Main Points :

- In Bolivia, major automakers — Toyota, BYD, Yamaha — now accept USDT (Tether) for vehicle purchases, reflecting real-world payment adoption.

- Bolivia has removed a 4-year cryptocurrency ban; crypto trading and USDT usage have surged, driven by inflation, foreign exchange scarcity, and currency distrust.

- Bolivian banks (e.g. Banco Bisa) now offer USDT custodial services, enabling purchase, storage, and transfers under regulation.

- Globally, USDT and other stablecoins are growing as instruments of value preservation, cross-border remittance, and payments, especially in emerging markets.

- In the U.S., the newly enacted GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act) establishes the first federal regulatory framework for payment stablecoins: reserve requirements, licensing, transparency, definitions of who can issue, etc.

- The stablecoin market, especially USDT, has massive transaction volume and growing nominal supply; projections indicate further expansion worldwide.

Tether’s Role in Bolivia: Real-World Payments & Economic Pressures

In mid-2025, Tether’s CEO Paolo Ardoino disclosed that Toyota, BYD, and Yamaha dealerships in Bolivia are now accepting USDT for vehicle purchases. This marks a significant instance where stablecoins move beyond digital or speculative usage into high-value, real-asset transactions. Bolivians can essentially buy cars with “digital dollars,” bypassing local currency volatility.

Bolivia’s macroeconomic environment has strongly pushed this adoption. The local currency (boliviano) is under heavy inflation and distrust, and there is a severe shortage of U.S. dollars. Under these conditions, citizens and businesses seek stable stores of value and payment options. Stablecoins like USDT offer a hedge.

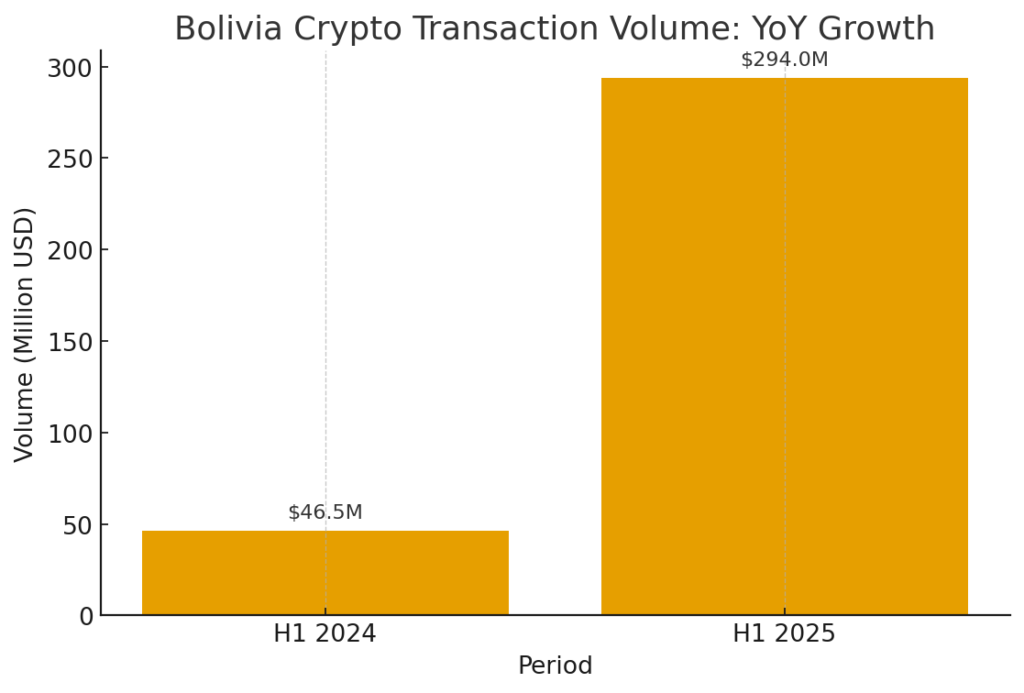

Regulatory shifts have enabled this change. After roughly four years during which cryptocurrency was largely banned (ban lifted in June 2024), Bolivia’s law environment has relaxed. The central bank acknowledges rapid growth in crypto transaction volume: in H1 2025, domestic crypto transactions reached about $294 million (≈ Bolivian crypto transactions), up from much lower figures a year prior.

Financial institutions are also participating: Banco Bisa began offering custodial services for USDT in October 2024, enabling users to buy, hold, and transfer USDT safely via regulated banking channels.

Global Stablecoin Trends: Usage, Growth, and Challenges

Beyond Bolivia, USDT remains dominant among stablecoins, especially in emerging markets. In Asia, Latin America, Africa, many users treat USDT (and USDC to lesser extent) as a de facto surrogate for the U.S. dollar—used for remittances, savings, and commerce where local currencies are volatile.

Chainalysis data shows stablecoin transaction volumes enormous: over the period June 2024 to June 2025, USDT’s monthly on-chain transaction volume exceeded $1 trillion in many months.

