Key Points :

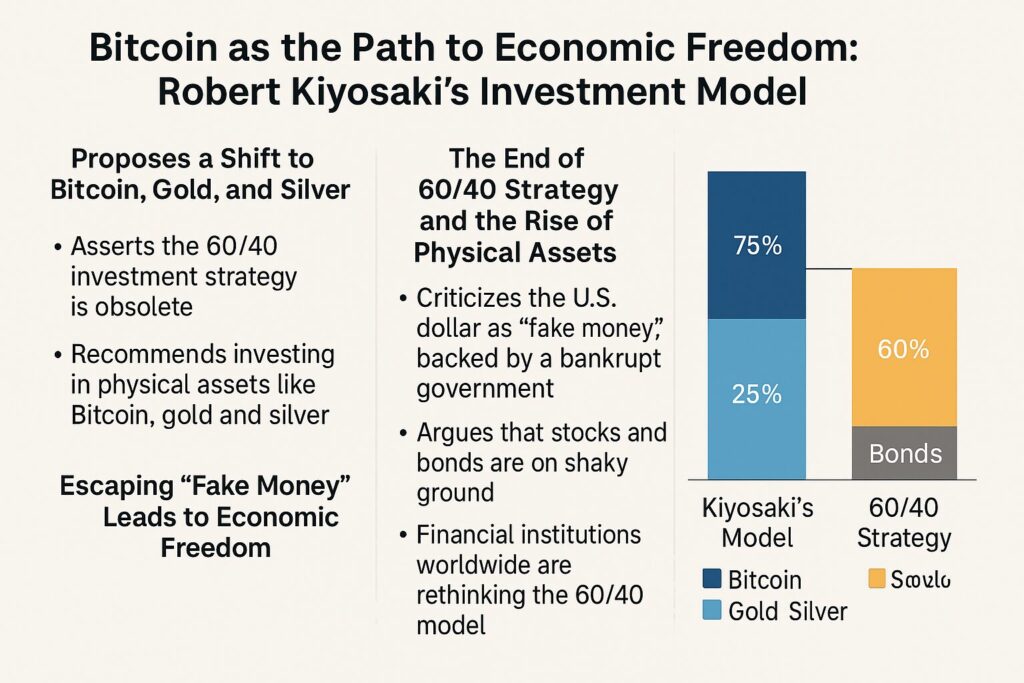

- Robert Kiyosaki argues the classic 60% equities / 40% bonds allocation is obsolete and that “real assets” like Bitcoin, gold, and silver are the new escape hatch from fiat risk.

- He calls the U.S. dollar a “fake money” backed by an indebted government, and sees bonds as IOUs from a bankrupt state.

- Kiyosaki proposes reallocating toward a “75/25” mix of real assets (gold, silver, Bitcoin) and real estate / commodity income streams.

- Institutional and fund-manager behavior is indeed shifting: some advocate new allocations (e.g. 60/20/20 or 50/30/20 with alternatives), and crypto ETFs are seeing record inflows.

- The trend of asset allocation is increasingly toward diversification into digital assets; Bitcoin’s ETF inflows and institutional adoption support this shift.

- But critics argue the 60/40 portfolio still has merit historically, and challenges remain: volatility, regulatory risk, correlation shifts, and portfolio construction complexity.

- For investors seeking next-generation returns, blending real-assets allocations with disciplined risk control, and monitoring emerging strategies (e.g. dynamic rebalancing, sentiment-driven models) may be more viable than a simple “throw into Bitcoin” approach.

- Overall, whether 60/40 is truly dead is debatable. What is clear is that the paradigm is shifting, and crypto and real assets are now central to serious portfolio conversations.

“Bitcoin, Gold & Silver: The Real Assets Turn”

Robert Kiyosaki, author of Rich Dad Poor Dad, recently announced that the era of the 60/40 portfolio is over. He argues that investors should abandon traditional allocations and instead lean heavily into real, tangible assets—chief among them Bitcoin, gold, and silver. According to Kiyosaki, the 60/40 model was already “dead” when the United States severed the link between the U.S. dollar and gold in 1971, and that financial advisors have for decades presented it as a magical cure for retirement security.

