becomes law.

The timing is notable: it coincides with global and regional shifts toward clearer digital-asset regulation, growing interest from institutional players, and pressure from bodies like the Financial Action Task Force (FATF) for countries to adopt robust anti-money-laundering (AML) and countering financing of terrorism (CFT) frameworks.

In short, Kenya is attempting a transition from “crypto tolerated but murky” to “crypto governed and encouraged.”

2. What the VASP Bill Requires: Structure & Obligations

2.1 Definition and Scope of VASPs

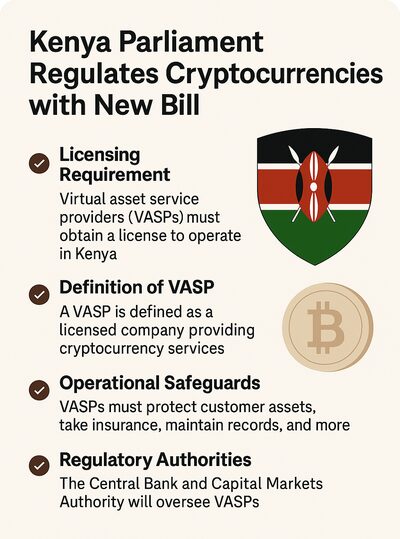

The bill defines a Virtual Asset Service Provider (VASP) as an entity offering virtual asset services within Kenya or registered under Kenyan law (including foreign firms registering locally). The definition is broad: it covers exchanges, wallet providers, custody, token issuers, brokers, and related infrastructure.

2.2 Dual Regulator Model

A central design of the bill is a dual regulatory oversight:

- Central Bank of Kenya (CBK): Responsible for licensing and supervising the issuance of stablecoins and virtual asset issuers, as well as oversight of custody and reserves.

- Capital Markets Authority (CMA): In charge of licensing and regulating exchanges, trading platforms, brokers, and marketplaces handling virtual assets.

This model mirrors some regimes in advanced markets (e.g., distinguishing issuance oversight from trading oversight) and attempts to leverage existing regulators rather than creating a wholly new institution.

2.3 Licensing Requirements and Compliance

VASPs under this law must meet stringent criteria:

- Maintain strong custody and segregation of clients’ assets, possibly in separate accounts or cold storage.

- Hold minimum capital / solvency buffers (exact thresholds to be defined via subordinate regulations).

- Implement audit, transparency, and recordkeeping protocols, keeping detailed transaction logs.

- Adhere to KYC / AML / CFT rules, including customer identification, monitoring, suspicious activity reporting, and record retention.

- Maintain conflict-of-interest policies, insurance or protection for user funds, and local bank accounts.

- Obtain licenses and renewals; noncompliance can lead to fines, license revocation, or criminal liability.

The bill also contemplates a permission regime for foreign stablecoins: only those from vetted jurisdictions or approved prior issuers may enter the Kenyan market, subject to reserve audits and regulatory guarantees.

Additionally, the Treasury will have authority to issue rules and regulations (subordinate legislation) defining details such as capital thresholds, custody rules, disclosure and reporting formats.

2.4 Consumer Protections & Market Integrity

The bill explicitly aims to protect users and ensure integrity:

- Firms must guard against fraud, manipulation, and misuse of assets.

- Licensing ensures only vetted institutions operate in Kenya, reducing the risk of rogue, fly-by-night operators.

- The law aims to bring Kenya in alignment with international standards (e.g. FATF).

- Enforcement mechanisms are envisioned to deter noncompliance, including civil and possibly criminal consequences.

Thus, the law does not merely permit crypto; it imposes a high bar for trust and accountability.

3. Strategic Aims: Why Kenya Is Doing This

3.1 Legitimacy and Risk Mitigation

By codifying rules, Kenya seeks to reduce regulatory uncertainty, which has deterred serious participants. Clear law reduces the risk of legal surprises, government crackdowns, or retroactive penalties. For investors and businesses, predictability is critical.

Moreover, the law is a guardrail against fraud, scams, market turbulence, and misuse of anonymity in crypto systems — all concerns that arise in lightly regulated environments.

3.2 Attracting Institutional Capital & Global Players

Kenya hopes this legal clarity will draw in established crypto firms (e.g. Binance, Coinbase) and institutional capital. As noted by Finance Committee Chairman Kuria Kimani, Kenya aspires to be a gateway for crypto business into Africa.

A fully licensed, regulated regime may make Kenyan operations eligible for global partnerships, investment, treasury operations, and listings that would otherwise find regulatory risk too high.

3.3 Regional Leadership & Fintech Hub Ambition

With this law, Kenya is seeking to assert leadership in East Africa and Africa at large. It seeks to join compatriots like South Africa (which already has crypto regulation) and Nigeria, to become a regional fintech and blockchain anchor.

This can help Kenya attract talent, tech startups, and cross-border liquidity. Operating as a regulated hub could enable Nairobi to host more tokenization, DeFi, payments, and blockchain projects targeted at the wider African market.

3.4 Promoting Financial Inclusion & Innovation

Digital assets are increasingly used not only for trading or speculation, but for payments, remittances, microloans, decentralized finance (DeFi), tokenization of assets, and as a mechanism for those underserved by traditional banking.

In Kenya itself, grassroots experiments are already ongoing. For instance, in Nairobi’s Kibera slum, an initiative called AfriBit Africa enables local people (such as waste collectors) to use bitcoin for payments, aiming to bring financial services to the unbanked.

Thus, the regulatory framework can legitimize and scale those experiments, under protection, oversight, and integration with broader financial infrastructure.

