Key Takeaways :

- The U.S. CFTC has launched a public‐comment initiative exploring the use of tokenized collateral (including stablecoins) in derivatives markets.

- This is not yet binding regulation, but a step in a larger “crypto sprint” to modernize capital markets.

- Industry heavyweights (Circle, Coinbase, Ripple, Tether) broadly support the initiative, seeing it as a way to improve capital efficiency, liquidity, and settlement speed.

- Challenges remain around valuation, custody, risk management, and regulatory guardrails.

- The outcome of public feedback (due October 20, 2025) will shape next steps, including possible pilot programs.

- This move aligns with broader trends: tokenized treasuries, institutional adoption of tokenized collateral, and updates to derivatives frameworks (e.g. by ISDA).

- For crypto/DeFi practitioners, the initiative hints at new opportunities in tokenization, stablecoin-backed products, and interoperability between traditional and blockchain finance.

Background and Context

On September 23, 2025, the U.S. Commodity Futures Trading Commission (CFTC) announced that it is launching an initiative to explore the use of tokenized collateral—including stablecoins—as eligible collateral in derivatives markets. This enterprise is part of a larger regulatory push dubbed the “crypto sprint,” aimed at aligning U.S. regulatory frameworks with blockchain innovation.

Acting Chairman Caroline Pham emphasized that collateral management is the “killer app” for stablecoins—i.e. a high-impact use case in markets. The CFTC’s initiative builds upon prior deliberations, including the CFTC’s Crypto CEO Forum (February 2025) and recommendations from its Global Markets Advisory Committee’s Digital Asset Markets Subcommittee.

Importantly, this is not yet binding regulation. Rather, the CFTC is soliciting public input (due by October 20, 2025) on technical options, guardrails, and design considerations. Based on feedback, the agency may launch pilot programs or propose regulatory changes.

This proposal dovetails with the recently enacted GENIUS Act, which formally establishes rules for U.S. payment stablecoins. That law lays a foundation for stablecoins to be backed by safe assets (e.g. U.S. Treasury, cash) and mandates certain transparency and reserve standards. The CFTC initiative can be viewed as a next step in integrating stablecoin markets with core financial infrastructure.

