Main Points :

- China’s AnchorX launched AxCNH, the first licensed offshore yuan-pegged stablecoin, aiming to power cross-border trade in Belt & Road Initiative (BRI) corridors.

- South Korea’s BDACS launched KRW1, a fully collateralized KRW-pegged stablecoin, on the Avalanche chain, with reserves held at Woori Bank.

- Both new stablecoins adopt overcollateralization with 1:1 backing via fiat deposits or government debt instruments.

- These launches signal an increasing geostrategic role for stablecoins, stepping into currency diplomacy and challenge to dollar dominance.

- Technical and regulatory challenges remain: liquidity, capital controls, cross-jurisdiction compliance, trust in reserves are all critical.

- Looking ahead, stablecoin adoption could expand into real-world asset (RWA) tokenization, central bank digital currencies (CBDCs) interplay, corridor rails, and potentially build an Asia-centric digital currency axis.

1. Introduction: A New Chapter in Stablecoin History

In September 2025, Asia witnessed a notable milestone in the evolution of digital assets: China introduced AxCNH, the first regulated stablecoin pegged to the offshore yuan (CNH), while South Korea rolled out KRW1, a stablecoin tied to the Korean won. These launches are not mere token innovations but strategic moves in a reshaping global financial order, where stablecoins serve both as digital infrastructure and tools of monetary influence.

Until now, stablecoins have largely been dollar-centric (USDT, USDC, BUSD). The sudden arrival of yuan- and won-pegged tokens suggests that nations are beginning to see them not just as crypto utilities, but as instruments linking national currencies to blockchain rails. This development matters to anyone interested in discovering next-generation crypto assets, unlocking new revenue sources, or applying blockchain to real-world finance.

In the following sections, we unpack the details, analyze current trends, and explore practical implications for builders, investors, and real-world users.

2. The AxCNH Launch: China’s Offshore Yuan Enters Blockchain

2.1 What is AxCNH?

AnchorX presented AxCNH on September 17, 2025, during the Belt & Road Summit in Hong Kong. It is described as the first licensed offshore yuan-pegged stablecoin.

The token is pegged 1:1 to CNH, the version of the yuan that circulates outside mainland China and trades freely in global markets (as opposed to the onshore CNY, which is tightly regulated).

To issue AxCNH, AnchorX obtained a license from Astana Financial Services Authority (AFSA) in Kazakhstan.

AnchorX claims that AxCNH is overcollateralized, meaning that custodians hold fiat deposits or government debt instruments exactly equal to the number of tokens in circulation.

2.2 Objectives and Strategic Role

The primary target is to facilitate cross-border settlement within Belt & Road Initiative (BRI) countries. By building a blockchain rail denominated in CNH, China aims to reduce settlement friction, currency conversion risk, and cost.

In that sense, AxCNH can be seen as a digital yuan proxy to deepen yuan’s international usage without fully relying on the Chinese government’s CBDC (e-CNY) in offshore markets.

Its backers and partners include Conflux (which provides blockchain infrastructure), Lenovo, Zoomlion, and others — firms which may test AxCNH in supply chains or cross-border trade scenarios.

Indeed, Zoomlion already conducted a test of AxCNH transfers on the Conflux network between BRI partners.

AxCNH is also listed on ATAIX Eurasia, trading pairs including AxCNH:KZT and AxCNH:USDT (though only for professional clients).

2.3 Challenges and Risks

- Capital controls and liquidity limits: Mainland China still exerts capital controls, and offshore CNH markets are much smaller than USD markets. This constrains scalability.

- Regulatory trust and transparency: Even though AxCNH is overcollateralized, global users must trust the custodial system, audit trails, and reserve integrity.

- Adoption inertia: Dollar-pegged stablecoins already dominate rails and demand; shifting behavior will take time.

- Geopolitical headwinds: Some jurisdictions may resist Chinese-linked financial infrastructure, especially amid U.S. and EU scrutiny.