4. Trends & Context: What This Signals for Africa and Crypto

4.1 African Regulatory Shifts Toward Crypto

Kenya is not alone in this regulatory turn. Across Africa:

- South Africa already has rules and guidance for crypto assets and intermediation.

- Nigeria has had a mixed approach but is increasingly pushing regulation over blanket bans.

- Botswana, Mauritius, Ghana, and other nations have also introduced frameworks or policy stances on digital assets.

- The Common Market for Eastern and Southern Africa (COMESA), which includes Kenya, has launched a Digital Retail Payments Platform to facilitate cross-border trade in local currencies, reducing dependency on the U.S. dollar.

These movements indicate that various African nations see crypto and blockchain not as fringe experiments but as infrastructure to boost cross-border trade, remittances, and financial inclusion.

4.2 Payment Infrastructure + Crypto = Synergies

Regulation alone is not sufficient: digital payments rails and infrastructure must evolve to absorb crypto flows. The COMESA initiative is an example: enabling local currency settlement across borders lowers friction and makes token-based or crypto-adjacent payment solutions more feasible.

Moreover, tying crypto services to fiat rails (banking, settlement, reserve backing) is key to real adoption. Kenya’s law, by requiring licensed VASPs to hold Kenyan bank accounts and custody reserves, is acknowledging that interface.

4.3 Risks, Challenges, and Innovation Tension

While regulation is welcome to many, it also introduces friction and costs:

- Compliance burdens (KYC/AML, audits, capital requirements) may deter smaller or experimental projects.

- Overly rigid rules risk killing innovation — especially in DeFi, tokenization, or borderless constructs.

- Enforcement will be key: regulators must have capacity, technical understanding, and consistency, or else the law becomes symbolic.

- There’s a risk of “regulatory arbitrage,” where firms shift to more permissive jurisdictions.

Balancing that tension—innovation vs. control—will be a continuous challenge.

4.4 Local Usage, Remittances & DeFi Potential

Crypto in emerging markets often gains traction through remittances, cross-border payments, and DeFi yield opportunities that outperform traditional local banking yields. Kenya’s young population, significant remittance inflow, and fintech-friendly culture make it fertile ground.

If licensed VASPs can integrate low-friction stablecoins or tokenized assets, Kenya could see new use cases: tokenized agriculture, microfinance using smart contracts, supply-chain tokens, and more.

5. The Path Forward & Key Milestones

5.1 Presidential Assent & Enactment

The bill still requires signature from President Ruto to become law. That is expected to be a formality, though it could be delayed depending on political considerations.

5.2 Subordinate Regulations & Rulemaking

Once signed, the Treasury and regulators will need to issue detailed rules: capital thresholds, custody frameworks, audit schedules, interface standards, reporting templates, etc. This is where much of the detail is determined, and where industry input will matter.

5.3 Licensing, Onboarding, and Market Transition

Existing crypto companies in Kenya or targeting Kenya must register, adjust to compliance, and seek licensing. Some may drop out; others will scale up. International players may apply to open Kenyan operations.

5.4 Monitoring & Enforcement

To maintain credibility, regulators will need to enforce rules, penalize abuses, audit compliance, and ensure that licensees truly operate to the high standard set by law.

5.5 Measuring Impact

Key metrics to watch:

- Number of licensed VASPs, and types (exchanges, custodians, issuers)

- Capital inflows and foreign institutional participation

- Growth in trading volume, liquidity, and usage of blockchain-based applications

- Integration with financial sector: partnerships with banks, fintechs

- Consumer protection outcomes: fewer scams, market stability, dispute resolution

- Economic spillovers: jobs, startup growth, crypto tourism

6. Implications for Crypto Hunters, Entrepreneurs & Practitioners

6.1 Opportunity: Entry into a Newly Regulated Market

If you are searching for the “next crypto frontier,” Kenya may offer opportunity. Projects or platforms that comply with the regime early may gain first-mover advantages. Licensed infrastructure (wallets, custody, token issuance) may see demand.

6.2 Challenge: Complying Without Losing Innovation

Innovators must build with regulation in mind: modular designs, auditability, robust security, compliance overhead. The cost of regulation can be high, so business models must account for that.

6.3 Partnership with Financial Institutions

Bridging between crypto and fiat will matter. Projects that can integrate with local banks, connect to Kenyan banking rails, or support tokenization of real-world assets in Kenya may find premium opportunities.

6.4 Regional Scaling

Kenya may serve as a hub, but projects can expand regionally (East Africa, COMESA region). If the Kenyan regulatory model is respected by neighbors, platforms can scale across borders.

6.5 Risk Assessment: Geopolitics, Enforcement, Currency Volatility

Regulated or not, operating in emerging markets carries risk: policy shifts, political changes, enforcement unpredictability, local currency volatility. Prospective participants must assess these rigorously.

7. Summary & Outlook

Kenya’s passage of the Virtual Asset Service Providers Bill 2025 is a landmark moment: it transforms digital assets in Kenya from a legal gray zone into a regulated domain. The law aims to safeguard consumers, foster innovation, and position Kenya as a crypto-forward hub in Africa. Its success, however, depends on execution: how detailed rules are written, how enforcement is managed, and how the private sector adapts.

For crypto enthusiasts, investors, entrepreneurs, and blockchain practitioners, Kenya now represents a market to watch closely. Early movers who align with regulation may capture advantage. Those indifferent to jurisdictional risk may be more hesitant. But broadly, Kenya’s move reflects a maturing of the global crypto ecosystem where emerging markets are no longer on the sidelines — they are shaping regulatory frontiers.