Main Points :

- Leading banks from the U.S., Europe, and Japan are jointly exploring issuing stablecoins pegged 1:1 to G7 currencies.

- The U.S. GENIUS Act establishes the first federal regulatory framework for payment stablecoins, clarifying issuer eligibility, reserve rules, and oversight.

- Banks and financial institutions express both opportunity and caution toward interest-bearing stablecoins and risks to traditional deposits.

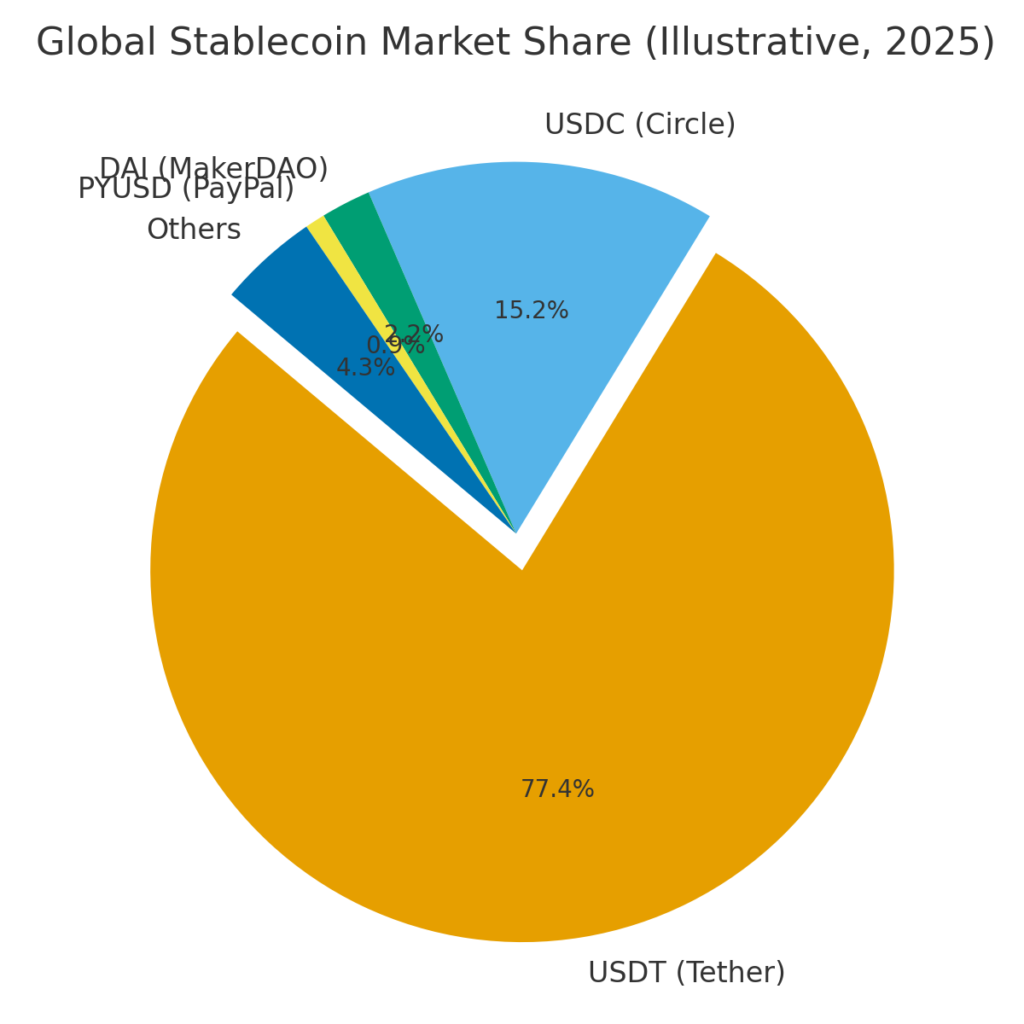

- The existing dominance of USDT, USDC, and DAI faces new contenders in a more regulated environment.

- Broader trends include stablecoin regulatory harmonization (e.g. MiCA in EU), real-world asset tokenization, and stablecoin demand reshaping sovereign bond markets.

Below is a refined, narrative overview, followed by a full Japanese translation.

