Key Points :

- Week 38 is historically the third-worst performing week for Bitcoin, with average return of about −2.25%.

- Indicators such as funding rates, implied volatility, and derivatives sentiment show cooling speculative dynamics.

- Despite the weak week, monthly and quarterly trends for Bitcoin remain positive.

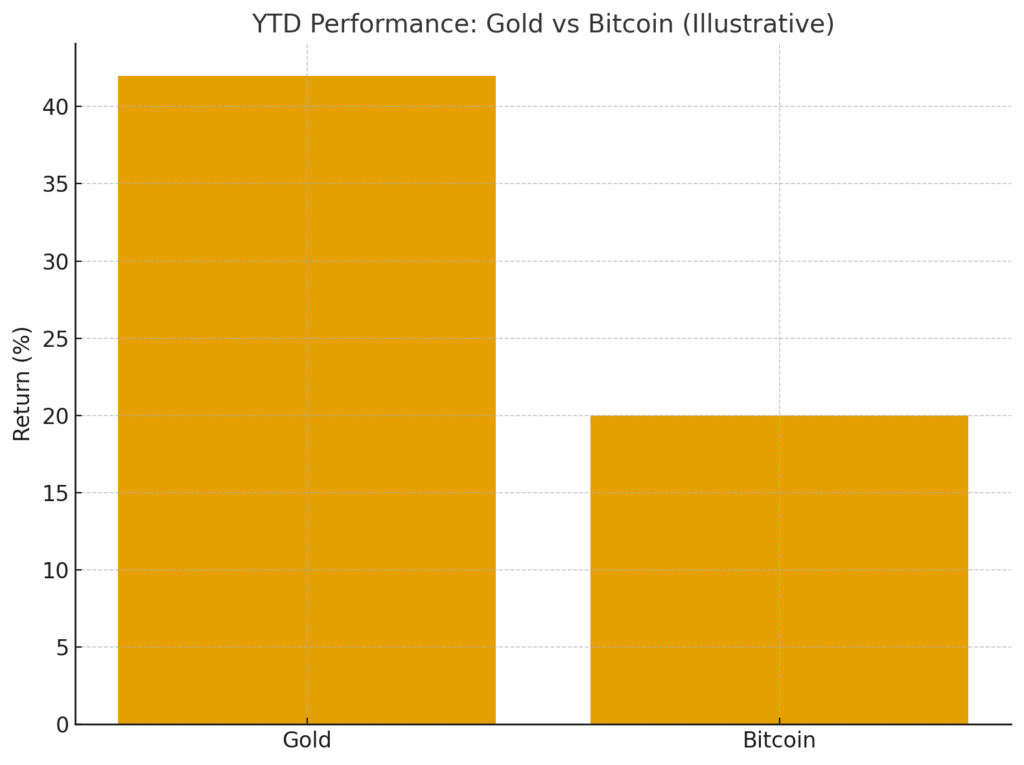

- Gold continues to outperform crypto, rising over 42% year‐to‐date, drawing some capital away.

- AI‐related stocks and tokens are gaining investor attention, possibly at Bitcoin’s expense.

- Seasonality suggests September tends to be weak for Bitcoin, but historically Q4 (especially October) offers strong returns.

1. Seasonal Weakness Hits Bitcoin Again

Historically, Week 38 of the year has been especially poor for Bitcoin, and this year has proven no exception. Data from Coinglass shows that Bitcoin’s average return during Week 38 is about −2.25%, making it the third‐worst week on record, surpassed only by Weeks 14 (−3.91%) and 28 (−2.78%) in past years.

