Main Points :

- JPMorgan is planning to launch cryptocurrency trading services for clients, but not in-house custody in the near term.

- The bank is pursuing an “and” strategy: working both within existing traditional finance and exploring new digital asset opportunities.

- JPMorgan has piloted a deposit token called JPMD on Base (an Ethereum Layer-2) as a bridge between traditional banking and blockchain rails.

- The bank sees a multi-chain future rather than a single dominant blockchain (i.e. not Ethereum alone).

- Regulatory clarity, risk appetite, and institutional demand will drive JPMorgan’s next moves.

- For readers seeking new crypto opportunities or real-world blockchain applications, JPM’s moves suggest where institutional capital and infrastructure might flow next.

Introduction

JPMorgan Chase, one of the largest and most influential financial institutions globally, is finally making a more assertive move into the digital asset space. While the bank has long been cautious — even critical — of cryptocurrencies, recent remarks by its leadership indicate it is ready to offer crypto trading services to clients, though direct custody (holding the assets itself) is off the table for now. This pivot is meaningful: it signals that traditional finance is increasingly comfortable integrating with blockchain and digital asset infrastructure, albeit in a risk-measured fashion.

In this article, I will (1) summarize the details of JPMorgan’s announced strategy, (2) contrast that strategy with recent developments in broader banking adoption of crypto infrastructure, (3) analyze implications for where institutional flows might go, and (4) conclude with what this means for innovators, developers, and aspiring adopters in the crypto/blockchain space.

Below is both an English version and a Japanese translation (non-summarized) of the article.

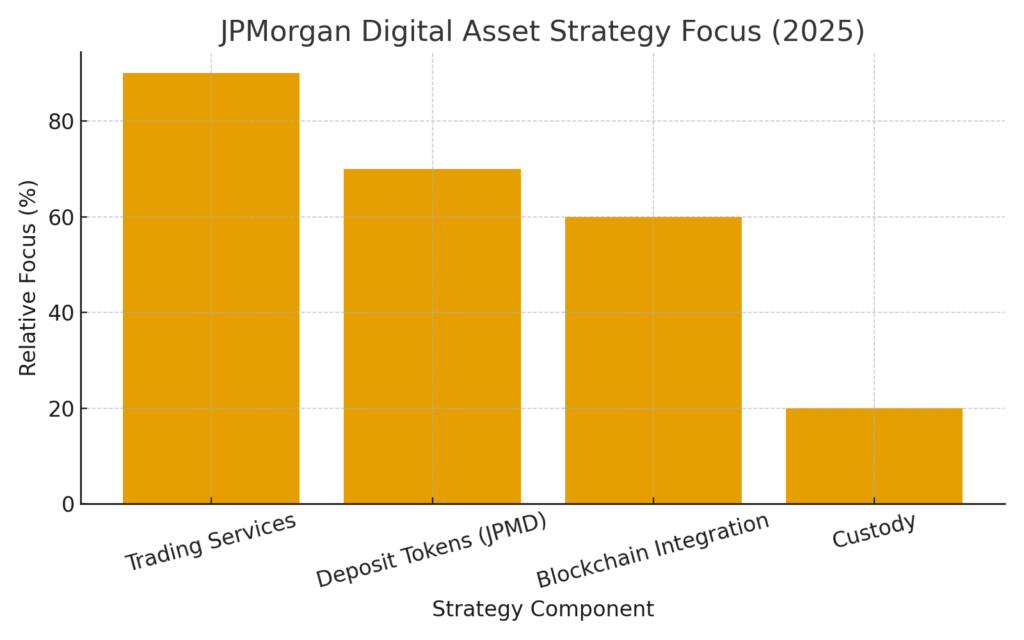

1. JPMorgan’s New Crypto Strategy: Trade, Not Custody (For Now)

Over recent days, Scott Lucas — Global Head of Markets and Digital Assets at JPMorgan — confirmed in media interviews that the bank is actively developing plans to provide cryptocurrency trading services to its clients. However, the firm is not planning to act as a custodian (i.e. directly hold private keys or wallets for clients) in the near future. When asked specifically whether JPMorgan would emulate Citibank or others by offering custody, Lucas stated it is “not on the horizon near-term.”

Lucas made clear that the firm is still evaluating which third-party custodians might be integrated, as well as how far JPMorgan is willing to push its institutional risk tolerance. He emphasized that custody would likely follow after the trading business is baked in, but only when the internal and regulatory risk frameworks are in place.

This phased approach allows JPMorgan to test the waters in digital assets while avoiding some of the steep capital, regulatory, and operational burdens associated with full custody.

2. The “And” Strategy: Traditional + Emerging, Simultaneously

Lucas also described JPMorgan’s approach as an “and” strategy — i.e. not choosing between the legacy financial world and blockchain/digital assets, but navigating both concurrently. In practice, this means JPMorgan will continue to service conventional markets while selectively building new infrastructure and products in the digital domain.

