Main Points:

- Chinese securities regulator (CSRC) has asked certain brokerages to halt real‐world asset (RWA) tokenization in Hong Kong, particularly offshore ventures.

- The move reflects Beijing’s growing concern about risk management, legitimacy of underlying claims, and offshore financial stability.

- Hong Kong continues to push ahead: legal reviews, stablecoin licensing, and pilots of tokenized products are expanding.

- Global RWA tokenization market is growing rapidly, but liquidity, regulatory clarity, and cross‐jurisdictional alignment remain major challenges.

1. What China Did

China’s Securities Regulatory Commission (CSRC) has informally instructed at least two major mainland brokerages to suspend their real‐world asset tokenization operations in Hong Kong. The guidance is not a formal rule or ban but signals a tightening stance. The goal seems to be ensuring better risk controls and verifying that claims made by firms trading or tokenizing assets are backed by strong and legitimate underlying asset business.

Hong Kong has seen a surge of interest in tokenizing RWAs in recent months: companies converting stocks, bonds, funds, real estate into blockchain‐based tokens. Some specific examples: GF Securities launched “GF Tokens” in June, backed by USD, HKD, offshore RMB. China Merchant Bank International (CMBI) helped raise ~¥500 million (≈ US$70.3 million) via a tokenized digital bond.

2. Why Beijing Is Concerned

a) Financial stability & risk exposure

The mainland is cautious about financial instability arising from tokenization, especially when tokenized assets are “offshore” or involve cross‐border settlement or less transparent underlying assets. There is concern that tokenized assets could mask property or credit risk in the mainland by shifting exposure.

b) Regulatory gaps and policy alignment

Because tokenization is relatively new, many jurisdictions—including mainland China—lack a coherent regulatory framework for tokenized assets. This includes rules around securities classification, disclosure, custody, and valuation. The pause gives time to align policies, definitions, and oversight.

c) Cross‐border control, investor protection

Mainland authorities are wary of products being marketed or sold offshore under looser rules. They want to ensure investor rights, that tokenization doesn’t circumvent capital controls, and that stablecoins or similar vehicles aren’t exploited in unregulated contexts.

3. Hong Kong’s Response and Momentum

Despite the CSRC’s guidance, Hong Kong is pushing ahead with building a robust framework for digital assets and tokenization:

- Legal reviews are underway: The Financial Services and the Treasury Bureau (FSTB) and the Hong Kong Monetary Authority (HKMA) have initiated reviews of tokenization, especially focusing initially on bond markets.

- Stablecoin licensing regime: By August 31, there were 77 firms interested in applying for stablecoin licenses under the emerging regime.

- Pilot tokenized products already live: Digital bonds, yield‐linked tokens, and RWA‐based products are being introduced by GF Securities, CMBI, Seazen Group, among others.

4. Broader RWA Tokenization Trends

While the China/Hong Kong story is recent, it fits into larger global trends in RWA tokenization. Some of these are:

- Market size and projections: Estimates vary, but the global RWA tokenization market is currently tens of billions of dollars, with projections climbing to $15–$30+ trillion by 2030 or early 2030s depending on assumptions.

- Institutional adoption: More traditional finance institutions, asset managers, and developers are entering the space. Tokenization of assets like real estate, private credit, treasuries, etc., is becoming more common.

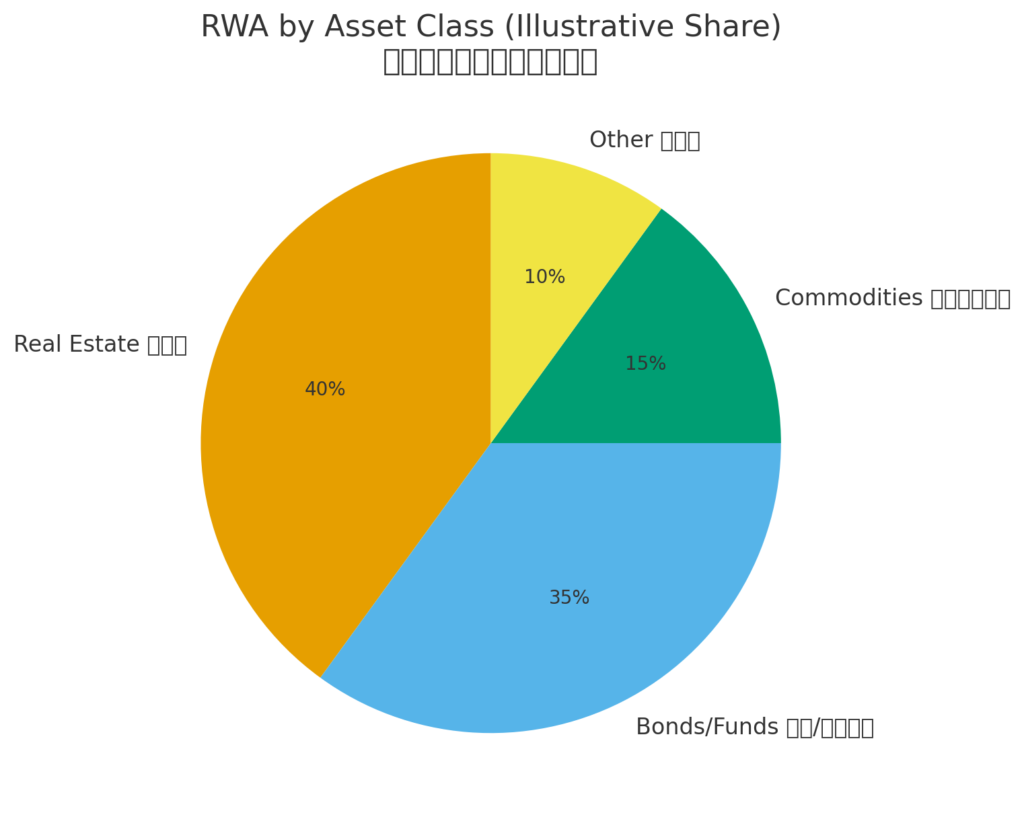

- Use cases & asset classes: Tokenization of bonds, funds, real estate, commodities, etc., are most mature. Newer ideas: intellectual property, carbon credits, fine art, etc., but with higher legal/valuation complexity.