- Onshore/offshore consistency: The relationship between AxCNH and China’s CBDC or domestic monetary policy must be managed carefully to avoid conflict.

Despite these obstacles, the launch of AxCNH marks a bold experiment: a nation-backed digital currency overlay built on cross-border rails.

3. The KRW1 Launch: South Korea Enters the Stablecoin Arena

3.1 What is KRW1?

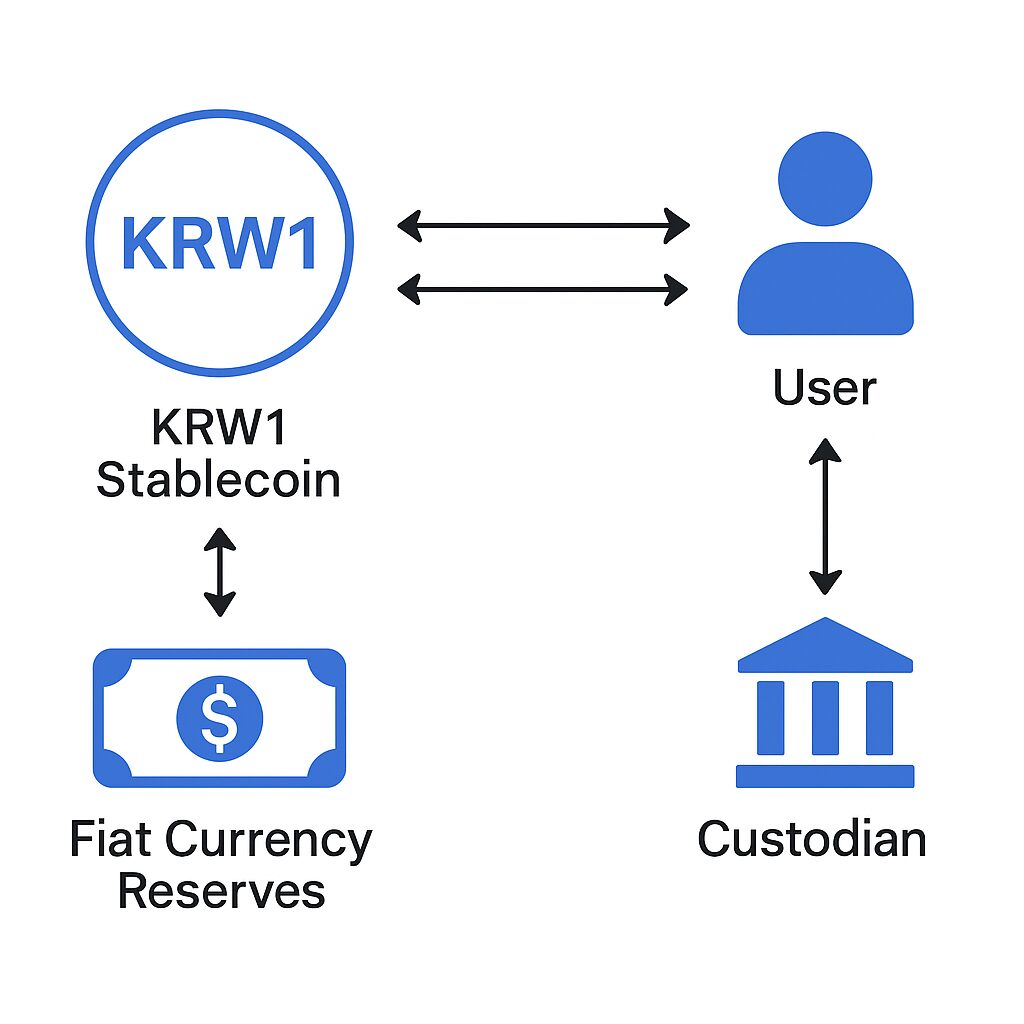

On September 18, 2025, BDACS (Busan Digital Asset Custody Services) launched KRW1, the first stablecoin pegged to the Korean won.

It is fully collateralized with Korean won deposits held at Woori Bank.

