Main Points :

- FCA aims to introduce full crypto regulation by 2026, focusing on risk-appropriate rules.

- Traditional banking rules will not simply be copied; a sector-specific framework will emerge.

- Key relaxations include management system requirements, cooling-off periods, and outsourcing rules.

- Stronger cybersecurity obligations and clearer consumer protections will be enforced.

- The UK hopes to position itself as a global digital asset hub in competition with the US and EU.

- For crypto businesses and investors, this marks both opportunity and regulatory accountability.

Introduction: A New Regulatory Era for Digital Assets

The UK’s Financial Conduct Authority (FCA) is preparing to implement a comprehensive regulatory framework for cryptocurrency businesses by 2026. Unlike traditional financial institutions, crypto platforms operate in highly volatile and decentralized environments. The FCA acknowledges that existing banking regulations cannot be applied wholesale and instead seeks a model that balances consumer protection, cybersecurity, and innovation.

This move places the UK alongside global peers like the European Union with its MiCA (Markets in Crypto-Assets Regulation) and the United States with evolving SEC enforcement. The UK is signaling that it intends to remain competitive as a financial hub while addressing crypto-specific risks.

FCA’s Proposed Adjustments: Tailoring Rules for Digital Assets

Relaxed Requirements for Management and Operations

One of the most striking elements of the FCA’s draft plan is the relaxation of certain obligations for crypto firms. These include:

- Traditional management responsibility structures applied to banks and investment firms.

- Strict internal systems and operational management requirements.

- Mandatory cooling-off periods for retail purchases.

The FCA argues that cryptocurrencies do not pose the same systemic risks as banks and that legacy frameworks designed for centralized intermediaries often do not fit decentralized, blockchain-based platforms.

Cooling-Off Periods Deemed Ineffective

In conventional finance, cooling-off periods allow retail investors to withdraw from risky products. The FCA, however, plans to remove this requirement for crypto. Given the extreme volatility of digital assets, such measures offer limited protection. Instead, the focus will shift toward clearer risk disclosures warning that consumers may lose their entire investment.

Outsourcing Rules and Blockchain’s Disintermediation

Banking regulation often emphasizes strict controls over outsourced functions. However, in crypto, transactions often occur without intermediaries due to blockchain technology. The FCA intends to modify outsourcing oversight accordingly, while still requiring transparency and accountability for firms that rely on third-party service providers.

Cybersecurity at the Core of Regulation

The FCA emphasizes cybersecurity as a central pillar of its future framework. With rising threats of hacks, phishing, and smart contract vulnerabilities, regulators are pushing firms to:

- Implement robust security protocols.

- Conduct regular penetration testing.

- Ensure secure custody of client assets.

- Maintain transparent incident reporting.

This mirrors global trends: in the US, the SEC and CFTC have both tightened reporting rules for cyber incidents, while the EU’s Digital Operational Resilience Act (DORA) sets new cyber compliance standards for financial institutions, including crypto service providers.

Why Old Rules Don’t Fit: A Technological Shift

David Geale, FCA’s Executive Director of Markets and Digital Finance, has highlighted that “copy-pasting banking rules onto crypto will not work.” Blockchain eliminates intermediaries, introduces smart contract automation, and operates with extreme price volatility. These realities require a framework that:

- Recognizes the role of decentralized technology.

- Accepts the absence of systemic risk (for now) but anticipates future scaling challenges.

- Differentiates between centralized exchanges and decentralized protocols.

Global Context: The UK vs. US and EU

EU’s MiCA as a Benchmark

The EU’s MiCA framework, which comes into effect in phases through 2024–2026, already sets passportable licensing standards, stablecoin issuance rules, and disclosure requirements across all 27 member states. It has been praised for clarity but criticized for its rigidity in fast-moving markets.

US Uncertainty

In contrast, the US regulatory landscape remains fragmented. The SEC continues to pursue enforcement actions against major exchanges, while Congress debates whether a unified framework should fall under the SEC, CFTC, or a new agency. This uncertainty has driven some firms to relocate operations abroad.

The UK’s Strategic Positioning

By 2026, the UK aims to craft a “middle path”: flexible enough to foster innovation but strict enough to maintain consumer confidence. The FCA’s messaging suggests it wants to avoid driving crypto companies offshore while still ensuring investor protection.

Implications for Crypto Companies

For crypto platforms, these regulatory shifts mean:

- Lower compliance burden in areas like cooling-off and outsourcing.

- Higher obligations in cybersecurity and consumer protection.

- Strategic clarity by 2026, which could reduce legal uncertainty.

Firms that align early with FCA’s expected standards may gain first-mover advantages in accessing institutional partnerships, securing banking relationships, and attracting UK-based retail customers.

Implications for Investors and Traders

For individual investors, FCA regulation offers both opportunities and warnings:

- More secure platforms, with higher standards for cybersecurity.

