Key Points :

- Crypto-focused venture capitalists are reducing risk appetite and avoiding hype projects, placing more emphasis on actual usage and revenue.

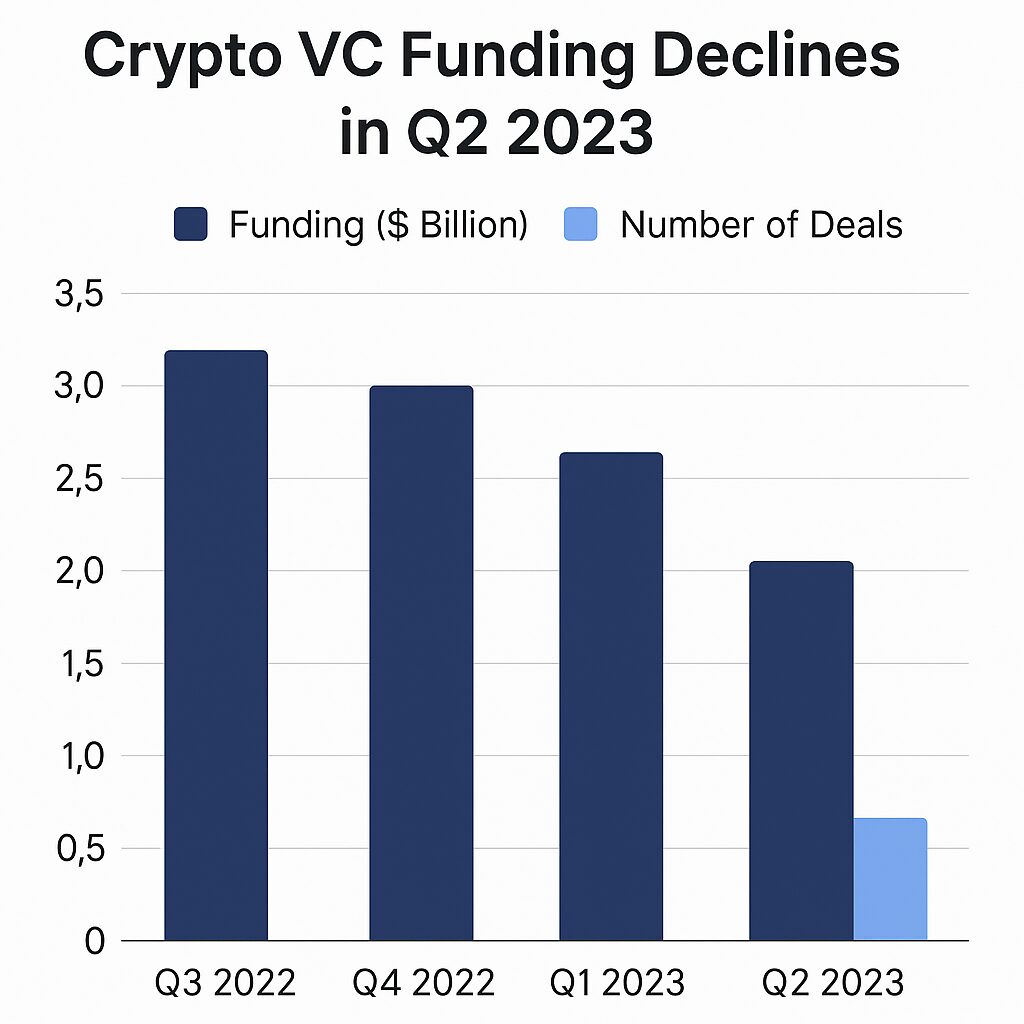

- The volume and number of VC deals in crypto have dropped sharply in 2025, reflecting a more cautious climate.

- VCs now demand clearer business models, demonstrable adoption, and predictable cash flows.

- Investments are shifting toward infrastructure, security, tokenization of real-world assets, and blockchain tools with real utility.

- Hybrid and token + equity financing models continue to evolve, and new on-chain frameworks (e.g. decentralized multi-manager funds) are emerging.

- Regulatory clarity (especially in the U.S. and stablecoin laws) and macro shifts are playing a larger role in shaping investor confidence.

1. The End of Narrative-Driven Investment

In the exuberant years of 2021–2022, many crypto VCs would cut checks based primarily on compelling narratives: “this is the next Layer-1,” “this protocol will be an Ethereum killer,” and so on. But that model is now under pressure. As Sylvia To, Director at Bullish Capital Management, remarked at Token2049, the era of betting on mere storytelling is over. Investors must now ask, “Who is using this? What is the real volume? Can the valuation be justified by actual use rather than projections?”

She observes that while a profusion of chains and infrastructure once appeared exciting, the market is too fragmented and many projects lack substance. In 2025, many startups have raised capital at inflated valuations without solid pipelines or revenue streams. In her view, 2025 has been a “slow year” overall.

This shift is echoed by Eva Oberholzer, CIO of Ajuna Capital, who notes that crypto VCs are now “much more selective” compared to previous cycles. They focus on predictable business models, institutional adoption, and irreversible usage — rather than speculative hype.

In short: narrative as a magnet is weakening.

2. Sharp Decline in Funding and Deals

The quantitative data confirms the mood shift. According to Galaxy Research, in Q2 2025 crypto and blockchain startups raised just USD 1.97 billion across 378 deals, a 59% drop in capital and 15% drop in deal count compared to Q1. That was the second-lowest quarter since Q4 2020.

Moreover, later-stage deals accounted for about 52% of the capital, with early-stage investments making up the balance.

While Q1 2025 had been buoyed by a USD 2 billion investment by sovereign-linked MGX into Binance (which distorted the comparison), even then the downward trend is evident.

This drop reflects not just caution, but triage: VCs are reallocating capital toward fewer but higher-conviction bets.

