Main Points :

- CZ (Changpeng Zhao) has publicly called on banks to adopt BNB, citing its recent market cap milestone and growing utility.

- BNB recently surpassed UBS in market capitalization and hit a new all-time high of about $900-$940 per BNB.

- There are emerging examples of banks and financial institutions experimenting with or offering services related to BNB or the BNB Chain, but full bank adoption faces regulatory, volatility, and integration challenges.

- Corporations are increasingly holding BNB in treasuries; there’s growing institutional recognition of its potential beyond just a trading token.

- Whether banks will meaningfully integrate BNB (for payments, remittances, settlement, collateral, etc.) depends heavily on regulatory clarity, risk management, and the development of stable infrastructure.

CZ’s Call for Bank Adoption of BNB

Changpeng Zhao (CZ), founder of Binance, has laid down a bold proposal: banks should adopt BNB. This call comes at a moment when BNB’s rise in value and usage has given it a level of prominence not often seen by non-stablecoin altcoins.

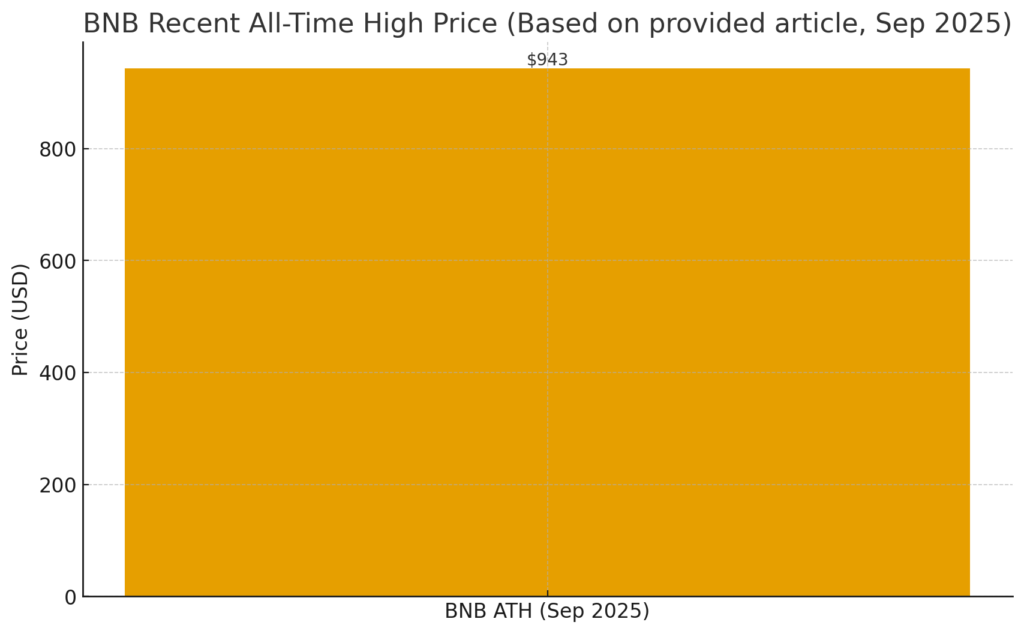

- On or about September 13, 2025, BNB’s price broke its previous records, reaching approximately $929 to $943.