1. Background: Why banks are eyeing stablecoins

In recent years, stablecoins—digital tokens pegged to fiat currencies or other stable assets—have served mainly as plumbing within the crypto world: a bridge between volatile cryptocurrencies and cash. Their primary use cases have been trading, liquidity routing, DeFi lending, and hedging. But for many institutions, stablecoins have lacked the regulatory clarity and institutional backing needed to cross over into broader financial infrastructure.

Now, a group of major global banks are reportedly exploring whether a new class of highly regulated, fiat-pegged stablecoins—especially those linked to G7 currencies—could become a foundational payment rail on public blockchains. The idea is to combine the stability and trust of major currencies like the U.S. dollar, euro, and yen with the programmability, transparency, and interoperability of blockchain-based money.

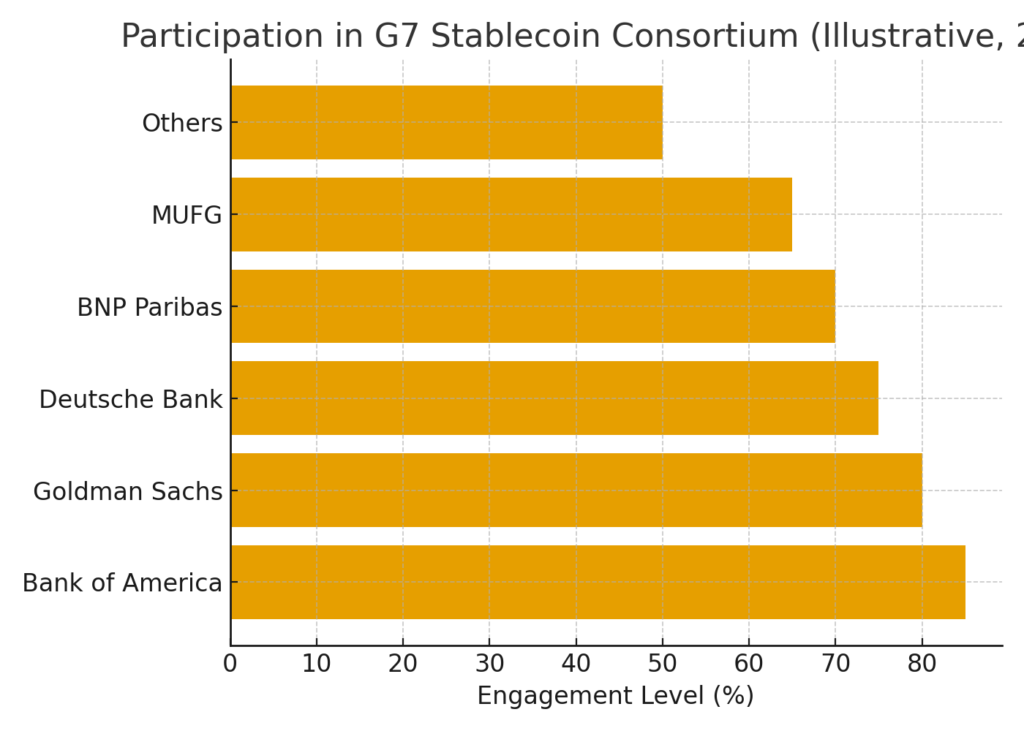

According to Reuters, ten major banks including Bank of America, Goldman Sachs, Deutsche Bank, Citi, UBS, BNP Paribas, MUFG, Barclays, TD Bank, and Santander have joined the initiative. Their shared goal is to explore whether digital currencies backed 1:1 by G7 fiat could function at scale while complying with regulation, managing risk, and preserving competition.

This initiative signals a shift: banks are moving from pilot projects to potentially constructing their own monetary rails—competing (or coexisting) with existing dominant stablecoins.

2. The GENIUS Act: U.S. regulation enters the picture

A key catalyst for institutional interest is the enactment of the GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins Act) in July 2025.

2.1 What the Act does

- It designates “payment stablecoins” a legal class distinct from securities, taking them largely outside the traditional securities laws.

- It restricts issuance of payment stablecoins to federally insured depository institutions, national banks, credit unions, or state banks, and certain regulated nonbank issuers under OCC oversight.

- It mandates that stablecoins be fully backed by liquid assets (e.g. U.S. dollars or U.S. Treasury instruments) and requires issuers to maintain redemption on demand at par (1:1).

- It imposes transparency obligations (e.g. reserve reporting), and subjects issuers to anti-money laundering (AML) and Bank Secrecy Act compliance.