Kiyosaki frames the dollar as “fake money” issued by a government that is the world’s largest debtor, and calls bonds the “IOUs of a bankrupt state.” He claims that the only way to preserve and grow wealth is to pivot toward assets outside conventional fiat-based finance—namely precious metals and digital currencies. His personal history underscores this conviction: Kiyosaki says he achieved financial independence decades ago not by relying on the 60/40 formula, but through income from real estate, commodities, and cryptocurrencies.

He specifically proposes reallocating 75% of capital into gold, silver, and Bitcoin, while assigning the remaining 25% to real-estate or other income-producing assets like oil or livestock. This “75/25 strategy,” he argues, is more resilient in the face of a systemic downturn he expects to be one of the greatest crashes in history.

The Critique of 60/40: Is the Old Model Failing Now?

Structural headwinds faced by 60/40

Kiyosaki’s critique hinges on a broader skepticism of fiat-based finance. He sees the U.S. dollar decoupling from gold in 1971 as a turning point, turning currency into an endlessly issuable “fake money.” In his view, stocks and bonds no longer rest on stable foundations. He asks: who buys the bonds of a bankrupt country?

Recent market events may lend credence to that view. The conventional 60/40 mix (60% equities, 40% bonds) has struggled in recent years: falling equity markets coupled with rising interest rates have simultaneously pressured both asset classes. Some analysts argue that the diversification benefits of 60/40 are eroding under new correlation regimes and macro stressors.

For example, in some recent drawdowns, both equities and bonds fell together—a scenario rare historically, but increasingly possible in the current environment. As a result, investment professionals are questioning whether the long-trusted 60/40 formula still delivers the reliability it once did.

Arguments for persistence or adaptation

However, not all experts concede that 60/40 is dead. Some believe that its long-term edge still exists, especially if modified or augmented. For instance, Morningstar published an article in 2025 arguing that 60/40 is “still alive,” especially when adjusted for individual investor needs.Others see merit in variant structures like 60/20/20 or 50/30/20 (i.e. allocating some weight to alternatives or hedges) rather than wholesale abandonment.

Morgan Stanley, for example, has considered the re-emergence of 60/40 under certain scenarios, noting its long historical track record and mean reversion trends. The debate thus centers less on whether 60/40 is wholly invalid, and more on whether it should be the default starting point in modern markets.

Institutional Shifts & Portfolio Innovation

New allocation models gaining traction

Kiyosaki is not alone in calling for a refresh of portfolio norms. Some influential market voices are proposing new allocation models:

- Mike Wilson, CIO at Morgan Stanley, has proposed a 60/20/20 model (60% equities, 20% bonds, 20% gold) to mitigate the weaknesses of bonds in a high-debt, low-rate world.

- Rick Edelman, speaking in a CNBC interview, recommended allocating 10–40% of a portfolio to cryptocurrencies.

- Larry Fink, CEO of BlackRock, has hinted that long-term portfolios may shift to something like 50/30/20 (equities 50%, bonds 30%, alternatives 20%) to accommodate nontraditional assets.

These shifts signal that the industry is actively searching for new defaults rather than sticking to rote rules.

Crypto ETFs: flows and institutional momentum

One of the clearest manifestations of the shift is the surge in capital flowing into crypto exchange-traded funds (ETFs). In the week ending October 4, 2025, global crypto ETFs saw $5.95 billion in inflows. Bitcoin alone attracted $3.55 billion of that, while Ethereum drew $1.48 billion. Others like Solana and XRP also saw meaningful inflows.

Meanwhile, BlackRock’s iShares Bitcoin Trust (IBIT) is nearing $100 billion in assets under management—the fastest ETF in history to approach that mark. As of this writing, it holds nearly 799,000 BTC.

Moreover, the trend is accelerating: inflows into crypto ETFs are already topping previous records. Bitwise forecasts that total inflows for 2025 could exceed those in the ETF’s inaugural year.

(Data Table / Graph Insertion Suggestion)

Insert chart: “Daily / Weekly Bitcoin Spot ETF Net Inflows (USD millions)”

You can use publicly available datasets (e.g. from Farside or The Block) to illustrate the surge around October 2025.

Bitcoin’s evolving role in institutional portfolios

Academic research suggests that Bitcoin is becoming more tightly integrated with traditional finance, altering its status as a pure “alternative” asset. Institutional adoption and corporate treasury strategies have led correlations between Bitcoin and equity indices to rise. In some periods the correlation peaked near 0.87. Further, analysis of firms holding BTC indicates that Bitcoin often acts as a causal “information driver” in return flows.