KRW1 operates initially on the Avalanche blockchain.

BDACS states that proof of reserves is available via API to allow transparent verification.

The launch followed a proof-of-concept phase, and the company plans to expand its use in remittances, payments, possibly public sector use.

Korea’s financial regulators (the FSC) aim to finalize stablecoin regulation around October 2025, which could provide a legal framework for KRW1’s scaling.

3.2 Significance and Strategic Implications

KRW1 is Korea’s bid to embed the won more deeply into blockchain rails. It gives local firms and investors a domestic stablecoin option rather than relying solely on dollar-pegged ones.

Because reserves are held in a Korean bank (Woori), local users may perceive KRW1 as more trustworthy due to domestic jurisdiction.

Moreover, by launching on Avalanche, BDACS taps into an established blockchain ecosystem, which could ease integration with DeFi protocols and cross-chain bridges.

If regulators support KRW1, it may pave the way for further fintech innovation, payments modernization, and even public sector integration (e.g. tax payments, government disbursements).

However, its success depends heavily on regulatory stability, institutional adoption, liquidity, and market trust, especially in comparison to USD-pegged incumbents with global reach.

4. Stablecoin Context and Market Trends

4.1 Global Stablecoin Landscape

By mid-2025, the stablecoin sector remains dominated by USD-pegged players (Tether, USDC, BUSD, etc.). Many projects had failed or imploded, especially algorithmic and undercollateralized models.

A “cold war” metaphor is emerging: East vs. West stablecoin rails. China’s AxCNH is positioning itself not merely for regional trade, but as a challenge to the dollar’s dominance in blockchain settlement.

Cryptoslate describes AxCNH as leveraging Hong Kong’s stablecoin regulatory regime and focusing more on corridor rails (Asia-Eurasia), rather than solely seeking global market share.

Trend forecasts suggest that by 2028, the global stablecoin market may reach $500 billion to $2 trillion.

4.2 Emerging Themes & Technical Directions

- Corridor rails over universal rails: Projects like AxCNH may focus on specific trade corridors (e.g. China-Central Asia, China-Middle East), rather than competing broadly against USD rails.

- Interplay with CBDCs and RWA tokenization: National stablecoins may interlink with central bank digital currencies (CBDCs) or act as on-chain proxies for real-world assets (RWA).

- Programmable money & smart contract integration: These stablecoins can interface with DeFi, tokenized supply chains, escrow, instant settlement, and composability.

- Regulatory clarity and compliance: More jurisdictions (Hong Kong, Singapore, etc.) are building regulatory frameworks for stablecoins.

- Proof of reserve transparency and auditability: Markets will demand verifiable reserves, possibly via real-time APIs, zero-knowledge proofs, or third-party attestation.

- Cross-chain bridges and ecosystem expansion: To gain liquidity, new stablecoins must integrate across multiple chains and with exchanges, custodians, wallets, etc.

- Risk mitigation by overcollateralization: Given failures of algorithmic models, fully collateralized designs are more credible for now.

5. Use Cases & Practical Adoption Scenarios

5.1 Cross-Border Trade and Supply Chains

Suppose a Chinese exporter wants to pay a supplier in Kazakhstan. Instead of converting CNY → USD → KZT, they might settle in AxCNH → KZT via local rails, thereby reducing conversion hops, volatility exposure, and transaction latency.

Similarly, a Korean firm might pay suppliers or remitters via KRW1 rails internationally, avoiding reliance on USD rails.

5.2 Remittances & Consumer Transfers

For migrant workers or cross-border payments in neighboring countries, local stablecoins can reduce remittance fees and settlement times compared to traditional banking or dollar rails.

5.3 Corporate Treasury & Hedging

Corporations holding yuan or won exposure may use AxCNH or KRW1 as on-chain hedges or liquidity buffers, converting back and forth with fiat as needed.

5.4 DeFi & Lending Markets

If AxCNH and KRW1 are integrated into DeFi protocols (lending, money markets, AMMs), they may provide local stablecoin liquidity. For example, liquidity pools of AxCNH/USDT or KRW1/USDC pairs.