- The law directs the Treasury Department to issue implementing regulations to balance innovation with financial stability, consumer protection, and illicit finance risk mitigation.

Because the GENIUS Act clarifies who may issue a stablecoin and under which conditions, banks now have a clearer legal path forward in the U.S. against a backdrop of otherwise uncertain or fragmented regulatory regimes.

2.2 Opportunities and limitations

The Act is widely considered pro-innovation by crypto proponents, as it reduces legal ambiguity and encourages institutional participation. It also channels stablecoin reserve demand toward U.S. Treasuries, reinforcing dollar dominance.

However, critics warn that the law may not sufficiently protect consumers or prevent concentration of power among large banks or tech firms.

3. Points of tension: interest, disintermediation, and systemic risk

3.1 Interest-bearing stablecoins

One flashpoint is the possibility of interest-bearing stablecoins: tokens that offer yields to holders. In the crypto world, some stablecoins and protocols already allow users to earn returns via algorithmic or lending mechanisms. But banks worry that regulated stablecoins offering yields might cannibalize traditional deposit bases, creating disintermediation or regulatory arbitrage.

Banking stakeholders caution that if depositors shift to yield-bearing digital assets, banks could lose stable funding, potentially stressing the traditional banking model.

3.2 Redemption risk, runs, and peg stability

Banks would need robust designs for liquidity, reserve management, and peg maintenance. In times of stress, mass redemption demands could strain reserves or trigger instability. Ensuring transparent reserves, diversified backing, and credible redemption mechanisms will be paramount.

3.3 Interoperability and competition

A major concern is ensuring that newly issued stablecoins can interoperate across blockchains, wallets, and payment systems. If each bank issues its own siloed coin, fragmentation could reduce utility. The consortium approach intends to mitigate this via a shared standard or governance framework.

In addition, competition with established stablecoins (e.g. USDT, USDC, DAI) will be fierce—unless issuers can offer superior trust, regulatory compliance, or features.

4. Current stablecoin landscape and challenges

4.1 Dominance of USDT and its role in debt markets

Tether’s USDT remains the largest stablecoin by far, with a market capitalization exceeding $178 billion.

Recent academic research shows Tether has become a significant holder of U.S. Treasury bills—roughly $98.5 billion as of Q1 2025—giving it nontrivial influence on short-term Treasury yields. In effect, stablecoin reserve activity is now an active participant in sovereign debt markets.

4.2 Regulatory fragmentation across geographies

While the U.S. now has GENIUS, other jurisdictions use different frameworks:

- In Europe, MiCA (Markets in Crypto-Assets Regulation) took effect in mid-2024 and governs “asset-referenced tokens” and e-money tokens, including stablecoins.

- Several central banks are exploring central bank digital currencies (CBDCs) or regulatory “sandboxes,” adding complexity to how private stablecoins coexist with official digital money.

4.3 Increasing use in DeFi, payments, and tokenization

Stablecoins support decentralized finance (DeFi) by providing low-volatility collateral, enabling lending, swaps, derivatives, and cross-chain bridges. Moreover, as real-world asset (RWA) tokenization grows—e.g. tokenized bonds, real estate, or securitized debt—stablecoins become payment rails or settlement currency in these ecosystems.

5. What’s new: recent developments and case studies

5.1 Bank consortium accelerates G7 project

The joint bank initiative announced in October 2025 is in exploratory phase; no issuance date has been declared yet. The banks describe the effort as a sandbox to evaluate digital asset benefits, market competition, and risk practices.

If implemented, these new stablecoins could directly compete with USDT at scale, but with added regulatory legitimacy.

5.2 U.S. stablecoin expansion by existing issuers

To adapt to the GENIUS Act, major stablecoin issuers are making strategic changes. For example, Tether has announced plans to launch a U.S.-based stablecoin, USAT, issued by Anchorage Digital Bank—structured to comply with the law. This move may allow Tether to maintain market leadership while aligning with new regulatory norms.

