Key Highlights :

- ChinaAMC Hong Kong launched a tokenized money market fund (CUMIU) on Ethereum, backed by ~$500M assets

- They extended to USD- and RMB-denominated tokenized MMFs, becoming a regional first for RMB

- China’s regulators have informally requested brokerages to pause RWA tokenization in Hong Kong

- The global RWA tokenization market is booming in 2025, with billions on-chain and rising institutional activity

- But significant challenges remain: liquidity, regulatory complexity, cross-chain friction

- Academic frameworks point the way to future RWA infrastructure: cross-chain identity, decentralized multi-manager funds

1. Setting the Stage: ChinaAMC and the CUMIU Tokenized MMF

In a bold move, China Asset Management (Hong Kong) launched the ChinaAMC USD Digital Money Market Fund Class I (CUMIU) on Ethereum. The fund pools capital into short-term deposits and high-grade money market instruments, aiming to produce stable USD returns while preserving liquidity and capital protection.

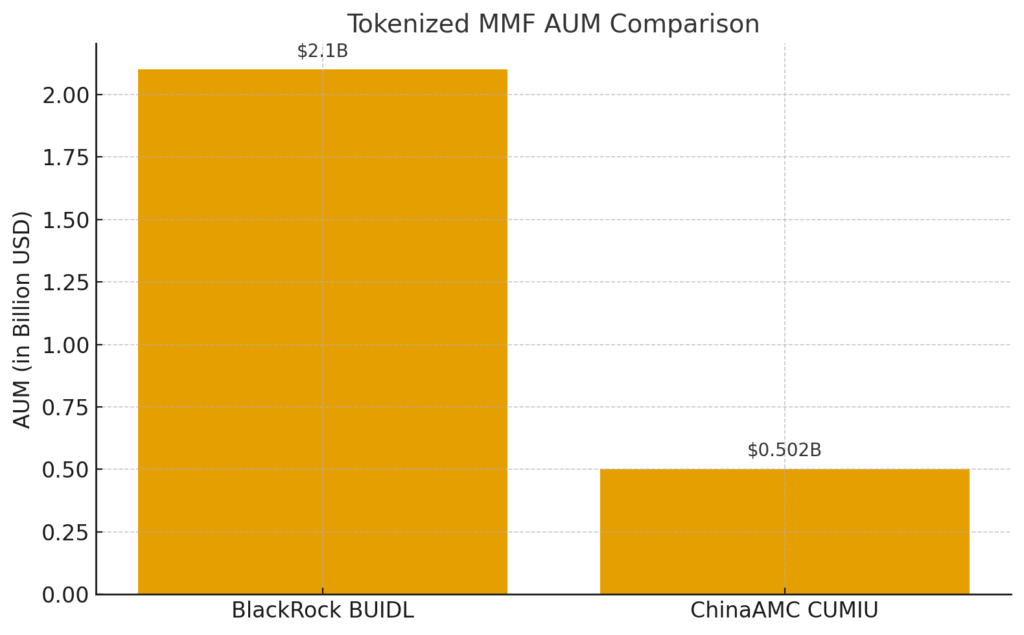

Every token is anchored to a $100 net asset value, and the platform charges a mere 0.05% annual fee. As of August, the fund had raised approximately $502 million, placing it among the largest tokenized funds globally (about 11th by size).

Interestingly, only two institutions currently hold CUMIU tokens, with public availability likely restricted by design. This controlled deployment strategy suggests that ChinaAMC is gradually validating settlement, compliance, and blockchain operations prior to broadening investor access.

ChinaAMC’s ambitions don’t stop with USD. In mid-2025, it introduced USD- and RMB-denominated tokenized MMFs to complement its existing HKD version. The RMB fund is claimed to be the world’s first tokenized RMB money market fund. Standard Chartered has joined as an asset service provider.

These tokenized funds are distributed not only through conventional brokers and banks but also via Virtual Asset Trading Platforms (VATPs) regulated in Hong Kong—effectively bridging traditional finance and crypto retail infrastructure.

ChinaAMC also operates a Hong Kong Ethereum ETF approved by the SFC, which includes staking capabilities—indicating a broader roadmap for integrating digital finance into legacy asset management setups.

