Key Takeaways :

- Fed Governor Waller positions stablecoins as an “essential” component of future U.S. payment rails

- The GENIUS Act, passed in July 2025, establishes the first federal regulatory framework for payment stablecoins in the U.S.

- Waller and other U.S. regulators emphasize private-sector innovation, risk management, and industry collaboration

- Internationally, stablecoin adoption is accelerating, especially for remittance and cross-border settlement

- Key challenges remain: cybersecurity, interoperability, monetary sovereignty, and global regulatory alignment

- Market players are already responding: e.g. Tether’s plan to launch a U.S.-compliant stablecoin (“USAT”) under GENIUS

1. Framing the Debate: Why Waller Calls Stablecoins “Essential”

At the Sibos conference in Frankfurt on September 29, 2025, Federal Reserve Governor Christopher Waller made headlines by declaring that stablecoins are essential to the future of U.S. payments. He presented them not as a threat to existing payment systems, but as a complementary “private sector innovation” that can coexist with and enhance traditional rails. Waller emphasized that if a stablecoin can be reasonably deemed safe, low risk, and accepted by consumers, it can function alongside credit cards, debit, and bank transfers without necessarily displacing them.

Waller has previously argued that increasing competition in payments — including from nontraditional entrants — could help reduce costs, especially for cross-border and remittance flows. He noted that in jurisdictions with limited banking access, dollar-pegged stablecoins already serve as practical alternatives.

He also underscored the importance of digital platforms being resilient, secure, and robust to cyberattacks, particularly as new rails integrate tokenized assets, smart contracts, and stablecoins.

His overarching position: the Fed supports innovation, but cautiously — with appropriate regulation and risk oversight built in.

2. The GENIUS Act: U.S. Stablecoin Regulation Enters the Mainstream

2.1 Overview and Key Provisions

In July 2025, President Donald Trump signed into law the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act), the first significant federal stablecoin legislation in the U.S.

Some of the major features of the GENIUS Act are:

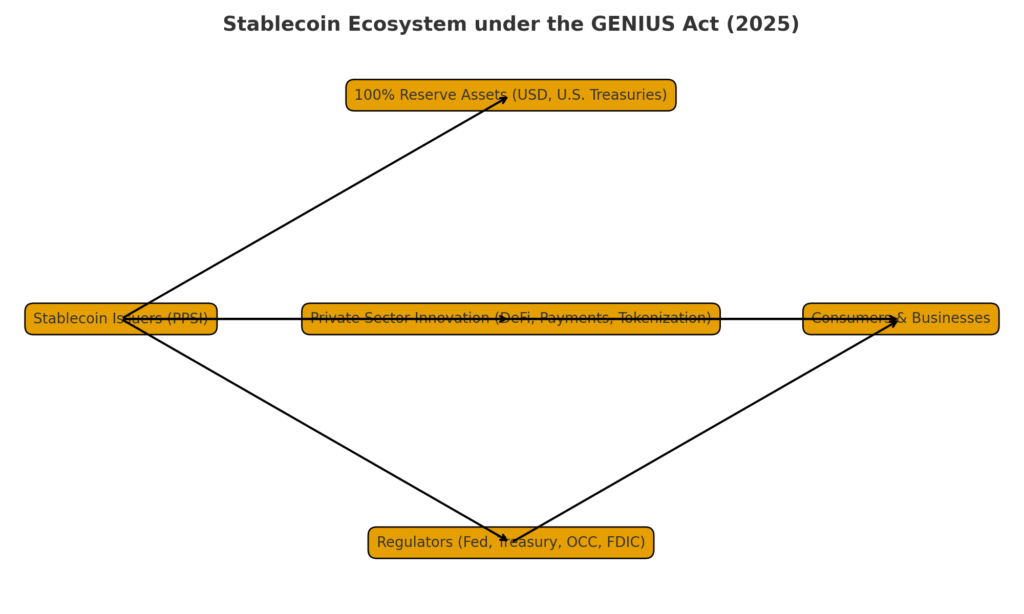

- It defines payment stablecoins (tokens used or designed for payments or settlement) and requires issuers to maintain a fixed‐value conversion or redemption promise.

- Only Permitted Payment Stablecoin Issuers (PPSIs) may issue payment stablecoins in the U.S. (with some limited exceptions).

- PPSIs must meet capital, liquidity, and reserve requirements similar to regulated financial institutions.

- 100% backing of reserves is required, in liquid assets such as U.S. dollars or short-term Treasuries.

- Issuers must make monthly public disclosures regarding reserve composition, and marketing of stablecoins must avoid misleading claims (e.g. falsely advertising federal backing).

- In case of insolvency, stablecoin holders’ claims are prioritized over other creditors.