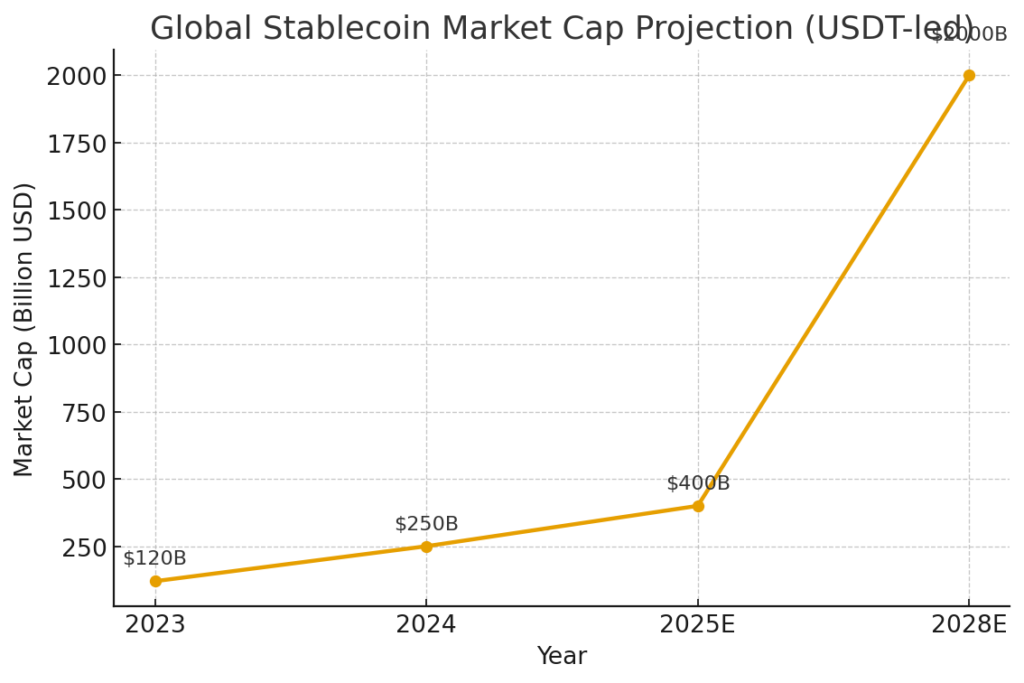

Value of stablecoins issued (market cap / supply) is also growing. Reports put total issued stablecoin value at about $250 billion mid-2025, up from ~$120 billion 18 months earlier. Forecasts suggest it could reach $400 billion by end of 2025, and even ~$2 trillion by 2028 if current trends continue.

However, rapid growth comes with risks. Economic instability drives demand, but also regulatory concerns (anti-money laundering, transparency), technical risks (custody, exchange risk), and political risks (monetary sovereignty). Some critics warn that stablecoins, if unregulated, could undermine domestic currencies, enable capital flight, or bypass banking systems.

U.S. Regulation: The GENIUS Act and Stablecoin Oversight

A major development is the passage of the GENIUS Act in the U.S. It was signed into law on July 18, 2025, after bipartisan votes in Senate and House.

Key features:

- A “payment stablecoin” is defined as a digital asset used for payment or settlement with a fixed (or predictable) value, redeemable or convertible for that fixed amount. It is not a national currency, deposit, or a security under U.S. securities laws.

- Issuers must maintain 100% reserves in highly liquid assets (USD, or short-term U.S. Treasuries), and must make monthly disclosures of reserve composition.

- Federal oversight and licensing: large issuers are federally regulated; smaller ones may be under state oversight; foreign issuers wishing to offer stablecoins in the U.S. must comply with comparable regulatory standards and register.

- Custodial and safekeeping requirements for reserves and stablecoin-related assets.

Impacts

- Provides legal clarity for stablecoin issuers, which had often operated in regulatory gray zones.

- Gives consumers and businesses better protection (transparency, reserve backing), which may increase trust.

- Makes the U.S. more competitive in attracting stablecoin innovation, because now there is a well-defined framework.

- At the same time, could lead to U.S. dollars or U.S.-denominated digital money becoming even more attractive globally, which has implications for other countries’ currencies.

Recent Developments & Additional Cases

- According to a report, Bolivia’s USDT adoption surged by ~630% YoY in 2025, especially after major automakers accepted USDT and with regulatory easing.

- Market cap of USDT was reported around $172.3 billion in recent measures, making USDT dominant (e.g. over 50-60% of the stablecoin market in certain metrics) in terms of supply or usage.

- On-chain transfer volume for USDT globally in first half of 2025 exceeded entire 2024 figures, showing acceleration.

Significance for Practitioners and New Crypto Seekers

For someone exploring new crypto assets, or seeking next revenue streams, or interested in blockchain’s practical uses, these are key takeaways:

- Real utility matters: USDT’s adoption in major purchases (cars) shows that stablecoins can serve large-ticket payments, not just micro-transactions or remittances.

- Regulation is becoming central: Unless a crypto infrastructure aligns with emerging regulatory norms (reserve backing, transparency, licensing), it may face barriers. U.S. GENIUS Act is a template.

- Emerging markets present opportunity: Markets suffering from currency instability, inflation, or limited banking access are fertile ground for stablecoin-based services: payments, transfers, price pegging, asset storage.

- Risk / legitimacy is equally important: Infrastructure around custody, regulation, exchange access, legal status will affect adoption and trust.

Summary & Outlook

USDT’s recent inroads in Bolivia – with car manufacturers accepting it, financial institutions offering custodial services, and regulatory bans lifted – constitute a case study in how stablecoins are moving from speculative assets toward being genuine tools of commerce and value preservation. Globally, USDT remains dominant among stablecoins, with transaction volumes, issuance size, and projections pointing to further expansion.

However, as this expansion accelerates, so too does the need for robust regulation, clear legal status, reserve transparency, consumer protections, and risk management. Laws like the GENIUS Act in the U.S. are critical signals that stablecoins are being treated seriously by governments — not merely as curiosities or financial engineering, but as potential pillars of modern payment systems.

For practitioners, developers, investors: paying attention to regulatory regimes, local economic conditions (inflation, currency weakness, remittance flows), and real-use case adoption (merchant acceptance, institutional custodians) is essential. The convergence of real-world need + stable, well-regulated infrastructure likely points toward stablecoins being a major growth area — both as platforms for payments and as hedge instruments in volatile economies.