Main Points :

- France’s central bank advocates granting ESMA direct supervisory authority over major crypto-asset issuers under MiCA

- Concerns over “multi-issuance” of stablecoins and regulatory arbitrage within the EU

- Divergent views: European Commission argues current MiCA rules suffice, while ESRB and some central banks call for tighter oversight

- Recent developments include eurozone ministers discussing how to promote euro-denominated stablecoins

- Implications for new crypto projects, stablecoin design, and cross-jurisdictional monitoring

1. Introduction: Why France Wants ESMA to Lead Crypto Oversight

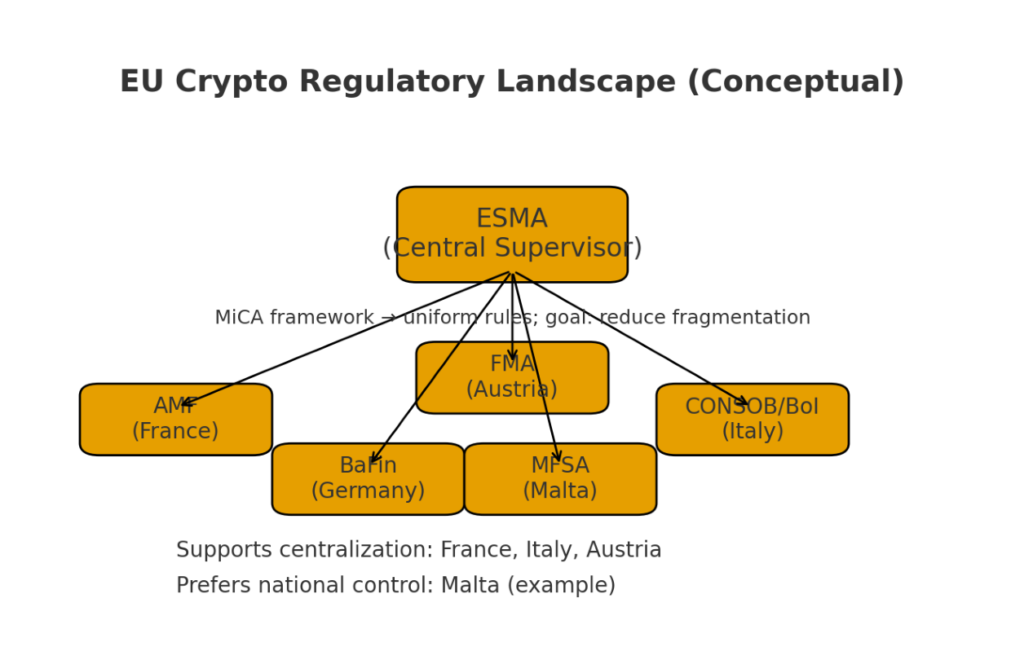

France’s central bank has recently renewed its call for the European Union to centralize crypto supervision under ESMA (European Securities and Markets Authority). The argument is that the current structure—where individual EU member states regulate crypto issuers under the MiCA (Markets in Crypto-Assets) framework—risks fragmentation and regulatory arbitrage. In particular, France sees these gaps as threatening the coherence of EU-wide enforcement, investor protection, and even the monetary sovereignty of the euro.

In this article, I summarize the arguments and counterarguments, incorporate the latest developments, and assess what this means for stakeholders seeking new crypto opportunities or designing blockchain systems that operate across borders.

Key Drivers behind the Proposal

France’s central bank governor, François Villeroy de Galhau, speaking at a fintech forum in Paris, argued that letting national regulators retain full control under MiCA risks uneven enforcement and “regulation shopping” among crypto firms.

He contends that ESMA should be empowered to directly supervise crypto-asset issuers, not just via national authorities, to ensure uniform rule application across the entire EU.

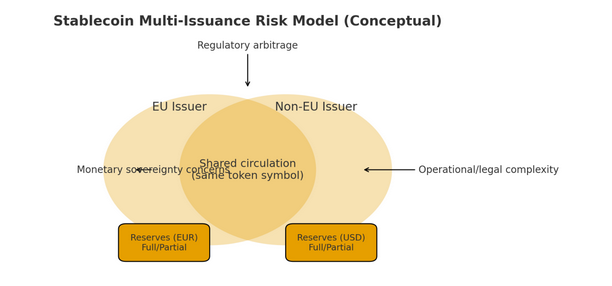

A particular point of vulnerability is the MiCA provision permitting multi-issuance of the same stablecoin—i.e. the same token being issued from both EU and non-EU entities—combined with only partial reserve backing. France sees this as a “weakness” that could erode the euro’s independence and lead to overreliance on non-European infrastructure.

Italian regulators have echoed these concerns, warning that fungible tokens across jurisdictions raise operational, legal, and stability risks.

Moreover, the ESRB (European Systemic Risk Board) has recently recommended a ban on cross-border stablecoin operations issued outside the EU as a safeguard measure.

In sum, proponents see centralized oversight as necessary to:

- eliminate enforcement gaps or “weak links” among member states

- enforce stricter controls on stablecoin issuance and reserve requirements

- protect the euro and EU financial sovereignty

- guard against systemic risks in times of market stress

Counterarguments & Tensions

However, not everyone is convinced. The European Commission has responded that existing MiCA rules already sufficiently address stablecoin risks and that further changes may be unnecessary.

Indeed, MiCA’s rules on reserve backing, transparency, and licensing for e-money tokens (EMTs) and asset-referenced tokens (ARTs) became effective in June 2024 for stablecoins, and in December 2024 for crypto service providers.

Critics of the French proposal argue that:

- Centralizing oversight might make the system more bureaucratic and less responsive to local innovation.