- The law restricts digital asset service providers from offering or selling payment stablecoins from foreign issuers unless the foreign issuer operates under a regime “comparable” to U.S. rules.

The GENIUS Act also delegates key regulatory and supervisory responsibilities to U.S. agencies such as the Treasury, the Federal Reserve, the FDIC, and the OCC (Office of the Comptroller of the Currency). It requires the Treasury to issue implementing regulations and define comparability standards for foreign regimes.

Implementation is expected to begin no later than January 18, 2027 (or 120 days after the first rules are issued), although stablecoins may gradually begin to comply earlier.

2.2 Implications for Market Participants

The GENIUS Act gives clarity to what stablecoin issuers must satisfy in the U.S., reducing regulatory uncertainty that has long weighed on the market.

However, compliance is likely to be costly, especially for reserve management, audit transparency, capital buffers, and regulatory examinations. Smaller projects may struggle to meet scale or oversight requirements.

Foreign issuers seeking U.S. access will need to align with comparable regimes or partner with U.S. entities — thereby reshaping cross-border stablecoin strategies.

Interestingly, the requirement of 100% liquid backing and interest in U.S. Treasuries may also shift capital flows: as stablecoin issuers accumulate Treasuries to back liabilities, they may become significant participants in government debt markets. Indeed, Tether already holds a large Treasury portfolio, and recent research suggests that its holdings may influence short-term yields.

3. U.S. Vision: Innovation, Private Sector Leadership, and Risk Management

Waller and his colleagues portray an ideal in which private firms drive payments innovation, while public regulators ensure robust guardrails. Waller’s remarks often stress that the government should not pick winners or build rails directly, but rather support experimentation and industry-led design.

He also repeatedly raises risk vectors inherent in digital payments:

- Cybersecurity and operational risk: As new rails integrate smart contracts, tokenized assets, and automated flows, platforms must be hardened against attacks.

- Resilience and redundancy: Payment systems must be built with fallback mechanisms, redundancy, and interoperation in mind.

- Financial stability concerns: If stablecoins grow large, sudden redemptions or market stress might impact monetary policy or bank balance sheets.

The Fed plans to host a Payments Innovation Conference in October 2025 that will bring industry, regulators, and technologists together to discuss stablecoins, tokenization, DeFi, and infrastructure.

This signals that the U.S. intends to evolve its payments infrastructure collaboratively, not unilaterally.

4. Global Landscape & Emerging Use Cases

4.1 Cross-Border Payments and Remittances

Stablecoins are gaining traction globally, particularly in regions with limited banking infrastructure or high remittance flows. In 2024 and 2025, several announcements show the growing role stablecoins are playing in payments:

- PayPal’s PYUSD is being used for cross-border disbursements via its Xoom arm, enabling settlement in stablecoin rails outside traditional banking hours.

- In Southeast Asia, partnerships between infrastructure companies (like StraitsX), e-commerce platforms, and wallets have launched stablecoin-driven payments for merchants.

- Japanese banks have piloted stablecoin-based cross-border transfers, leveraging blockchain rails instead of correspondent banking.

These moves underscore that stablecoins can reduce settlement time, friction, and cost, particularly for small-value payments or remittances where traditional correspondent banking is inefficient.

4.2 Diverging Regulatory Approaches

While the U.S. embraces stablecoins as payment innovation, Europe has taken a more cautious stance. The EU’s MiCAR (Markets in Crypto-Assets Regulation), effective since mid-2024, governs e-money tokens and asset-referenced tokens, placing stricter oversight on stablecoin issuance.

European central bankers have voiced concerns over “monetary sovereignty” and the risk that external stablecoins may displace domestic currency systems. For instance, at Sibos 2025, the European and U.S. central bankers debated strongly — Waller championing private stablecoins, and Bundesbank President Nagel warning of risks to monetary control and financial stability.

The contrast underscores a global tension: whether stablecoins should be unleashed to drive innovation or tightly guarded to protect monetary control.

5. Market Moves: How Players Are Reacting

5.1 Tether’s U.S. Push: “USAT”

In September 2025, Tether (the issuer of USDT) announced its plan to launch a U.S.-based stablecoin called USAT, designed to comply with the GENIUS Act. It will be issued by Anchorage Digital Bank (a U.S. trust bank with national charter) and governed by U.S. rules.

USDT itself, as a foreign issuer, plans to remain compliant via reciprocity provisions under GENIUS. The launch of USAT reflects how major stablecoin issuers are repositioning to stay competitive in the U.S. market under the new regulatory regime.

5.2 Treasury Demand & Yield Impacts

As noted earlier, stablecoin issuers’ need for U.S. Treasuries to back reserves has real macro consequences. Tether already holds tens of billions in U.S. Treasuries, which may affect short-term yields — some research suggests a link where increases in stablecoin issuer holdings are associated with yield compression.