This theme is consistent with JPMorgan’s broader posture in recent years: maintain leadership in traditional banking and markets, yet avoid being left behind in the evolution toward tokenization, programmable assets, and blockchain-native flows.

3. JPMD: JPMorgan’s Deposit Token Experiment

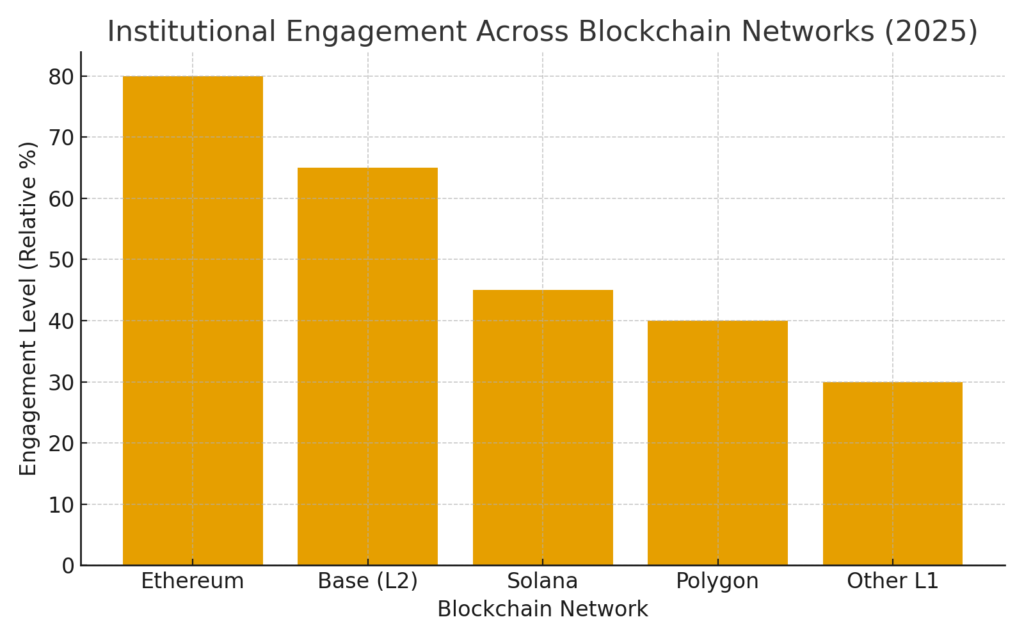

One of the most striking developments is JPMorgan’s pilot of a USD deposit token known as JPMD. This deposit token is being tested as a Proof-of-Concept (PoC) on Base, an Ethereum Layer-2 network developed by Coinbase.

JPMD is distinct from stablecoins: it is intended to represent a bank deposit (i.e. a digital claim on JPMorgan’s balance sheet) and is issued by a permissioned infrastructure initially, albeit transacting on a public chain. JPMorgan labels it a “deposit token,” not a stablecoin, emphasizing that it is integrated with traditional deposit and liquidity frameworks.

The stated rationale is that institutional clients may want on-chain, 24/7 settlement, compatibility with tokenized assets or collateral, and seamless cash settlement in digital flows. JPMD is seen as bridging JPMorgan’s existing cash/treasury infrastructure with blockchain rails.

Though still experimental, JPMD’s deployment is a signal: JPMorgan is laying tonal groundwork for tokenized deposits and cash-equivalent instruments that can inhabit the blockchain world.

4. Not Betting On Ethereum Dominance: A Multi-Chain Outlook

Lucas also expressed skepticism that Ethereum will emerge as the ultimate, singular blockchain for all activity. He argued that the landscape will remain multi-chain, with emergent Layer-1 networks and alternative ecosystems gaining traction alongside Ethereum.He suggested JPMorgan will monitor and possibly participate across multiple public chains.

This is an important signal: rather than backing one network, JPMorgan is giving itself flexibility to deploy services where competitive advantages or use cases arise.

