Key Takeaways :

- The USDe depeg event on Binance appears to stem from an internal oracle referencing Binance’s illiquid orderbook, not a failure of USDe’s collateral or protocol.

- Some traders allege a coordinated attack exploited Binance’s “Unified Account” collateral system, amplifying liquidations and triggering cascade effects.

- The depeg was largely isolated to Binance; across other venues, USDe remained close to $1 and redeeming functions operated normally.

- Binance has committed to compensating affected users (~$283 million) and changing oracles and risk parameters.

- The episode highlights deeper risks in exchange-specific oracle design, collateral architecture, and systemic contagion in leveraged markets.

Background: What Happened to USDe on Binance?

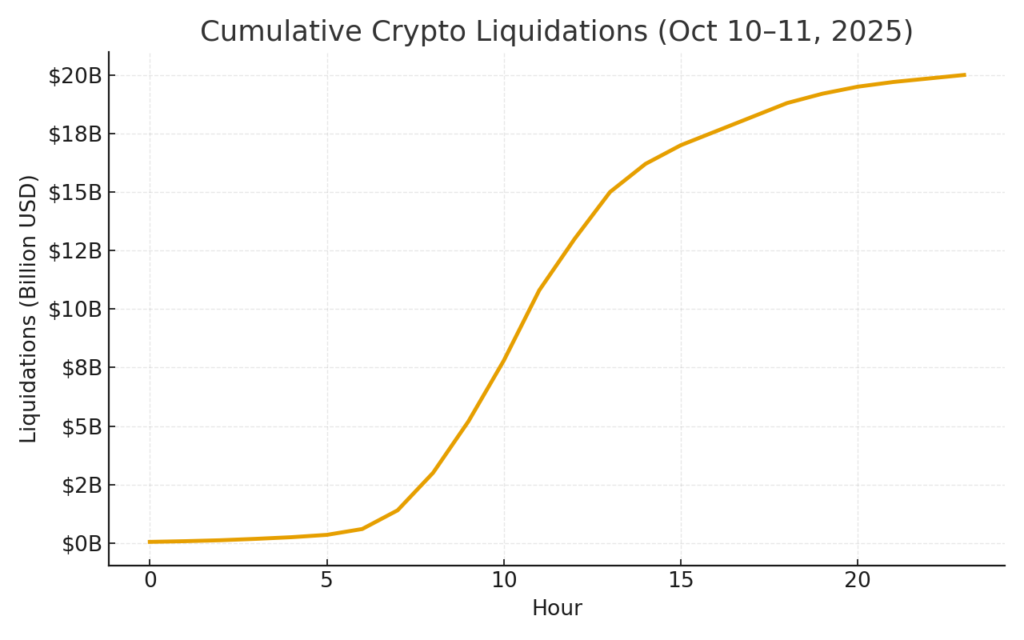

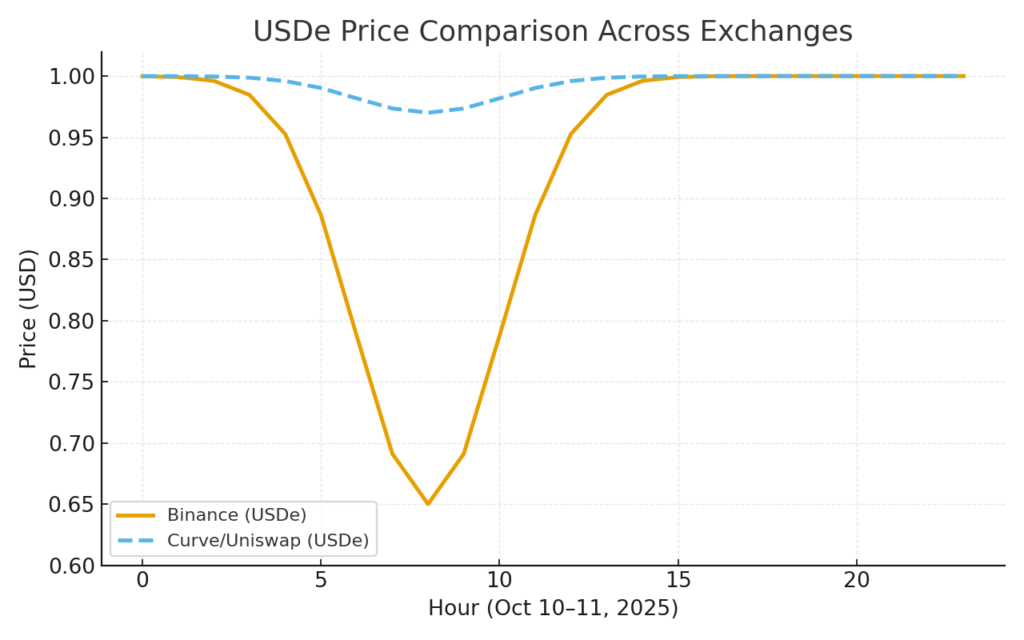

On October 10–11, 2025, a dramatic upheaval struck the crypto markets: Ethena’s yield-bearing synthetic dollar, USDe, lost its peg on Binance, falling to as low as $0.65. This event coincided with one of the largest 24-hour liquidation cascades in crypto history, with over $19B–$20B of leveraged positions liquidated globally.