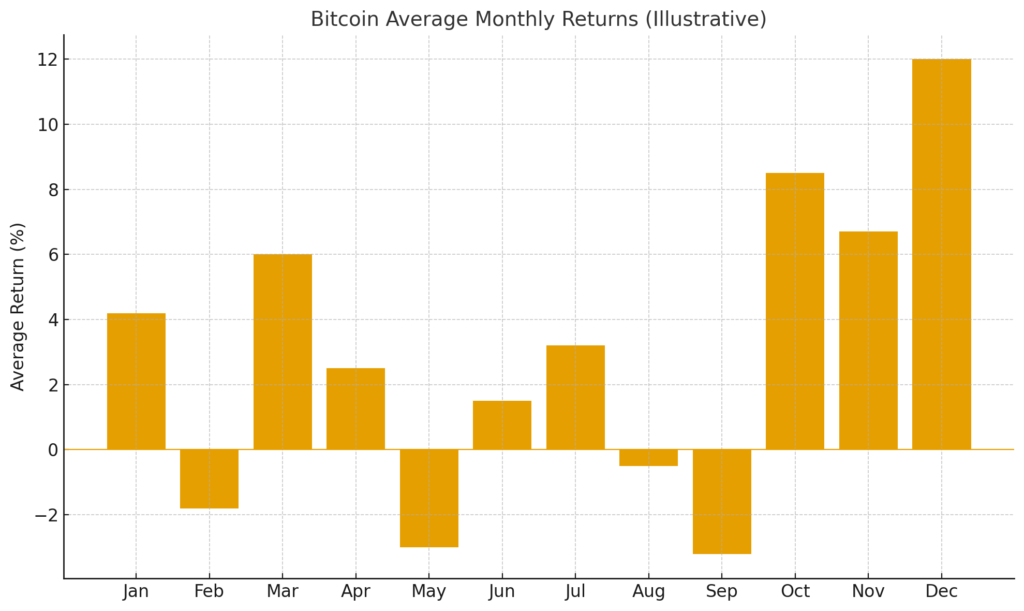

This seasonal trend is reinforced by broader patterns in September. Over the past decade, September has often been one of Bitcoin’s weakest months (average loss ~3.2%), while October tends to flip sentiment and deliver strong gains. Q4 generally has been Bitcoin’s best quarter historically.

Thus, what we observe now may be part of a recurring cycle more than a deviation—September’s weakness followed by potential strength in Q4.

2. Price Action and Max Pain Signals

Bitcoin is trading in the range of approximately US$113,000 around Week 38.

One technical/derivative market signal drawing attention is the “max pain” level in the options market. According to Deribit, the monthly options expiry for September suggests the max pain level (i.e. strike price where most options expire worthless) is around US$110,000. This can be interpreted as showing potential downside risk if market participants lean toward that level.

3. Cooling Speculative Heat: Funding Rates & Volatility

Multiple metrics indicate that speculative fervor in the Bitcoin market is easing:

- Perpetual futures funding rates have dropped to around annualized 4%, which is among the lowest in a month. This suggests less demand to hold leveraged long positions.

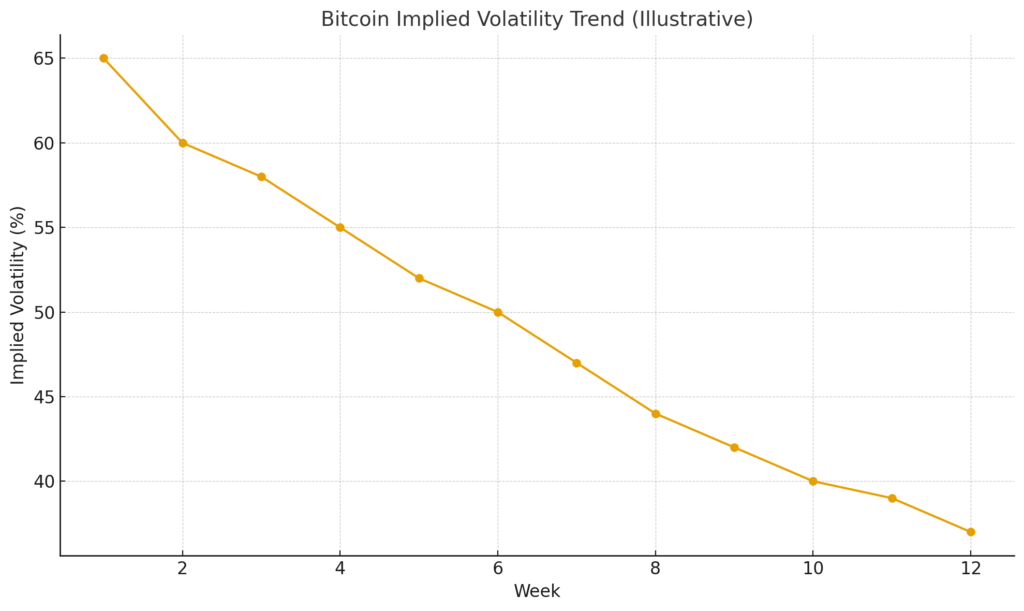

- Implied volatility (IV) is also low—around ~37‐38% annualized in various measures. Historically, when IV drops this far, markets may be underestimating future swings.