If stablecoin scale expands further, systemic impacts on government debt markets, interest rates, and capital flows are possible.

5.3 Institutional and Infrastructure Responses

- Payment incumbents (banks, fintechs) may seek to integrate with or issue stablecoins to stay competitive.

- Blockchain infrastructure firms, layer-1 protocols, and smart contract platforms will continue to compete for stablecoin issuance frameworks (through token standards, gas costs, and auditability).

- Regulatory tech firms will play a bigger role: compliance, disclosure automation, reserve auditing, and interoperability protocol design.

6. Challenges and Open Questions

6.1 Interoperability & Network Effects

For stablecoins to become primary payment rails, interoperability between blockchains, legacy systems, and rails (e.g. ACH, SWIFT) is critical. Without it, fragmentation will limit utility.

6.2 Cybersecurity and Operational Risk

The integration of smart contracts and tokenization increases the attack surface. Zero-days, protocol errors, or oracle exploits could propagate across rails. Regulators will expect strong risk mitigation and incident response planning.

6.3 Monetary Sovereignty and Systemic Risk

As stablecoins scale, central banks might lose influence over money supply, interest rates, and liquidity. In crises, mass redemptions or “runs” might stress banks or payment systems. This concern is especially acute in smaller economies.

6.4 Regulatory Alignment & Global Coordination

GENIUS is U.S.-centric; ensuring cross-border stablecoins and global coordination (e.g. recognizing foreign stablecoins, harmonizing rules) remains difficult. Differences in legal frameworks and monetary authorities complicate reciprocity.

6.5 Cost and Compliance Burden

Meeting capital, audit, disclosure, and cybersecurity requirements may favor large incumbents. Smaller, niche, or decentralized stablecoins may find entry difficult.

7. What This Means for Crypto Innovators & Revenue Seekers

7.1 Building Compliant Stablecoins in the U.S.

If you are considering launching or integrating a U.S. dollar–pegged stablecoin in the U.S. market, GENIUS gives you a blueprint. You’ll need:

- Full liquid reserves (dollars, Treasuries)

- Transparent reserve disclosures

- Back-office infrastructure for compliance, audits, KYC/AML

- A structure as a Permitted Payment Stablecoin Issuer (or partnership with one)

While challenging, compliance also offers legitimacy, institutional on-ramp, and potential for widespread adoption.

7.2 Interoperability and Infrastructure Plays

Projects that facilitate interoperability, bridging, cross-chain liquidity, and auditability will be in high demand, especially as stablecoins seek to scale across blockchains and connect with legacy financial rails.

7.3 Regional & Cross-Border Use Cases

Markets with weak banking systems, expensive remittance corridors, or cross-border trade inefficiencies are fertile ground. Building stablecoin rails for remittance corridors or cross-border settlement (e.g. Southeast Asia, Latin America, Africa) may deliver real traction.

7.4 Compliance & RegTech as a Differentiator

Offering modular compliance, automated disclosure tools, insurance, reserve validation, and audit transparency can become selling points. Projects that ease the burden for stablecoin issuers will find demand.

7.5 Tokenization & DeFi Synergies

Stablecoins often serve as the “plumbing” for DeFi: lending, collateral, derivatives, payments. Innovators that integrate stablecoin rails seamlessly into DeFi applications (with regulatory guardrails) can capture value.

8. Toward a New U.S. Payment Topology: Vision and Risks

The combination of Waller’s advocacy and the GENIUS Act signals a U.S. shift toward a public‐private hybrid payments infrastructure, where regulation ensures safety and stability, but innovation stems from private actors.

However, the transition is not risk-free. The path ahead must navigate:

- Scaling secure, robust platforms

- Achieving interoperability across chains and existing finance

- Preserving monetary sovereignty

- Managing cyber risk

- Ensuring global bridges and regulatory alignment

If successfully navigated, stablecoins could become integral to U.S. payments, drive financial inclusion, reduce cross-border friction, and invite renewed innovation in digital money.

Conclusion

The recent remarks by Fed Governor Waller, combined with the passage of the GENIUS Act, mark a turning point in how the U.S. views stablecoins: not as speculative assets, but as foundational infrastructure for future payments. The legal clarity delivered by GENIUS now offers a regulatory playground for innovation — especially for those who can marry compliance with technical excellence.

For innovators and revenue-seekers, this is a moment to think big: whether you’re designing compliant stablecoins, building bridging or auditing tools, or targeting underserved corridors, the structure is taking shape. But success will depend on balancing ambition with prudence: networks must be resilient, regulators engaged, and interoperability seamless.

Stablecoins may yet realize their promise as the digital backbone of next-generation payments — both in the U.S. and globally.