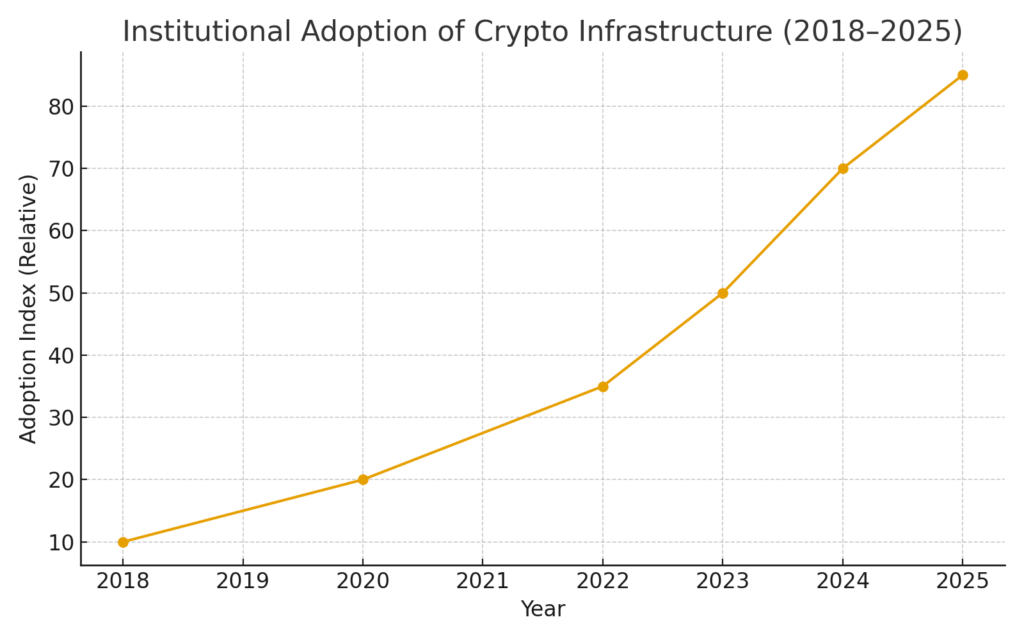

5. Recent Trends & Competitive Context in Institutional Crypto

JPMorgan’s shift should be seen in the broader context of institutional adoption, evolving regulation, and competitive pressure:

- Banks exploring custody: While JPMorgan is holding off on custody for now, other large players are making moves. For example, Citibank reportedly plans to launch a crypto custody service in 2026.

- Tokenized deposits and stablecoin interest: Banks including Citi and JPMorgan are publicly stating interest in tokenized deposits and stablecoin platforms.

- Regulatory clarity and risk tolerance: Lucas noted that regulatory frameworks are gradually becoming clearer, enabling more confident exploration by traditional institutions.

- Custody revival among banks: U.S. Bancorp is relaunching its institutional Bitcoin custody service.

- Shifting leadership tone: JPMorgan CEO Jamie Dimon, once vocally critical of crypto, has recently signaled growing openness to stablecoins and tokenized deposits.

- Regulatory momentum in U.S. legislation: Passage or movement of bills like the GENIUS Act could further legitimize stablecoins and tokenized deposits in regulated banking contexts.

All these signals suggest that JPMorgan is positioning itself for gradual, but meaningful, integration into the digital asset ecosystem without overcommitting prematurely.

6. Implications for Crypto Innovators, Developers, and Seekers of New Assets

For readers who are scanning for emerging cryptos, new yield avenues, or practical blockchain adoption, JPMorgan’s moves carry several possible implications:

- Demand for supporting infrastructure: As big banks begin engaging, they will need secure, high-performance infrastructure — custody providers, auditing, compliance tools, token bridges, governance frameworks, etc. Building these “plumbing” services may yield significant opportunities.

- Tokenized money instruments: JPMD and similar deposit tokens may give rise to novel use cases — e.g. on-chain cash layering, programmable treasury, tokenized lending using deposit tokens as collateral, or embedded finance models.

- Institutional flows may favor regulated tokens: Banks will likely prefer working with tokens or instruments that conform to compliance requirements (KYC/AML, transparency, auditability). Projects that can align with institutional-grade standards may attract partnerships or capital.

- Multi-chain opportunity space: Since JPMorgan is not pegged to a single chain, ecosystems on non-Ethereum Layer-1 or Layer-2 may attract institutional attention, especially those that deliver performance, interoperability, or unique features.

- Gradual adoption rather than overnight disruption: JPMorgan’s risk-measured pace warns that institutional adoption won’t be explosive or brusque — expect incremental rollouts, pilot programs, and partnerships before full-scale launches.

7. Conclusion: A Gradual Bridge Between TradFi and Web3

JPMorgan’s announced pivot toward providing crypto trading services, combined with experimentation in deposit tokens (JPMD) and a flexible multi-chain orientation, marks a critical inflection in how major financial institutions will integrate with blockchain systems.

Although the bank refrains from custody today — citing risk, regulatory, and operational concerns — its “and” approach reveals a strategy of evolving rather than replacing. For those scanning for the next crypto opportunities, JPMorgan’s direction offers clues: compliance-aligned infrastructure matters, tokenized cash instruments may become significant, and interoperability across chains will be essential.

In short, JPMorgan is not leaping headlong into crypto, but stepping cautiously along a path that bridges traditional money and programmable digital finance. For those building on the frontier, the question is: will you build the rails on which institutions will one day run?