According to Guy Young, co-founder of Ethena Labs, the incident was not caused by any deficiency in the USDe protocol, its underlying collateral, or the token’s structure. He claims that minting and redemption continued operating smoothly through the volatility, and about $2 billion worth of USDe was redeemed across Curve, Fluid, Uniswap, and other venues within 24 hours, with deviations limited to ~30 basis points (bps) or less.

The sharp price distortion was, he argues, isolated to Binance, because Binance’s oracle for USDe referenced its own internal orderbook data (which had limited liquidity and was under stress during the crash), rather than tapping into deep external pools of liquidity. This design made it vulnerable to price shocks: the orderbook-based oracle gave a skewed value, which then cascaded into forced liquidations among traders using USDe as collateral on that platform.

Young argues that had Binance adopted a global liquidity-depth oracle (aggregating across pools), “no one would have been liquidated” in money markets referencing USDe globally.

On Binance’s side, the exchange recognized the disruption and pledged compensation of $283 million to affected users (covering futures, margin, loan, collateral redemptions) and plans to implement changes including adding redemption prices to index weights, a soft price floor, and transitioning to external oracle feeds.

Yet independent observers and traders raise the possibility that this was not mere misconfiguration — but a strategically timed exploit.

Coordinated Attack Theory: How Could It Be Done?

Binance’s “Unified Account” & Collateral Vulnerabilities

Some traders, notably “ElonTrades,” propose that the depeg was intentionally engineered by exploiting vulnerabilities in Binance’s Unified Account system, which allows users to deposit various assets (including USDe) as collateral for margin and leveraged trading.

In this system, the price oracle input was tied to Binance’s internal orderbook rather than external or aggregated feeds. That was, in their view, a “major vulnerability.” Elasticity in time: Binance had publicly announced that it would switch to external oracles by October 14. The attack, they suggest, unfolded in the interim—when the vulnerability was known but not yet patched.

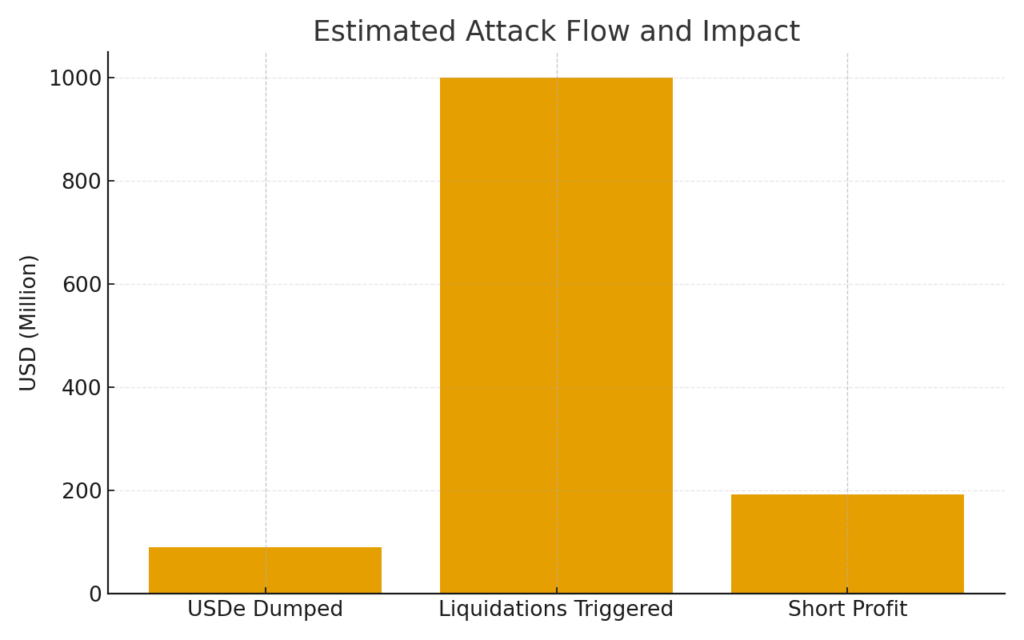

During that window, attackers reportedly dumped up to $90 million worth of USDe into Binance’s orderbook, driving the on-exchange price to $0.65. That in turn forced liquidations on Binance of other users — estimated at up to $1 billion in collateraled positions.

Simultaneously, the attackers had opened massive short positions in Bitcoin (BTC) and Ethereum (ETH) on the decentralized perpetual futures platform Hyperliquid—just minutes before a U.S. tariff announcement (by then-President Trump) triggered broader market panic. The shorts, closed after the crash, yielded some $192 million in profit in speculation.

Some even argue the overall cascade loss of $20B in liquidations may have been triggered by a relatively modest $100 million position, acting as a contagion amplifier.

