Main Points :

- Regulatory clarity, especially from the U.S. GENIUS Act, is driving corporate adoption of stablecoins.

- As of mid-2025, about 13% of firms are already using stablecoins; 54% of non-users plan to within 6-12 months.

- For users, cost savings in cross-border payments are substantial: 41% report at least 10% cost reduction.

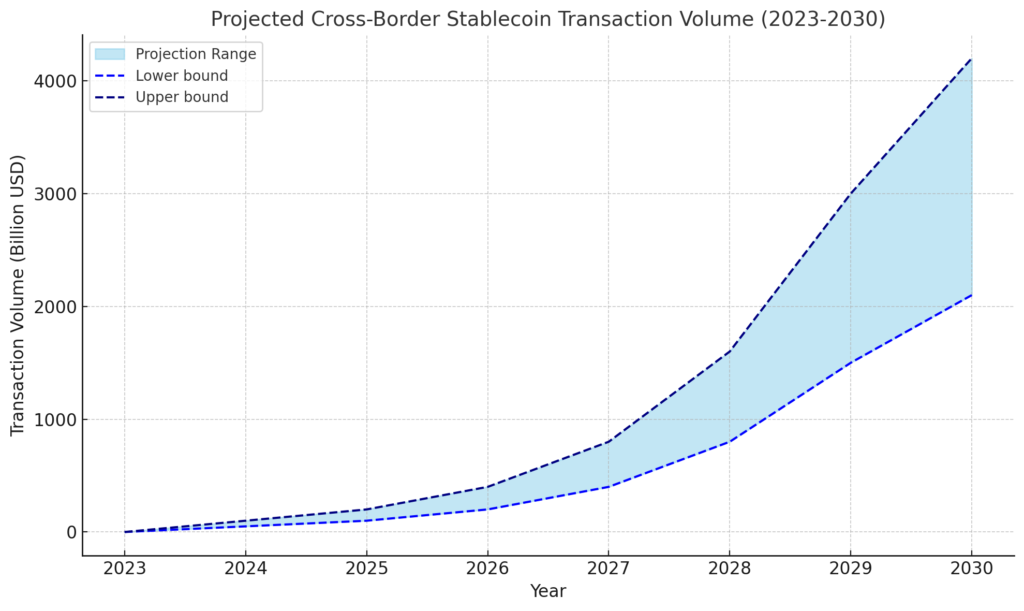

- By 2030, stablecoins are projected to account for 5-10% of all cross-border payments, representing $2.1-$4.2 trillion in value.

- Major hurdles persist: only 8% of businesses currently accept stablecoin payments; many firms rely on banks or fintechs for integration.

- Globally, regulation and infrastructure remain key in determining where adoption proceeds fastest, with regions like Latin America, Asia, and Europe each having distinct challenges and opportunities.

1. Regulatory Turning Point: The GENIUS Act and Global Frameworks

In July 2025, the U.S. passed the GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins Act), which for the first time puts a federal framework around “payment stablecoins.” Key features include oversight of stablecoin issuers, requirements for reserve backing, and constraints on who may issue stablecoins in the U.S.

This regulatory clarity is cited by many corporate executives as a primary driver for adoption. It alleviates ambiguity around how reserves should be handled, which institutions will be regulated, and reduces risks around taxation, custody, and compliance. Meanwhile, other jurisdictions are also advancing regulation: the European Union via MiCAR (Markets in Crypto-Assets), and other countries exploring stablecoin-oriented laws.

2. Current Adoption: Who’s Using, Who’s Planning

According to the EY-Parthenon survey of about 350 executives (corporates and financial institutions) in June 2025:

- 13% already use stablecoins, especially for cross-border payments.

- Among non-users, 54% expect to adopt stablecoins within the next 6-12 months.

- Among current users, 62% use stablecoins to pay suppliers across borders; 53% accept cross-border payments from business partners.