5.5 Government & Public Sector Use

Governments may adopt them for tax collection, welfare disbursement, or as programmable money (conditional transfers) in pilot zones, especially along recognized corridors.

6. Comparative Analysis: AxCNH vs KRW1

| Feature | AxCNH | KRW1 |

|---|---|---|

| Currency Peg | Offshore Chinese yuan (CNH) | Korean won (KRW) |

| Collateralization | Overcollateralized, 1:1 | Fully collateralized, 1:1 |

| Custodian / Reserves | Custodial fiat deposits or government debt | Woori Bank Korean won deposits |

| Blockchain / Network | Uses Conflux, listed on ATAIX, cross-chain ambitions | Avalanche chain initially, with possible expansion |

| Regulatory Path | Licensed via Kazakhstan AFSA, uses Hong Kong venue | Under Korean oversight, FSC rules pending |

| Strategic Focus | BRI cross-border settlement, corridor rails | Domestic rails, regional cross-border payments |

| Risks | Capital control constraints, adoption friction, geopolitical resistance | Regulatory clarity, liquidity competition, trust in bank reserves |

This comparison illustrates different scales and ambitions: AxCNH is grand in scope and geopolitical ambition, while KRW1 is perhaps more modest but potentially more stable in its local rooting.

7. What It Means for Crypto Investors and Builders

- New opportunities for yield and arbitrage: Early liquidity providers or market makers along AxCNH / KRW1 rails may capture spreads, fees, and incentive rewards.

- Asset innovation: Builders could layer synthetic assets, derivatives, or cross-currency swaps built on these stablecoins.

- RWA integrations: Tokenizing real estate or trade receivables denominated in CNH or KRW becomes more seamless with on-chain stable currency rails.

- Interoperability demand: Bridges, cross-chain messaging, and composability will be vital; teams that build robust cross-chain stablecoin infrastructure may find demand.

- Risk evaluation is key: Because these are novel issuances, audit trail, legal enforceability, reserve transparency, and custodial security must be deeply examined.

- Partnerships matter: Adoption may hinge on integration with banks, ERP systems, trade platforms, and governments.

8. Future Outlook & Predictions

- AxCNH may gradually extend to more BRI partner countries. If successful, China might coax additional licensing in Hong Kong, Singapore, or free trade zones.

- KRW1’s regulatory success in Korea will be a bellwether: if the FSC provides clear supportive rules, KRW1 could become complementary to (or competitor of) USD rails in East Asia.

- Over time, stablecoins pegged to other Asian currencies — e.g. HKD, SGD, IDR — may follow suit, leading to a regional stablecoin ecosystem.

- We may see hybrid models, where CBDCs (e-CNY) flow to or from AxCNH under defined rules, merging state money with private rails.

- In the medium term, a digital corridor architecture may emerge: e.g. CNH rails connecting China to Central Asia, Asia to Middle East, etc.

- The success of these projects will push regulators globally to finalize frameworks around stablecoin issuance, reserve rules, and cross-border supervision.

9. Conclusion

The launches of AxCNH and KRW1 mark a bold inflection point in the stablecoin landscape. No longer are stablecoins purely utility tools within crypto; they are becoming tools of monetary strategy, infrastructure for trade corridors, and nodes in a broader digital currency ecosystem.

For builders, these developments offer fertile ground for DeFi primitives, cross-chain protocols, asset tokenization, and new revenue bearings on corridor rails. For investors, early participation in liquidity, market making, and stablecoin ecosystems might be compelling — if performed with careful diligence toward reserve integrity, regulatory risk, and adoption traction.

While challenges abound — from capital controls and regulatory acceptance to liquidity constraints and geopolitical headwinds — the momentum is clear: the stablecoin race is evolving from a dollar monopoly into a multipolar contest. Asia is setting the stage for a new generation of digital currency rails. We are entering a period where national currency meets blockchain — a thrilling frontier for those seeking the next crypto frontier.