Key Takeaways:

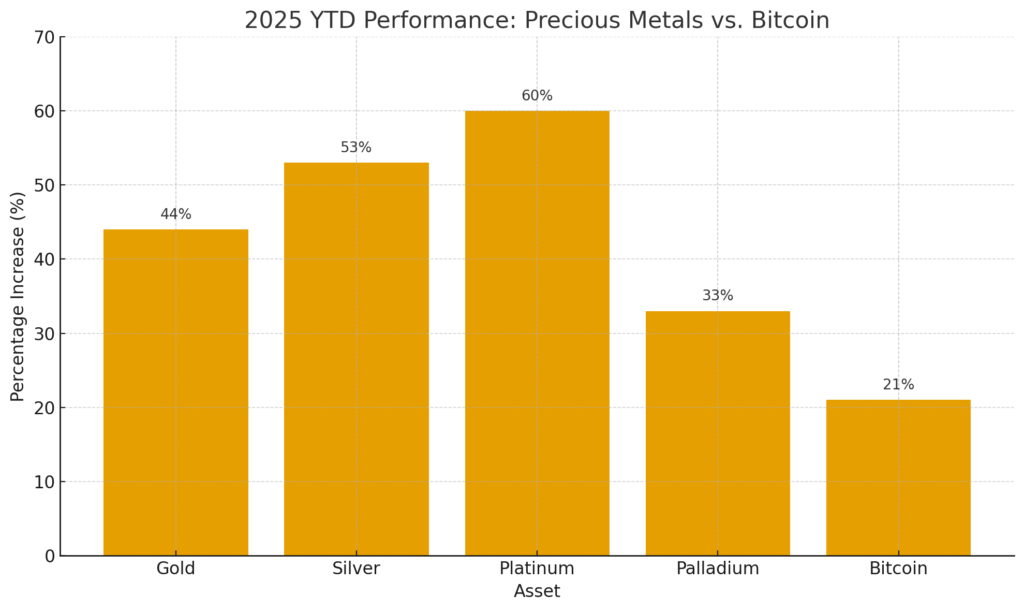

- In 2025, gold has surged ~44%, while silver, platinum, and palladium have all outpaced Bitcoin’s performance; platinum in particular has seen gains of 55–60%.

- Central banks are aggressively buying gold, elevating the entire precious metals complex; this institutional demand exerts upward pressure on prices.

- Bitcoin’s growth is being capped by older-wallet sell-offs and lack of central bank adoption; it remains largely a retail/institutional speculative asset rather than a reserve asset.

- Nevertheless, some analysts foresee that by 2030 Bitcoin may begin to co-occupy central bank balance sheets alongside gold.

- For crypto and blockchain practitioners, this context suggests that digital assets must evolve in utility and trust (e.g., tokenized real-world assets, stable collateral, central bank digital currencies) to compete with precious metals as stores of value.