Why This Matters

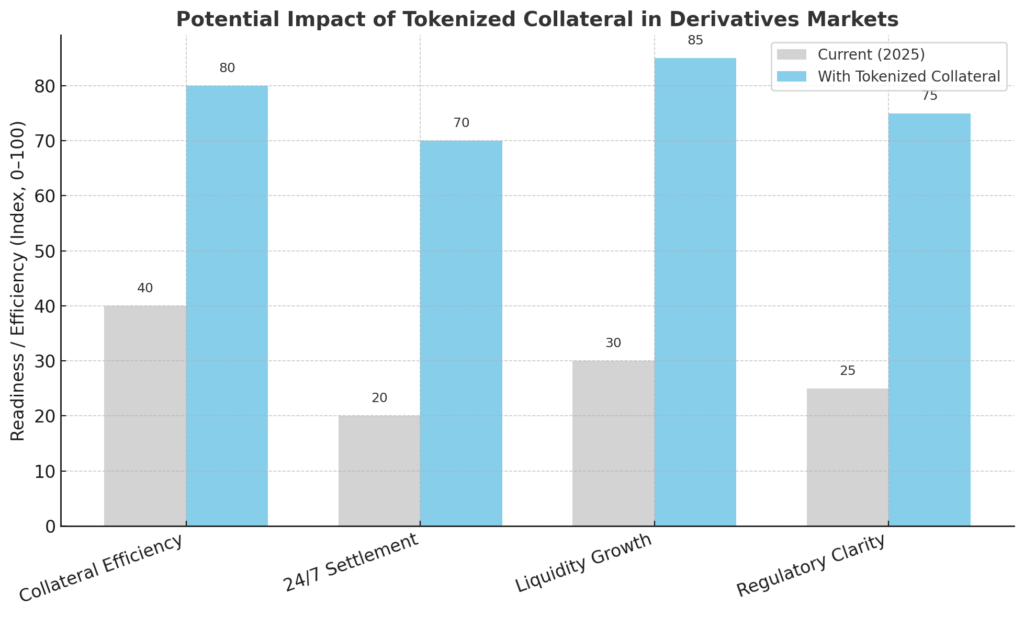

Improving Capital Efficiency and Liquidity

One of the largest frictions in derivatives markets is the need to post collateral (often in cash or Treasuries), which can be operationally burdensome, slow, and capital-inefficient. Tokenized collateral, with stablecoins or tokenized Treasuries, could enable near-instant settlement, reallocation, and more efficient capital use.

Enabling 24/7 Markets

Traditional markets follow limited trading hours and settlement windows. Tokenized collateral could permit around-the-clock operations and intraday margining that is more responsive.

Unlocking New Yield and Collateral Products

Crypto participants are already exploring tokenized treasury and money market funds as alternatives to stablecoins. According to the Financial Times, tokenized Treasury fund assets have surged ~80% in 2025 to $7.4 billion, as crypto players seek yield plus collateral utility. Such tokenized instruments may play a bigger role in collateral ecosystems.

Regulatory Alignment and Legitimacy

By inviting public comment and building regulatory guardrails, the CFTC aims to provide clarity and institutional certainty. If well-designed, this may lower barriers for institutional capital to enter digital asset systems.

Global Competitive Position

Other jurisdictions (e.g. EU, Singapore) are also exploring tokenization in capital markets. The U.S. push may help maintain competitiveness and influence global standards.

Industry Response

Immediately after the announcement, major crypto–finance firms voiced support:

- Circle: President Heath Tarbert stated that trusted stablecoins such as USDC could be used as collateral in derivatives, lowering costs and unlocking liquidity.

- Coinbase: Greg Tusar called the move “a revolution for U.S. derivatives” and praised the recognition of stablecoins as future money.

- Ripple: Jack McDonald emphasized that clear rules on valuation, custody, and settlement are essential to bring institutions onboard.

- Tether: Paolo Ardoino noted that stablecoins already form a $300 billion global market, underscoring the significance of integrating them into derivatives markets.

While industry support is strong, some voices caution about implementation complexity: ensuring interoperability across platforms, managing cross-border risk, and reconciling volatile token values with stable obligations.

Technical & Regulatory Challenges

Valuation, Volatility, and Risk Adjustment

Determining how collateral value should be adjusted in volatile periods is nontrivial. Even so-called stablecoins have potential reserve, redemption, or peg‐stress risk. The CFTC must define how “haircuts” (discounts) or buffer reserves apply.

Custody and Security

Secure custody of tokenized collateral, segregation, prevention of double-spending or misuse, and robust auditability are essential. The infrastructure must be extremely secure.

Legal and Contractual Updates

Many derivatives contracts are governed by ISDA (International Swaps and Derivatives Association) master agreements. ISDA has already updated an annex to support tokenized collateral, but widespread adoption will require further legal, contractual, and compliance work.

Interoperability Across Platforms

Collateral tokens must operate seamlessly across clearinghouses, exchanges, wallets, and custodians. Cross-chain and cross-jurisdiction interoperability is a complex engineering and regulatory task.

Regulatory Guardrails

To protect systemic stability, the CFTC must define which stablecoins are acceptable (e.g. only those licensed under the GENIUS Act), what reserve standards must be met, governance and auditing rules, and how to monitor for misuse or contagion.

Market Fragmentation and Liquidity Gaps

Not all tokenized assets will be liquid in all market conditions. There is risk of fragmentation: collateral markets may not be deep enough during stress periods, causing valuation or settlement failures.

Recent Developments & Related Trends

- ISDA updates: As mentioned, ISDA has adapted its framework to include tokenized collateral in derivative contracts. This helps legal acceptance.