- Clearer risk disclosures, ensuring investors understand volatility.

- Potential expansion of regulated offerings, including new tokens, ETFs, and custody services.

However, investors should not assume regulation eliminates risk. The FCA has stressed that crypto assets remain highly speculative, and consumers may lose 100% of their investment.

Charts and Figures

[Insert Graph 1: Global Crypto Regulatory Timeline (2023–2026)]

- EU: MiCA full implementation by 2026.

- UK: FCA framework by 2026.

- US: Uncertain, enforcement-driven.

- Asia: Singapore, Japan, and Hong Kong pushing innovation-driven regulation.

[Insert Graph 2: Key Regulatory Focus Areas]

- Relaxations: management rules, cooling-off, outsourcing.

- Reinforcements: cybersecurity, consumer duty, transparency.

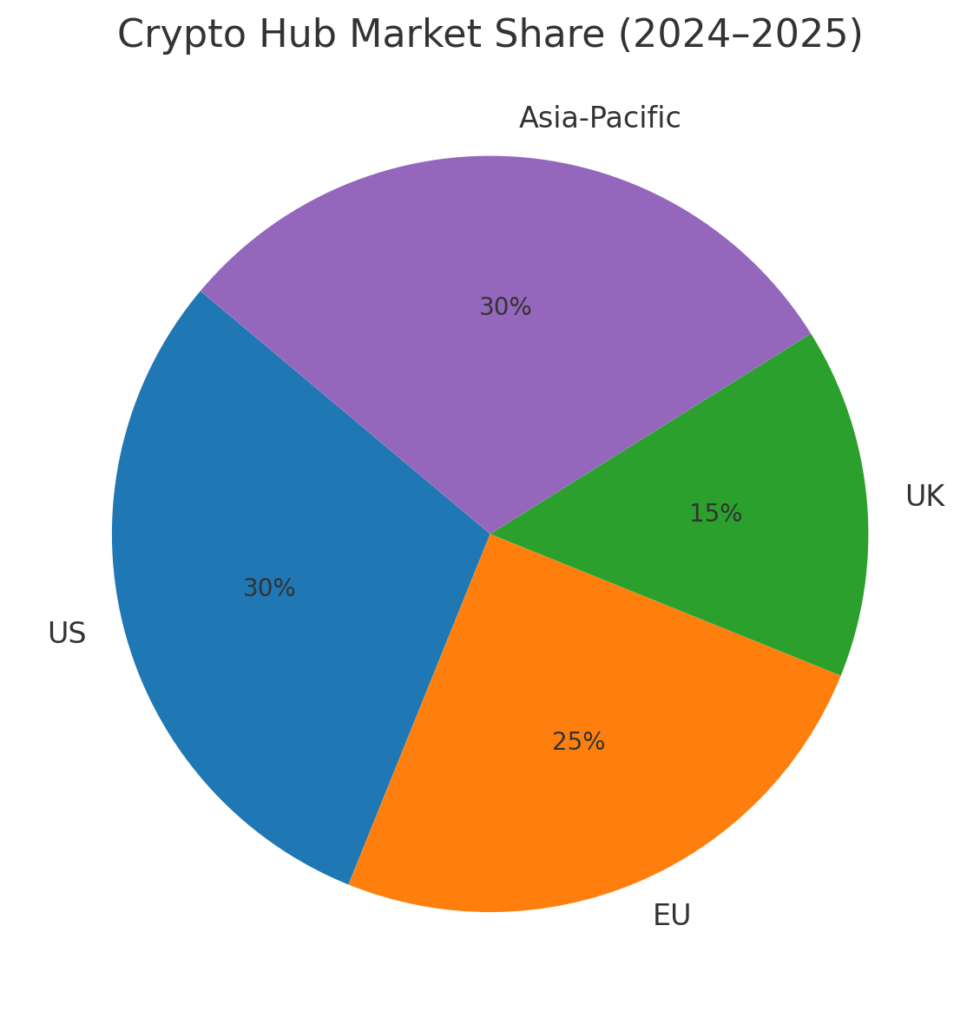

[Insert Graph 3: Market Share of Crypto Hubs (2024–2025)]

- US, EU, UK, Asia-Pacific breakdown.

Conclusion: The Future of the UK as a Digital Asset Hub

The FCA’s upcoming regulatory framework represents a pivotal shift for the UK crypto ecosystem. By recognizing the unique risks of digital assets while avoiding the pitfalls of over-regulation, the FCA seeks to strike a delicate balance.

If successful, the UK could position itself as a leading global hub for digital finance, competing with the EU’s MiCA-driven market and the US, where regulatory uncertainty remains.

For businesses, this is the time to prepare operational systems, cybersecurity, and compliance frameworks in anticipation of 2026. For investors, this signals a maturing market where opportunity and caution must coexist.