1. 2025 Performance: Precious Metals Surge Ahead

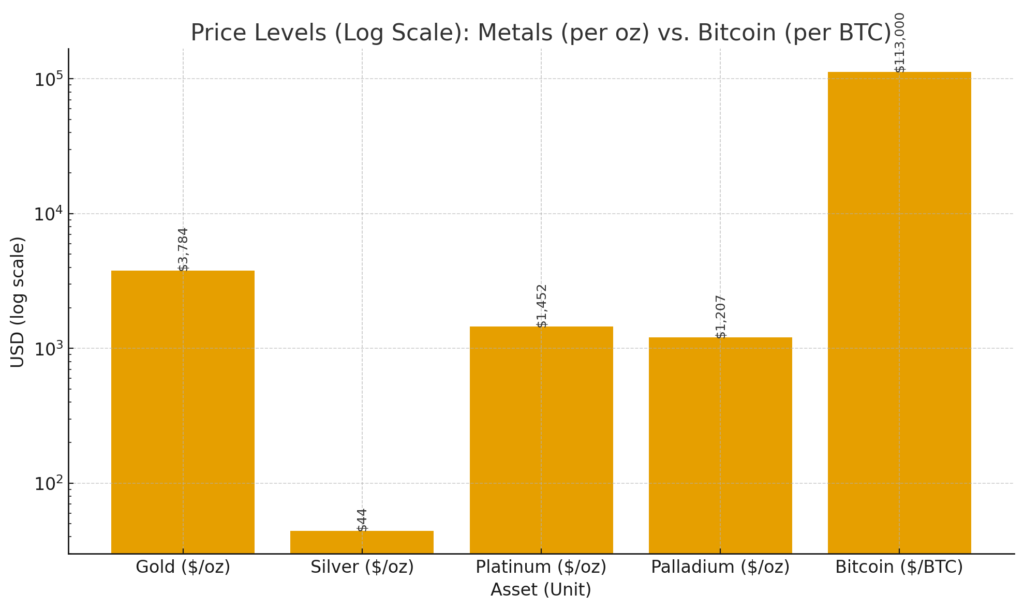

In 2025, gold has drawn widespread attention for its remarkable rally. According to TradingView data, gold has jumped approximately 44%, reaching a near all-time high of $3,784 per troy ounce. However, gold is not alone in this rally. Silver has gained about 53% to $44.32 per troy ounce, and platinum has seen meteoric growth—rising ~60% to $1,452. Palladium has also climbed ~33%, settling near $1,207.

In fact, recent reports imply that platinum is now leading the precious metals pack; one article notes a 57% surge year-to-date, outperforming both gold and silver. These returns significantly outpace Bitcoin’s gains in the same period, which have been modest by comparison—Bitcoin has risen just above 20%, reaching around $113,000.

This divergence suggests that in volatile times, capital is gravitating toward hard, physical assets rather than digital ones—at least for now.

2. Why Precious Metals Are Winning (for now)

2.1 Central Bank Buying: The Ultimate Institutional Endorsement

A major driver behind the gold rally (and by extension silver and platinum) is the aggressive purchasing activity by central banks. Global central bank gold reserves today total about 36,000 metric tons, according to an ECB-backed study. Over the past three years, central banks have added more than 1,000 tons annually—more than double the long-term average.

Furthermore, a 2025 survey by the World Gold Council (WGC) found that 76% of central banks expect to increase their gold holdings over the next five years, and nearly three-quarters plan to reduce dollar-denominated reserves. Deutsche Bank has also responded to these trends by raising its 2026 gold forecast to $4,000 per ounce, citing strong central bank demand, a weaker U.S. dollar, and the potential for renewed Federal Reserve easing.

This institutional demand provides both credibility and an anchor of supply-side support to the precious metals markets.

2.2 Sentiment, Inflation, and Safe-Haven Demand

Global macro conditions reinforce this flow into metals: concerns about U.S. fiscal deficits, rising inflation, political risk, and challenges to central bank independence create an environment where investors seek refuge in tangible assets.

Saxo Bank notes that in September 2025, gold touched $3,800, silver hit a 14-year high around $44.46, and platinum climbed above $1,500, its strongest level in over a decade. Part of this momentum is due to declining U.S. funding costs and fragile risk sentiment in equities.

These tailwinds have improved the risk/reward calculus of precious metals relative to digital assets in the eyes of many institutional and retail investors.

2.3 Industrial Demand & Relative Valuation (for Silver and Platinum)

While gold often plays a monetary role, silver and platinum carry strong industrial demand fundamentals. Silver is used in electronics, solar panels, and various industrial applications, giving it a dual role as both a precious metal and industrial commodity.

Platinum (and to a lesser extent palladium) has applications in automotive catalytic converters, medical devices, and certain industrial processes. Some analysts now view platinum as undervalued relative to gold; the gold/platinum ratio has drawn attention as it narrows, suggesting capital rotation into platinum.

Additionally, supply constraints may aid platinum. Reports from WPIC forecast that from 2025 to 2029, platinum could experience annual average supply deficits—supporting further price appreciation.

Thus, silver and platinum offer a more compelling narrative in 2025: upside potential anchored by industrial demand, valuation divergence, and supply dynamics.

3. Bitcoin’s Underperformance: Causes and Implications

3.1 Lack of Reserve Asset Status

Despite being portrayed as “digital gold,” Bitcoin has not yet secured a role in central bank reserves. Without that institutional backing, it lacks the same stability of demand and institutional safety net as physical metals.