- Challenges: Key issues are liquidity (many tokens have low trading volumes, weak secondary markets), regulatory uncertainty, valuation transparency, custody solutions, cross-jurisdictional legal ambiguities.

5. Implications for Investors & Builders Seeking New Crypto / Revenue Sources

For those interested in new crypto assets, revenue streams, or practical blockchain applications, the China‐Hong Kong pause and global trends suggest several lessons:

- Projects or tokens that rely on ambiguity in regulation or weak risk controls are at risk of regulatory pushback—especially from jurisdictions like China.

- Lower‐risk RWAs (e.g., tokenized money-market instruments, short‐term government bonds, real estate with transparent ownership) are more likely to be tolerated and perhaps beneficial.

- Investor protection will matter: disclosures, legal ownership, custody, on/off ramps, audits will be differentiators.

- Interoperability, transparent valuation, and liquidity will be key: even if tokenized, without active secondary markets or clear rules, the value may remain constrained.

- Strategic localisation: depending on where the assets are, which laws apply, who the investors are. Regulatory jurisdictions matter.

6. Recent Developments & Case Studies

- Seazen Group (Chinese property developer) announced an institute in Hong Kong to explore RWA tokenization (intellectual property, revenue streams) and possibly issuing NFT products tied to properties.

- Stablecoin interest: the stablecoin licensing process in Hong Kong has attracted dozens of applicants. Stablecoins are likely to serve as infrastructure for transactions and settlement in tokenized asset frameworks.

- Global regulatory movement: In the U.S., Europe, and Asia, regulatory bodies are trying to clarify how tokenized assets—especially those qualifying as securities—will be treated. Frameworks like MiCA in EU, discussions in U.S. Senate/SEC, etc.

Graph / Figure Suggestion

- Current estimated global RWA tokenization market size (e.g. ~$24-$30B) vs projected size in 2030 (e.g. $15-30T)

- Breakdown by asset classes (real estate, bonds/funds, commodities, others) showing % share.

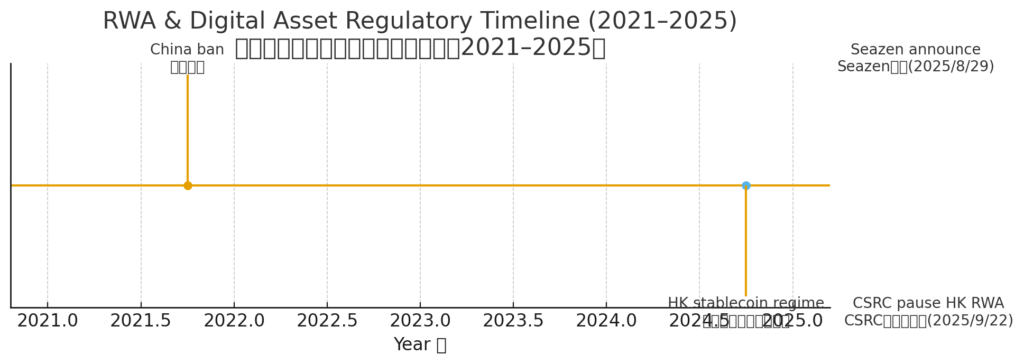

Also possibly a timeline chart showing (2021 → 2025) regulation pushbacks, tokenization pilot launches, and major events (e.g., China crypto ban 2021, Hong Kong stablecoin regime, Seazen announcement, CSRC guidance etc.).

7. What This Means Going Forward

- The pause by CSRC isn’t likely permanent ban, but more of a moment to ensure frameworks catch up. Hong Kong may remain a key node if it can align legal, operational, and policy standards with mainland expectations.

- Regulatory risk is high in cross-border RWA tokenization. Any builder or investor must pay attention to both the domestic regulators and foreign ones (especially China, in this case).

- Liquidity is the bottleneck—scaling secondary markets, enabling interoperable standards, and clearing legal/custodial hurdles will become competitive advantage.

- There is opportunity for “compliance oriented” platforms, bridge builders, legal tech, data/valuation providers in the RWA ecosystem: services that reduce risk and increase trust will likely be profitable.

Conclusion

The CSRC’s instruction to certain mainland brokerages to halt RWA tokenization in Hong Kong marks a cautionary turning point. While Hong Kong continues to accelerate its digital finance agenda, Beijing is signaling that oversight, legitimacy, and systemic risk cannot be overlooked. For crypto asset seekers and blockchain practitioners, the path to revenue and innovation in RWA is still open—but it will favor projects with legal clarity, transparency, lower risk, and strong infrastructure. The pause may not mean “stop forever,” but it’s a reminder that in finance, especially when transforming real world assets into digital tokens, regulatory alignment often makes or breaks value.