This evolving correlation profile complicates the narrative of Bitcoin as a purely noncorrelated diversifier. But it also underscores that Bitcoin is maturing into an asset that must be considered in mainstream portfolios—not just as speculative upside, but as part of systematic allocation.

Practical Challenges & Risks

While Kiyosaki’s rhetoric is provocative, the practical implementation of a heavy real-asset / Bitcoin portfolio faces several challenges:

Volatility and drawdowns

Bitcoin and precious metals are far more volatile than bonds. Any portfolio heavily invested in them must tolerate sharp drawdowns. For many investors, that requires robust risk controls, hedging, or dynamic allocation models.

Regulatory & custody risk

Regulation around cryptocurrencies remains unsettled in many jurisdictions. Legal and tax regimes may shift, potentially impairing returns. Furthermore, secure custody of digital assets at scale is nontrivial—especially for institutional investors.

Correlation regime shifts

As previously noted, Bitcoin has started to correlate more with equities, particularly in times of macro stress. Thus, it may not always provide diversification benefits when markets fall broadly.

Portfolio construction complexity

Allocating into real assets and crypto requires more attention to risk, liquidity, rebalancing frequency, and cost structure. A portfolio with 75% in Bitcoin/gold is not simply a mechanical rebalancing play—it demands ongoing oversight and possibly deeper quantitative support.

Skepticism from traditionalists

Many investment professionals caution that abandoning 60/40 entirely may be premature. The 60/40 framework has centuries of historical data supporting it. Critics might argue that real assets and cryptos can complement, but not completely replace, fixed-income ballast.

Toward Smarter Portfolio Architecture

Given both the promise and risks of Kiyosaki’s vision, what might a more practical roadmap look like?

1. Start with a core + satellite model

Rather than discarding 60/40 entirely, many investors might use it as a “core” base and layer a “satellite” allocation into real assets and crypto. For example, maintain a core 40–50% equities and 20–30% fixed income, and allocate 10–20% to alternative buckets (precious metals, Bitcoin, real estate, commodities).

2. Dynamic rebalancing & tactical overlays

Instead of static allocations, use dynamic strategies—rebalancing more aggressively when volatility is stretched, using momentum or regime indicators to shift weights. Some academic work even augments 60/40 via reinforcement learning to improve risk-adjusted returns.

3. Sentiment-based crypto tilts

Recent research has shown that combining sentiment metrics (e.g. from news, social media) with technical indicators can improve crypto portfolio performance. Integrating such approaches may help manage risk in the more volatile parts of the portfolio.

4. Gradual scaling & risk-limited entry

Rather than an immediate 75% shift, investors may prefer scaling allocations over time, using dollar-cost averaging, or introducing caps and drawdown thresholds to protect capital.

5. Constant monitoring of correlation & regime shifts

As correlation regimes evolve, the portfolio should adapt. What works in a bull market may falter in a crisis. Regular reassessment of how crypto and real assets are behaving relative to equity and bond markets is essential.

Conclusion: A Paradigm Shift, Not a Simple Cutover

Robert Kiyosaki’s dramatic declaration that the 60/40 portfolio is dead has stirred debate. His prescription—to tilt aggressively toward Bitcoin, gold, and silver—resonates powerfully with those who believe that fiat money is unstable and modern markets are fracturing under debt stress.

Yet the picture is more nuanced. The 60/40 strategy may not be entirely finished, but it is being tested in a new environment—higher rates, heavier government debt, shifting correlations, and rising demand for alternative assets. Institutional capital flows, crypto ETF inflows, and emerging portfolio structures all point to a rethinking of capital allocation orthodoxy.

For investors seeking next-generation return engines and diversification, the take-home is not to reflexively abandon bonds and equities, but to readjust how much conviction you place in them. A hybrid, dynamic, and intelligently diversified approach that includes real assets and crypto—while respecting risk controls and liquidity constraints—is more likely to survive in the coming era than extremes in either direction.

In short:

- Yes, the 60/40 paradigm is under siege.

- Yes, crypto and precious metals are ascending in investor priority.

- But the wisest path is one of balance, adaptation, and empirical discipline rather than dogmatic overhaul.