Even as institutions invest in Bitcoin (e.g., through ETFs), these flows are subject to volatility, redemptions, and regulatory uncertainty—unlike central bank purchases of gold, which tend to be strategic and long-term.

3.2 Old-Wallet Sell-Offs & Distribution

Another drag on Bitcoin’s rally has been the distribution of holdings from older wallets. As Bitcoin surpasses thresholds like $110,000, some long-term holders or early adopters are liquidating, which can offset the inflows from new buyers and dampen price gains.

These outflows—or at least the perception of them—create resistance zones and may limit sustained upside momentum, especially when markets are fragile.

3.3 Volatility, Regulatory Risk, and Maturity

Bitcoin remains subject to sharp swings—daily moves of >10% happen frequently. Regulatory developments or macro shifts (e.g., interest rates, capital flows, taxation) can provoke abrupt sentiment reversals.

Moreover, while Bitcoin’s adoption is maturing, its infrastructure, counterparty risk, and perception as a speculative asset rather than a safe haven still limit its appeal for large institutional allocations (beyond hedge, VC, or wealth-diversification exposures).

4. Outlook: Coexistence or Competition?

4.1 Can Bitcoin Join Central Bank Reserves?

Some financial institutions are projecting that Bitcoin may eventually cohabit central bank balance sheets alongside gold. For example, Deutsche Bank research suggests that by 2030, Bitcoin could ascend into reserve-likeness.

That said, such a shift would require breakthroughs in trust, regulation, custody, and macro policy acceptance. Without these, Bitcoin may remain in a parallel but distinct asset class.

4.2 Hybrid Portfolios: Precious Metals + Digital Assets

For risk-aware investors interested in both security and upside, combining physical precious metals (gold, silver, platinum) with select digital assets may offer balance. Metals anchor stability and diversifying safe-haven exposure, while crypto can capture upside from innovation and adoption cycles.

From a blockchain practitioner’s perspective, this push underscores the need for real-world utility, on-chain trust, and interop with traditional finance. Tokenized gold, commodity-backed tokens, central bank digital currencies (CBDCs), or decentralized collateralization models might be the next frontier to compete.

4.3 Watch for Rotation and Sentiment Shifts

Markets are dynamic. If inflation subsides, central banks pivot, or investor sentiment swings back toward risk assets, a rotation from metals into equities and crypto is possible. Bitcoin’s volatility affords high reward potential—but also high downside risk.

Thus, keeping a close eye on macroeconomic signals (interest rates, bond yields, central bank policies) as well as adoption metrics (custody, ETF flows, institutional allocations) will be key for timing and allocation decisions.

5. Implications for Crypto / Blockchain Practitioners

- Don’t chase Bitcoin as a pure store-of-value asset — until digital assets achieve more institutional trust and reserve status, they are likely better positioned as high-growth, higher-risk components rather than core hedges.

- Focus on composability with real assets — protocols that enable tokenized gold, silver, and platinum exposures could gain traction by bridging the digital and physical worlds.

- Emphasize credibility and custody solutions — secure custody, audited reserves, transparency, regulatory compliance—all will matter if blockchain assets are to compete with traditional safe havens.

- Monitor central bank and institutional trends — if central banks ever begin holding crypto assets, that could change the game fundamentally.

- Adopt humility in cycles — precious metals’ outperformance in 2025 is a reminder that markets rotate, and sometimes fundamentals (scarcity, institutional demand, macro stability) can overturn narratives.

Conclusion

In 2025, the standout narrative is that precious metals are outperforming Bitcoin—often by a wide margin. Gold has soared ~44%, silver ~53%, and platinum an astonishing ~55–60%, while Bitcoin’s gains have been more modest in the ~20% range.

This divergence underscores several structural truths: central banks currently favor physical assets; Bitcoin has not yet earned deep institutional reserve status; and markets are rediscovering the allure of tangible scarcity and non-counterparty value.

That said, this environment is not an indictment of crypto or blockchain, but a wake-up call: digital assets must evolve beyond speculation and build credible infrastructure, trust, and real-world utility if they hope to compete with gold’s decades- or centuries-old narrative.

For investors and technologists alike, the opportunity lies not in choosing metals or crypto exclusively, but in designing hybrid portfolios and protocols that harness the strengths of both.