- Derivatives indicators show a decline in hedging demand and a more complacent tone among options traders.

These suggest that while Bitcoin has fallen this week, the market is not in panic—but rather in cautious observation, possibly awaiting trigger events.

4. Broader Trends: Monthly, Quarterly, Year‐to‐Date

Despite the weak week, Bitcoin is still:

- Up about 4% in September so far.

- Up about 6% in the current quarter.

Year to date, after a strong run earlier, Bitcoin has gained considerably. Some reporting mentions >20% gains by mid‐2025.

This suggests that the recent drop is more of a pullback rather than a reversal of the longer‐term trend—assuming no major external shock emerges.

5. Gold Outperformance & Alternative Assets

Gold remains a strong performer in comparison to Bitcoin and other cryptos:

- Gold has gained more than 42% year‐to‐date, extending its outperformance over crypto markets.

- Investors traditionally treat gold as a safe haven; its recent run may be pulling some capital that might otherwise go into speculative crypto positions.

Other alternative sectors gaining attention include AI and high‐performance computing stocks. Their strong performance may be drawing interest (and capital) away from crypto in certain investor segments.

6. AI & Crypto: Competition, Convergence, and Investor Focus

AI’s rise in the public markets and in crypto is a key trend relevant to those scouting the next investment frontier.

- Grayscale recently introduced a new Artificial Intelligence Crypto Sector, comprising ~20 tokens, with combined market capitalization ~US$20‐21 billion. This includes AI platforms, tools/resources for AI, and AI apps and agents.

- AI‐driven trading systems (bots) are increasingly prevalent, automating trades, risk management, and portfolio allocation. They are increasingly used to manage both stocks and crypto exposure.

- Part of the investor shift appears to be thematic: AI has become a major narrative similar to “tech” or “growth,” and is absorbing interest in terms of capital, media attention, and speculative demand.

This dynamic both competes with crypto for risk capital and suggests crypto projects with strong AI or compute relevance may have extra tailwinds.

7. Derivatives & On‐Chain Signals: Mixed but Important

Looking inside derivatives markets and on‐chain metrics gives more nuanced signals:

- Open interest in futures has increased in some periods, but funding rates suggest that long leverage is not as hot as before.

- The options skew is becoming less aggressive in some cases, indicating reduced demand for hedging or protection.

- On‐chain metrics like transfer volumes are rising, suggesting renewed flow of capital, even though user activity (number of active addresses) and fees are softer.

These mixed signals point to a market in transition: some buying/investment interest remains, especially institutional (e.g. ETF flows), but speculative excess appears reduced.

8. Recent Developments to Watch

To give the full picture, here are recent developments (outside of the original article) that shed light on where things may be headed:

- Implied volatility for Bitcoin in 30‐day options (e.g. via indices like Volmex BVIV) has dropped to ~38%, approaching multi‐month or multi‐year lows.

- The seasonal pattern (weak September, strong Oct‐Dec) holds up in current analysis.

- AI‐infrastructure companies are raising large capital (e.g. Nvidia’s partnerships, data center projects) and drawing attention from investors seeking growth outside crypto.

- Regulatory, macroeconomic, and rate expectations (e.g. expectations for Fed rate cuts or interest rate policy) are influencing Bitcoin’s outlook as well.

Conclusion: What This Means for Investors Seeking New Crypto Opportunities

Bitcoin’s drop in Week 38, while notable, is not anomalous given its seasonal history. The contraction in volatility and falling speculative metrics suggest a market that’s cooling off, but not collapsing. Positive returns in September and the quarter so far reinforce that the medium‐term trend remains favorable, with possible upside ahead—especially as we move into Q4, which has historically rewarded holders.

For investors looking for crypto assets beyond Bitcoin (or earlier entry points), a few strategic implications:

- Monitor assets in the newly formed AI Crypto Sector, especially those with strong utility in compute, data infrastructure, or tools for AI. These could benefit both from AI narrative tailwinds and crypto upside.

- Watch derivative signals (volatility, skew, funding rates) to gauge when market sentiment might shift from caution to re‐acceleration.

- Keep gold or stable, yield‐producing assets in view as hedges—especially for periods of low confidence or external risk.

- Be mindful of macro factors: interest rates, regulation, global economic uncertainty all continue to feed into crypto risk premium.

In sum, Bitcoin’s recent decline may feel uncomfortable, but for those with an eye for cycles and alternatives, it could present opportunity—not just risk.