- DTCC platform: The Depository Trust & Clearing Corporation (DTCC), a major U.S. financial infrastructure provider, is building a blockchain‐based tokenized collateral management platform on its own AppChain.

- Euroclear & Digital Asset: In Europe, Euroclear launched a tokenized collateral initiative with Digital Asset, pointing to cross-market momentum.

- JPMorgan’s TCN: JPMorgan has implemented a Tokenized Collateral Network (TCN) enabling clients (e.g. BlackRock) to tokenize shares and use them as collateral in OTC trades.

- Tokenized Treasuries use: Market participants are using tokenized Treasuries for intraday margin calls because of faster settlement and liquidity.

- Tokenized fund growth: The FT reports that tokenized treasury or money market funds have seen rapid growth in 2025 (~80% increase to $7.4 billion), often used by crypto traders as collateral or yield vehicles.

- Stablecoin demand affecting yields: A working paper found that Tether’s large U.S. Treasury holdings may lower short-term yields, highlighting how stablecoin demand may influence traditional markets.

These developments suggest that, beyond regulation, the technical and market infrastructure for tokenized collateral is actively evolving, creating a more hospitable environment for this CFTC initiative.

Implications for Crypto & DeFi Practitioners

New Collateral Markets

If stablecoins or tokenized assets become accepted collateral in regulated derivatives, new markets and products may emerge: tokenized collateral swaps, lending against tokenized assets for derivatives margin, etc.

Bridging TradFi and DeFi

Participants skilled in DeFi infrastructure (smart contracts, tokenization, custody) may find opportunities to provide infrastructure, tooling, or services around collateral or settlement in hybrid TradFi + DeFi environments.

Valuation or Risk Tools Demand

As collateral markets evolve, demand will grow for sophisticated risk models, price oracles, and real-time monitoring systems to support collateralized instruments in volatile conditions.

Focus on Compliance & Certification

Projects will need to meet high standards for auditing, transparency, and regulatory compliance to be eligible as collateral providers. This raises the bar for trustworthiness and infrastructure maturity.

Strategic Token Design

Stablecoin or asset token issuers may adapt designs for collateral usage—higher liquidity, modular custody, composability, and interoperability become more competitive differentiation.

What to Watch & Next Steps

- Public Comment Consolidation

The CFTC will collect and review feedback until October 20, 2025. The quality and diversity of responses could shape the regulatory trajectory. - Pilot Programs

Based on feedback, the CFTC might authorize controlled pilot programs to test tokenized collateral in live derivatives settings. Early pilot outcomes will be critical. - Proposed Rulemaking

If pilots succeed, formal rule changes may follow, potentially amending margin rules or registration requirements. - Industry Adoption & Infrastructure Build-out

Infrastructure providers (custodians, exchanges, smart contract platforms, interoperability middleware) will need to scale and integrate. - International Coordination

Since derivatives and collateral markets are global, harmonization or coordination with other jurisdictions (EU, Asia, Singapore) will influence adoption. - Market Behavior & Liquidity Stress Tests

Real-world stress scenarios (volatile markets, liquidity crunch) will test whether tokenized collateral systems hold under strain.

Conclusion

The CFTC’s move to explore tokenized collateral—specifically leveraging stablecoins—in derivatives markets is a potentially transformative moment for both traditional finance and crypto. While still in its nascent stage, this initiative signals that regulators are taking seriously the bridging of DeFi principles with regulated market infrastructure.

For those seeking new crypto opportunities, this development suggests fertile ground: infrastructure development for collateralization, tokenization of real-world assets, risk modeling, custody solutions, and bridging protocols. But success is contingent on robust design in valuation, security, interoperability, and strong regulatory frameworks.

If executed thoughtfully—with strong safeguards and industry collaboration—tokenized collateral may usher in a new era of capital efficiency, liquidity, and composability across finance. This could meaningfully lower barriers for institutions and deepen the integration between crypto and traditional markets.