Timing & Targeting: Suspicious Alignment

The timing is especially suspicious: the collapse occurred in the window between Binance’s announcement and the scheduled oracle fix (Oct 14). This suggests the attackers exploited a “sweet spot” before the upgrade.

Moreover, only a few specific tokens — USDe, BNSOL, WBETH — suffered dramatic depegging on Binance; other stablecoins like USDT, USDC were relatively stable. That selective targeting gives credence to the idea of a concentrated exploit, rather than indiscriminate market stress.

Some analysts and commentators (e.g., @KookCapitalLLC) even allege that Binance itself may have had knowledge or participation in the vulnerability vector to induce mass liquidations, perhaps to weaken competing venues like Hyperliquid. These remain speculative claims.

On-Chain Behavior, Market Reaction & Containment

On-Chain and Cross-Platform Behavior

Across other venues and DeFi money markets, USDe largely maintained its peg, with minting/redeeming operating smoothly and price variations limited to around 0.3%. Lending protocols such as Aave had USDe hard-coded as $1 (insulating them from the Binance anomaly).

Ethena Labs reaffirmed that USDe remained overcollateralized throughout the event. Meanwhile, Ethena’s governance token ENA dropped as much as 40% in the immediate aftermath, before beginning to recover.

Notably, Binance’s compensation of $283 million was approved and paid in two waves, covering users affected between 21:36 and 22:16 UTC, plus verified losses on redemptions and transfers. Binance contends the market crash preceded the depeg (i.e., the depeg was not the root cause).

Risk Controls and Exchange Changes

In response, Binance promised several immediate adjustments:

- Incorporating redemption prices into index weights used for collateral pricing

- Implementing a soft price floor in the reference index for USDe

- Switching to external oracles instead of relying purely on its internal orderbook

- Reviewing extreme price movement controls (e.g. limit orders from years ago) that may distort pricing during stress

Furthermore, the incident has unleashed calls for deeper regulatory oversight of centralized exchanges and clearer standards for oracle design.

Broader Implications for Crypto, Stablecoins & DeFi

Oracle Design in Exchanges: A Weak Link

This episode starkly illustrates a key systemic risk: exchange-specific oracles can act as single points of failure. If an exchange references only its own orderbook or narrow liquidity pools, it becomes vulnerable to manipulation, especially under stress or when an attacker controls a large order.

Comparative designs that aggregate across deep pools or implement multi-source validation provide more resilience. In DeFi research literature, the problem of oracle manipulation has been studied (e.g. in SecPLF, securing protocols for loanable funds against oracle attacks).

As more yield-bearing or synthetic assets enter trading venues, collateral systems must carefully consider the reliability, decentralization, and adversarial security of their oracles.

Systemic Contagion via Leverage & Collateral

The USDe depeg and subsequent liquidation cascade show how a local breakdown on one platform can trigger a chain reaction. Even though the depeg was isolated to Binance, the forced unwind fed into broader market panic, margin calls, and a sweeping liquidation of ~$20B across the ecosystem.

It’s a reminder: in highly leveraged environments, collateral design, cross-platform dependencies, and risk buffers are all critical. A local vulnerability can rapidly become a global shock.

Stablecoin Confidence & Reputation Risks

Stablecoins in the crypto system serve as foundational rails: for lending, arbitrage, collateral, settlement, and more. Even a brief depeg can erode confidence, triggering cascading reactions, margin squeezes, and reputational harm.

For newer or alternative stablecoins (especially non-fiat backed or synthetic), their resilience to exchange risk and oracle manipulation becomes a gatekeeper to adoption.

Lessons for New Projects, Investors & Practitioners

- If you’re designing or evaluating a synthetic or yield-bearing token, pay close attention to oracle architecture, especially in how oracles are used for collateral pricing.

- Diversification of data sources (on-chain aggregation, external feeds, fallback oracles) is essential to guard against venue-specific manipulations.

- In trading or investing, be cautious of exchange-specific pricing — arbitrage spreads may hide manipulation risk.

- Be mindful of collateral risk: even seemingly stable assets can become fragile under stress if used in leveraged systems.

- Monitor changes in exchange risk parameters (oracle switches, fee changes, margin rules) — vulnerability windows may open during transitions.

Conclusion

The USDe depeg incident on Binance is a dramatic case study in how local system design choices (especially oracles and collateral systems) can cascade into a full-blown market crisis. While Ethena’s narrative suggests the core protocol held firm and the failure was a venue-level oracle misdesign, the possibility of a coordinated exploit cannot be dismissed. The selective targeting, timing, and cross-exchange contagion all raise red flags that demand further scrutiny.

Beyond this one incident, the event forces us to reexamine how we build robust synthetic assets, oracles, and collateral systems for the next generation of DeFi. For developers, users, and investors alike, the key takeaway is that resilience to oracle failure and minimizing exchange-specific dependencies are now nonnegotiable in designing systems meant to survive stress.

If you like, I can also create a polished version with graphs (using actual price data) and visuals, plus a version tailored to Japanese readers. Would you like me to do that next?