2. Regulatory Undercurrents: The CSRC’s Quiet Pushback

While Hong Kong has sought to cultivate a crypto-friendly regulatory environment, Beijing’s appetite for such innovation is more cautious. According to Reuters, the China Securities Regulatory Commission (CSRC) has informally advised at least two major brokerages to pause their RWA tokenization initiatives in Hong Kong. The rationale? Strengthening risk controls and demanding that tokenization ventures are backed by sound business models.

This signals a divergence in policy orientation: Chinese regulators aim to prevent runaway capital outflows or unregulated speculative digital asset proliferation, especially via offshore jurisdictions. Although crypto trading and mining are banned in China proper, Hong Kong remains more liberal—which may create tensions.

Because the CSRC’s directive is informal (not a formal law), the timeline and permanence of any pause remain uncertain. That ambiguity is a key risk factor for firms trying to build crypto-native finance products with mainland Chinese capital.

3. The RWA Tokenization Boom in 2025

3.1 Market Expansion & Metrics

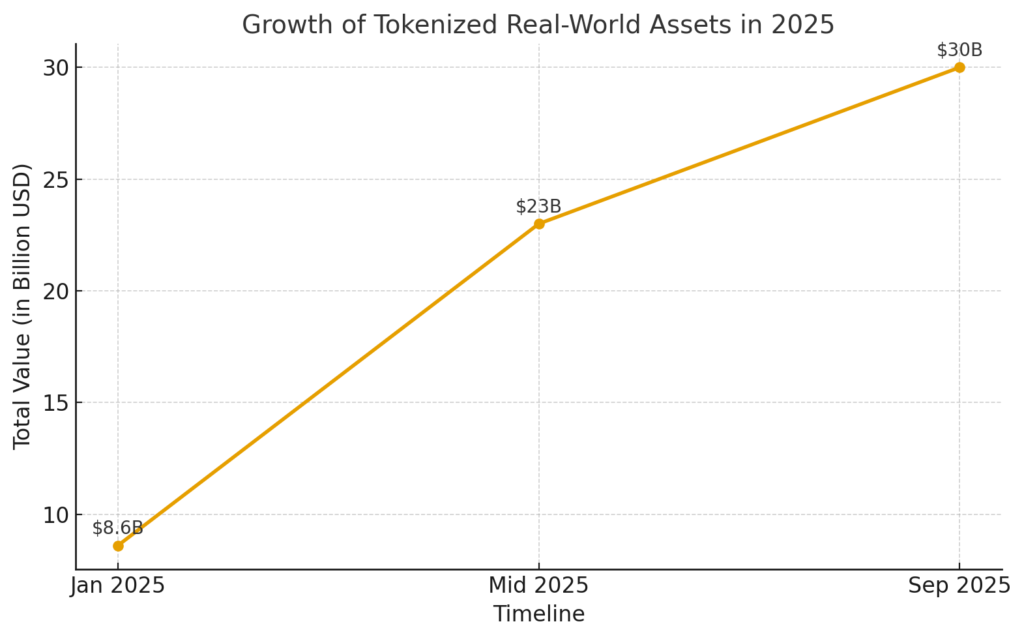

The RWA tokenization sector has exploded in 2025. Beginning the year with approximately $8.6 billion in tokenized assets, the market ballooned to over $23 billion, representing a 260% year-to-date growth. In parallel, RWA.xyz reports that total on-chain RWA assets have recently surpassed $30 billion.

A large proportion of the growth is concentrated in tokenized Treasury and money market instruments. For instance, the value of tokenized Treasury products is estimated to have increased 80% during 2025, reaching about $7.4 billion in assets. BlackRock’s BUIDL token has played a pivotal role: climbing from $649 million to ~$2.9 billion in 2025.

3.2 Leading Use Cases

- Tokenized Treasuries & Short-Term Debt: These remain the anchor of the RWA space. Their low credit risk and familiarity make them attractive for blending on-chain yield with traditional safety.

- Private Credit & Syndicated Loans: Developers are tokenizing portions of private credit deals and syndicated loans to democratize access and liquidity.

- Real Estate / Asset-Backed Structures: Projects are underway to tokenize property, infrastructure, or mortgage-backed assets—but real-world legal, jurisdictional, and operational hurdles slow their momentum.