3. What VCs Now Prioritize: Utility, Revenue, Adoption

The narrative shift has brought with it a new rubric for evaluation. VCs increasingly demand:

- Demonstrable usage / adoption — Who is using the protocol? Are there real users and meaningful volume?

- Predictable revenue or monetization models — The business model should not rely solely on future token price appreciation.

- Institutional engagement — Projects that support or rely on institutions (e.g. enterprises, financial players) are preferred.

- A defensible moat in infrastructure, security, or protocol tech — As opposed to superficial features or gimmicks.

These demands favor companies with traction (or at least early product-market fit) and pragmatic roadmaps rather than speculative visions.

One domain drawing continued interest is tokenization of real-world assets (RWAs). Projects that convert real assets (real estate, commodities, securities) into digital tokens—with clear legal and compliance frameworks—are increasingly appealing.

Similarly, infrastructure layers (such as oracles, privacy modules, cross-chain bridges) and protocols improving security, scalability, or interoperability are favored over copycat applications.

4. New Models, Emerging Frameworks

While the landscape tightens, innovation in financing and architecture continues. Crypto VCs increasingly blend token-based investments and traditional equity warrants, rather than choosing one exclusively. This allows alignment with on-chain incentives while preserving conventional upside.

At the same time, new frameworks are appearing on-chain. For instance, a recently proposed decentralized multi-manager fund framework lets vaults accept capital, allocate to strategy modules, validate performance, and dynamically reallocate—all in an automated, on-chain fashion. It blends asset management concepts with chain-native design.

These architectural evolutions suggest the next frontier: autonomous capital allocation, composable protocol layers, and hybrid token–equity structures.

5. External Factors: Regulation, Macros, and Institutional Signals

The stricter VC posture is not happening in a vacuum. Several macro and regulatory shifts are amplifying caution:

- In the U.S., the GENIUS Act (passed July 2025) establishes stricter rules for stablecoins—requiring full backing in low-risk assets, transparency, and dual federal-state oversight.

- The push for crypto regulation and stablecoin clarity increases confidence in projects targeting real-world finance bridges.

- The U.S. has also floated proposals around strategic crypto reserves (e.g. a U.S. crypto reserve) that may lend symbolic legitimacy to the sector.

- In terms of capital trends, some firms are shifting toward digital asset treasuries (i.e. holding crypto on balance sheets) rather than startup investing.

- M&A activity is increasing—larger firms acquiring smaller startups as exit paths become more constrained.

- Meanwhile, regulatory clarity in key jurisdictions helps reduce legal risk and encourages more deliberate project structuring.

Thus, the external environment incentivizes projects with sound compliance, realistic economics, and resilient business models.

6. What This Means for Entrepreneurs and Investors

For those seeking the next crypto investment or building a new protocol, here are practical implications:

For Founders / Builders

- Focus on real traction early: even minimal usable flows help validate your thesis with disciplined investors.

- Design revenue models, even if small or preliminary, rather than leaning on exponential token price assumptions.

- Modular, composable infrastructure work tends to accrue value—protocol plumbing doesn’t get replaced every cycle.

- Hybrid token + equity structures may make your startup more acceptable to cautious VCs.

- Build defensibility through moats (e.g. strong cryptography, integration partnerships, compliance edge).

- Prepare for stronger due diligence—technical, usage, legal, tokenomics will be scrutinized more.

For Investors / Allocators

- Move past hype and develop refined frameworks to screen for real adoption, risk, and business viability.

- Allocate more to later-stage rounds or follow-on investments in proven names.

- Be open to on-chain fund models or algorithmic capital allocation structures (e.g. multi-manager funds).

- Monitor regulatory developments closely—projects that align early with good compliance may offer risk-adjusted differentiation.

- Consider investing in bridging infrastructure, real-world tokenization, privacy, composability—that is, the rails, not just the apps.

Latest Developments & Examples (2025 Highlights)

- The Ether Machine: A merged vehicle backed by crypto institutions is going public via SPAC, with more than 400,000 ETH on its balance sheet. This reflects institutional appetite for transparent crypto exposure.

- Sygnum raised USD 58 million and attained a USD 1 billion valuation—emphasizing institutional crypto infrastructure as a resilient vertical.

- Rain, the stablecoin-linked card issuer, expanded chain support and raised significant capital, underscoring fintech + crypto convergence.

- Kazakhstan launched its first regional crypto fund, in partnership with Binance, signaling state-level backing of crypto finance.

- M&A in Web3 has accelerated, as tech firms acquire infrastructure startups to absorb talent and capabilities.

- On-chain research continues to progress: for example, vote delegation behavior in DAOs is being dissected academically (finding that reputation, and ties to VC firms, still influence delegation).

- Multi-agent AI systems are being developed to manage crypto portfolios with better risk-adjusted returns, offering a glimpse of automated investing’s future.

These examples illustrate that the new winners are less about marketing and more about structural substance.

Conclusion: A New Era of Discipline in Crypto VC

The era of easy narrative-driven investments is evolving into one of discipline, rigour, and real use. Crypto VCs in 2025 are no longer willing to back stories alone—they demand demonstrable adoption, defensible business models, and credible tokenomics. The data confirms this: funding has contracted, deals are fewer, and capital is concentrating on later-stage, high-conviction projects.

For entrepreneurs, that means delivering early traction, aligning your token-economic design with real utility, and structuring for deeper scrutiny. For investors, it means rebuilding evaluation frameworks that emphasize fundamentals, not FOMO. And for the ecosystem overall, it marks a maturation: a transition from speculative dreams to sustainable infrastructure.

If you like, I can generate a full infographic or updated charts for funding trends (2023–2025) or suggest specific new crypto projects that seem to meet this stricter VC bias. Would you like me to do that?