Thus, adoption is no longer merely speculative: many firms are moving from interest into actual implementation. But uptake in “receiving stablecoin payments from customers / merchants” remains low.

3. Cost, Speed, and Other Business Drivers

One of the strongest motivators for stablecoin adoption is cost savings: 41% of respondents who are using stablecoins report at least a 10% reduction in international transaction costs.

Other drivers include:

- Faster settlement times vs legacy correspondent banking or SWIFT-based payments.

- Improved liquidity and reduced friction in cross-border flows.

- Being able to manage treasury, supplier payments, and B2B relationships more efficiently.

4. Forecasted Growth: Scale by 2030

EY estimates that by 2030 stablecoins could represent 5-10% of all cross-border payments globally. That share corresponds to $2.1 to $4.2 trillion in transaction volume.

This forecast assumes continued regulatory progress, improved infrastructure, and increasing adoption among both senders and receivers of cross-border payments. If these conditions are met, stablecoins may transform a significant portion of international business payments, remittances, and corporate finance flows.

5. Barriers & Infrastructure Challenges

However, several challenges remain:

- Only 8% of businesses currently accept stablecoins as a payment method. This low “receiving side” adoption limits utility.

- Many firms depend on banks or fintech intermediaries for integration. Direct acceptance or internal infrastructure is less common.

- Security risks: smart contract vulnerabilities, custody risks, reserve transparency. Institutional users are concerned about these and demand robust oversight.

- Regulatory variation between jurisdictions: rules in the EU, U.S., Asia, Latin America differ in important ways, which leads to complexities for firms operating cross-border.

6. Regional Trends & Other Recent Moves

Beyond the EY survey’s global perspective, several regional and sectoral developments are worth noting:

- Europe / EU: Under MiCAR, stablecoins and crypto-asset service providers are regulated with standards for transparency and consumer protection. But debates about “multi-issuance” stablecoins (tokens issued in multiple jurisdictions by branches of the same issuer) are generating concern, especially regarding risks of reserve mismatch or redemption obligations.

- Canada: The Bank of Canada is urging coordination among federal and provincial authorities to regulate stablecoins and improve digital payment systems, pointing out domestic fragmentation as a problem.

- Bahrain and Middle East: Bahrain has introduced a new stablecoin law, broadening regulations for issuance and offering of stablecoins tied to fiat currencies. This signals the Gulf’s intention to be a hub for regulated digital finance.

These regional moves reinforce the idea that stablecoin adoption is being shaped not just by market demand, but by how well regulators craft rules and build infrastructure.

Graph / Figure

I recommend inserting a bar chart or line graph at this point, showing projected stablecoin cross-border transaction volume from 2023 → 2030, with a $2.1-4.2 trillion band shaded for 2030. This helps visualize growth.

Conclusion & Implications

In summary, the passage of the GENIUS Act in the U.S. has been a catalyst for stablecoin adoption, by reducing regulatory uncertainty and providing a framework for issuers, reserves, and oversight. Corporates and financial institutions are responding: while only a small percentage already use stablecoins, a majority intend to adopt within the next year.

The forecast is ambitious: stablecoins controlling 5-10% of cross-border payments by 2030 implies a revolution in international finance—different payment rails, reduced costs, faster settlements. But realizing that potential depends on overcoming infrastructure-level friction (businesses accepting stablecoins, integrating systems), ensuring strong security and reserve transparency, and harmonizing regulation across borders.

For someone seeking new crypto assets or revenue opportunities, the key areas to watch are:

- Stablecoin issuers with solid reserve backing and regulator compliance.

- Infrastructure providers (wallets, custody, rails) that facilitate accepting stablecoins.

- Regions where regulation is becoming friendlier, opening opportunities for earlier movers.

- Use cases beyond just remittances or supplier payments—e.g. treasury management, trade finance, programmable payments.

Overall, stablecoins are shifting from fringe crypto utilities toward core components of global payments infrastructure. Whether or not they reach the top end of projections, they are likely to play far more than a marginal role in the next 5 years.