- Collateralization & DeFi Extensions: Tokenized RWAs are being used as collateral in lending, or as components in composable DeFi financial architectures.

GrowthTurbine notes the 2025 wave of tokenized yield instruments includes treasury bills, syndicated loans, and yield-bearing debt instruments aiming to diversify income sources.

3.3 Academic & Infrastructure Innovation

- Cross-Chain Identity & Authentication (xRWA): A new academic proposal outlines how to enable RWAs to traverse blockchains without repeated verification, using Decentralized Identifiers and Verifiable Credentials.

- Modular Decentralized Fund Architectures: Another framework proposes permissionless, multi-strategy tokenized vaults managed by human or AI agents using a layered on-chain architecture.

- Liquidity & Tradability Studies: A recent study warns that many RWA tokens, despite being issued, struggle with liquidity, narrow transferability, and low secondary trading activity.

These research directions address the next frontier: creating robust, interoperable, and liquid RWA infrastructures.

4. What This Means for Crypto Investors & Practitioners

For those seeking next-generation crypto yield or token innovations, the RWA space offers intriguing possibilities:

4.1 Yield + Composability: A “Best of Both Worlds”

Tokenized MMFs (like ChinaAMC’s, or BlackRock’s BUIDL) function as on-chain yield assets. That means they can be composable—used as collateral, leveraged, or integrated within DeFi pipelines—while earning real financial income rather than synthetic yields.

For example, instead of parking capital in stablecoins (which often produce little or no yield), an investor might hold a tokenized MMF that pays interest, while still using it within DeFi protocols.

4.2 Democratizing Access to Institutional Products

Tokenization fragments minimums, permitting fractional investments in traditionally inaccessible products (e.g. treasuries, privatized credit, real assets). This opens new doors for smaller investors or institutional participants to diversify.

4.3 Infrastructure & Token Plays

Beyond the underlying assets, the enablers—platforms, oracles, bridge protocols, identity systems—represent token opportunities. Projects building secondary markets for RWA tokens, liquidity engines, or cross-chain bridges may become essential plumbing.

4.4 Risks & Governance Sensitivities

- Regulatory Uncertainty: As seen in China’s case, policy shifts can abruptly hamper operations or access. Jurisdictions matter deeply.

- Distribution / Whitelisting Controls: Many RWA token models restrict transferability or require whitelisting, limiting full “permissionless” aspirations.

- Liquidity Constraints: Low trading volume and narrow investor bases can trap capital or prevent exit.

- Custodial & Valuation Trust: Dependence on audited custodians, on-chain oracles, and transparency remains critical for credibility.

Hence, investors should approach with cautious allocation, deep due diligence, and awareness of jurisdictional rules.

5. Recent Cases & Illustrations

- RMB Tokenized Fund Launch: The launch of ChinaAMC’s RMB-denominated tokenized MMF in 2025 marks a watershed moment, adding a currency variant to tokenized finance arms.

- Wall Street Entry: Goldman Sachs and BNY Mellon built a private-blockchain setup for tokenized money market funds via mirror tokens, signaling institutional experimentation.

- Regulation Interference: The CSRC’s informal pause on Hong Kong RWA launches underscores the importance of mainland policy in global tokenization strategies.

- Liquidity Warning: Academics highlight that many tokenized assets sit illiquid, emphasizing that issuance is only step one.

- Innovative Protocol Designs: Cross-chain xRWA systems and decentralized multi-manager fund architectures point toward scalable, composable RWA futures.

6. Conclusion & Outlook

ChinaAMC’s push into tokenized MMFs—starting from Ethereum with CUMIU and expanding to USD/RMB denominated versions—signifies that tokenized finance is shifting from speculative experiment to institutional-grade asset class. The involvement of global banks and asset managers further reinforces this trajectory.

Yet, the path is neither simple nor guaranteed. Liquidity, regulatory clarity, cross-chain interoperability, and trust remain major hurdles. Academic and technical innovation (e.g. xRWA, decentralized fund frameworks) is essential to unlock the next level of efficiency and accessibility.

For crypto practitioners, RWA tokenization offers a dual frontier: yield-enhancing assets with on-chain composability, and protocol/infrastructure opportunities underpinning the market. But success will depend not just on token design, but on legal structures, market microstructure, and cross-jurisdiction coordination.