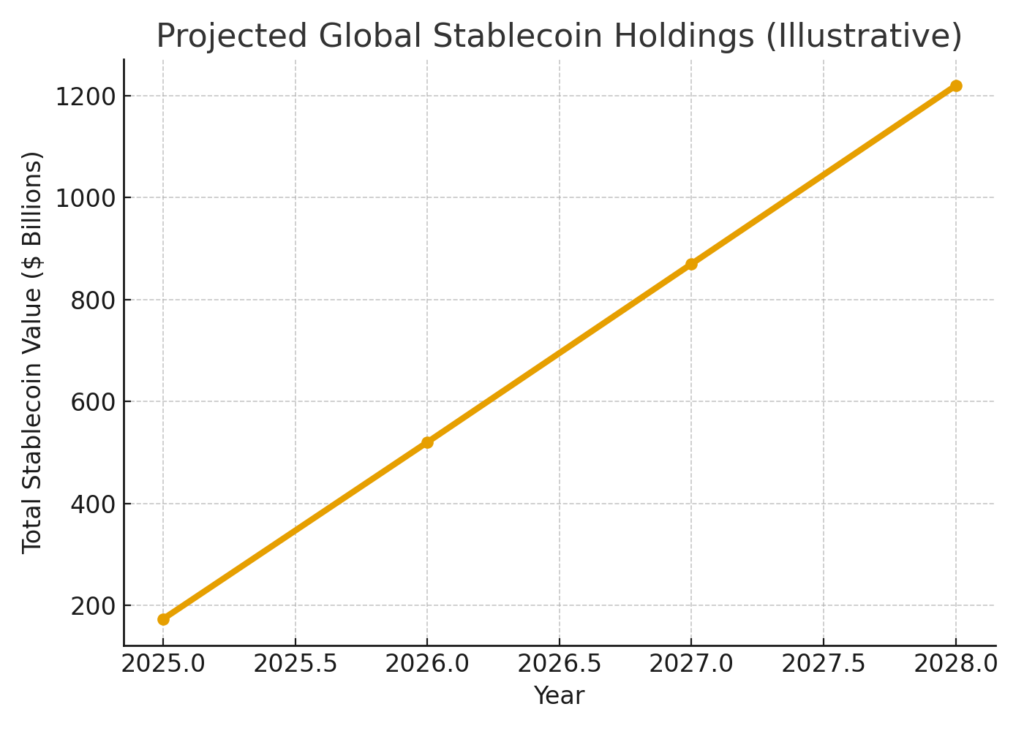

5.3 Macro implications: outflows from banks in emerging markets?

Standard Chartered released a report estimating that U.S. dollar-pegged stablecoins could draw up to $1 trillion out of bank deposits in emerging markets over three years, as users shift toward stable, liquid digital assets. The report forecasts stablecoin holdings rising from $173 billion to $1.22 trillion by 2028 in certain vulnerable economies. This potential capital flight could strain local banking sectors and monetary policy frameworks.

6. Implications for new entrants, developers, and practitioners

6.1 Strategic entry points

If you are considering launching a stablecoin or participating in this infrastructure, here are some promising angles:

- Niche or localized stablecoins pegged to non-G7 currencies or baskets, where large banks have less interest.

- Programmable features (e.g. built-in micropayments, wrapping for tokenization) that traditional banking bonds may struggle to deliver.

- RWA integration: aligning stablecoins with tokenized bonds, real estate, or receivables may yield differentiated utility.

- Permissioned APIs / rails: building middleware that bridges bank-issued stablecoins and DeFi layers.

6.2 Risks and caution areas

- Regulatory compliance burden: Ensuring auditability, AML/KYC operations, redemption guarantees, and governance may require substantial infrastructure.

- Peg robustness: Under stress, maintaining 1:1 redemption is nontrivial; poor design (e.g. over-leverage, illiquid reserves) can lead to collapse.

- Competition and adoption hurdles: With incumbents like USDT and USDC deeply embedded, new coins must offer clear advantages.

- Crossjurisdictional complexity: Ensuring regulatory compliance in the U.S. (GENIUS), Europe (MiCA), Japan, and elsewhere may demand tailored token versions or structures.

7. Conclusion: A turning point for stablecoins and finance

The announcement of a G7-pegged bank consortium, combined with the U.S. GENIUS Act, marks a turning point: stablecoins are no longer fringe crypto instruments—they are being seriously considered as core infrastructure for digital finance. If these bank-backed, regulated stablecoins succeed, they could rewrite how money moves across borders, how value is tokenized, and how institutional adoption unfolds.

However, success is far from guaranteed. Execution risks, regulatory pushback, and competitive dynamics will test whether these projects can deliver both stability and innovation. For developers, investors, and institutions seeking the “next big thing” in crypto, this convergence of banking and blockchain deserves careful attention: the stakes are high, and the opportunity is real.