- It could discourage competition or burden smaller, regional crypto participants.

- Revisiting multi-issuance rules could undermine the very flexibility that allows cross-border scale and interoperability. Indeed, industry groups have warned that overrestriction might harm Europe’s competitiveness.

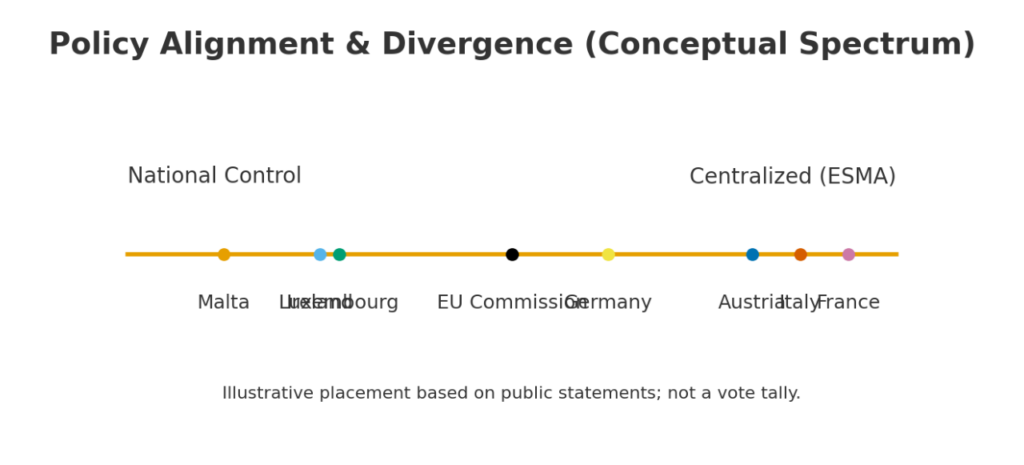

Furthermore, some member states are cautious. Malta, for instance, fears that centralization may reduce efficiency and might prefer enhanced collaboration among national supervisors rather than full authority transfer.

France has even threatened to block “passporting”—the mechanism by which a firm licensed in one EU country may operate in all others—if it continues to see weak regulatory standards in some jurisdictions.

Thus, the debate is not simply about more rules, but about who enforces them, how uniformly, and at what cost to innovation.

Recent Developments & Evolving Landscape

Recent events confirm that this is more than a theoretical debate. A few key developments:

- Eurozone ministers are now discussing ways to boost euro-denominated stablecoin issuance to counter the dominance of U.S. dollar–pegged tokens.

- The European Commission has signaled its commitment to preserve the existing MiCA framework, even amid pressure for change.

- The ESRB has intensified warnings around multi-issuance schemes, urging urgent policy action.

- France, Italy, and Austria are aligning in their calls for centralized oversight.

- The EU’s crypto supervisory authorities (EBA, EIOPA, ESMA) have also issued reminders and fact sheets to consumers, clarifying what protections MiCA affords and what risks remain.

From a crypto-project or business perspective, these changes matter. The rules governing passporting, jurisdiction, reserve backing, redemption rights, and cross-border operations all influence the architecture of new tokens and services.

What It Means for New Crypto Projects & Stablecoin Architects

For anyone designing or evaluating a new token or crypto business under EU jurisdiction or aiming at EU users, the evolving supervisory landscape presents both challenges and opportunities:

- Jurisdictional Strategy

Where you incorporate or register matters more than ever. If ESMA becomes the direct supervisor of major issuers, projects may find it optimal to choose structures that place them under ESMA’s purview, rather than fragmented national authority. - Designing Stablecoins

The debate over multi-issuance means that truly fungible tokens issued across jurisdictions may face new restrictions or additional reserve/redeemability requirements. Projects may need to adopt more conservative models:- Single-jurisdiction issuance

- Full reserve backing (no partial reserves)

- Clear, auditable redemption mechanisms

- Emergency liquidity safeguards

- Cross-Border Compliance & Monitoring

Real-time supervision, uniform disclosure, and standardized audit frameworks may become mandatory. Blockchain projects will need strong governance, transparent reserve mechanisms, and rigorous risk controls to satisfy cross-jurisdictional regulators. - Investor Confidence & Positioning

A token approved by ESMA (or seen operating under such a regime) may carry a competitive advantage in terms of credibility and stability. Investors and institutions are likely to favor tokens with robust regulatory backing, especially in more cautious markets. - Competition & Innovation Balance

The centralization push risks stifling nimble innovation if “one size fits all” standards dominate. Projects that can balance compliance with flexibility (e.g. modular or upgradeable protocols) may thrive.

Summation & Outlook

France’s call to centralize crypto supervision under ESMA is more than just regulatory posturing—it represents a strategic attempt to reclaim control of the financial infrastructure as crypto becomes more embedded in global payments and capital flows. While the European Commission presently defends the sufficiency of MiCA, mounting pressure from central banks and macroprudential authorities suggests that enhancements or clarifications are likely.

For builders, investors, and innovators in blockchain and crypto, this evolution means paying close attention to the rules of jurisdiction, stablecoin architecture, and governance models. Tokens designed to operate at scale across borders must anticipate stricter oversight, cross-jurisdiction compliance burdens, and higher standards for reserve management and transparency.

In the months ahead, key focus areas will include:

- Whether the EU will amend MiCA to limit or refine multi-issuance mechanisms

- The extent to which ESMA (or another central authority) gains direct supervisory powers

- The development of euro-denominated stablecoins and how they compete with dollar-pegged incumbents

- How new crypto projects position themselves to align with evolving regulatory certainty

Ultimately, the balance between innovation and prudential stability is being renegotiated in Europe—and that will shape where the next wave of crypto opportunity emerges.