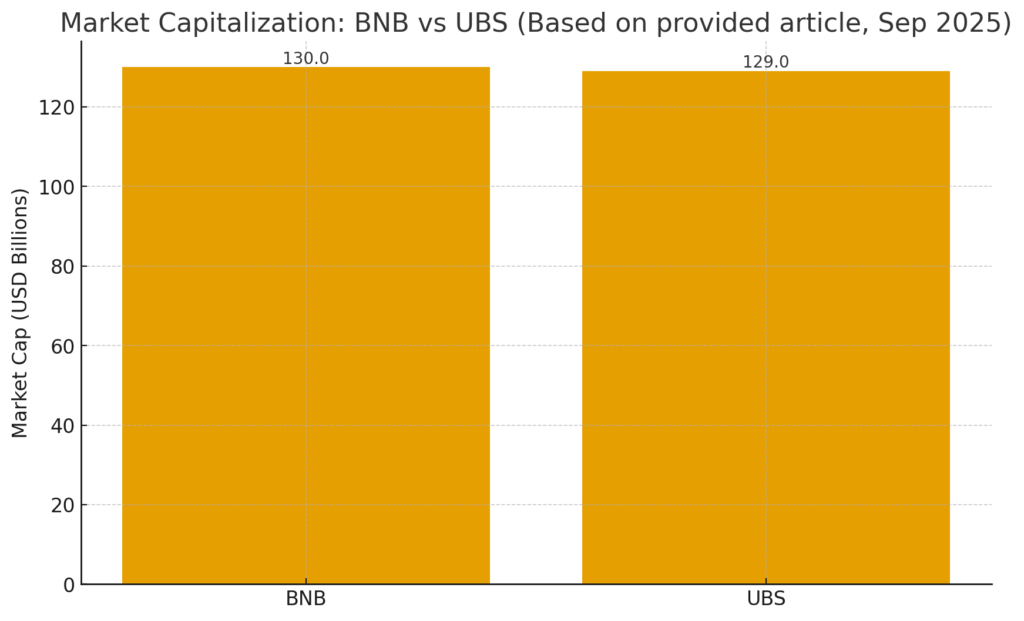

- Market capitalization of BNB has crossed over $130 billion, which according to several sources exceeded UBS’s ~$129 billion.

- In his messaging, CZ has offered assistance: “as a small community member, I am happy to help any bank integrate [BNB].”

The proposal is not just rhetorical. CZ seems to be positioning BNB not only as a speculative token or utility token for Binance fees, but as part of a broader infrastructure: payments, DeFi, cross-chain transactions, governance via BNB Chain, possibly even as a settlement or collateral asset.

Market Momentum and Institutional Signals

BNB’s push for wider recognition is underpinned by strong market performance and signs of institutional interest.

- BNB’s all-time high (ATH) in mid-September 2025 was around $900-$940 per token.

- Stablecoin inflows to the Binance ecosystem and regular coin-burns of BNB are cited by analysts as supporting its price strength.

- Analysts are projecting further gains, some targeting around $1,300 for BNB if its bullish price breakout continues.

Institutional and corporate interest:

- A major partnership was announced between Binance and Franklin Templeton, aimed at creating digital asset products for global institutional investors. This has been taken as a signal of deeper institutional confidence in BNB.

- Several corporations (including biotech, semiconductor, and other non-crypto native industries) have begun adding BNB to their treasuries. For instance, Windtree Therapeutics, Nano Labs, and BNC have allocated meaningful amounts into BNB holdings.

- Institutional trading access has expanded: in Hong Kong, the licensed exchange OSL has begun offering BNB for professional/institutional investors (those meeting high thresholds) under regulated conditions.

Use-Cases & Existing Integrations

While full bank adoption remains mostly aspirational, there are existing integrations or pilot examples that suggest what is possible.

- OSL (Hong Kong): supports professional investor trading of BNB with stablecoin pairs (USDT, USDC) and US dollar.

- Corporate treasury holdings: companies beyond crypto sector are diversifying into BNB, treating it akin to a strategic asset in their balance sheets.

These use-cases illustrate potential banking-adjacent roles: payments, settlement, collateralization, or even remittances leveraging BNB Chain infrastructure.

Barriers: Regulation, Volatility, Trust

However, several serious obstacles must be addressed before banks broadly embrace BNB.

- Regulatory Risk and Licensing

- Many jurisdictions still have unclear or evolving rules around cryptocurrencies, especially non-stablecoins.

- Banks are highly regulated; integration of crypto tokens requires clarity around anti-money laundering (AML), know your customer (KYC), consumer protection, taxation etc.

- Price Volatility

- BNB is not a stablecoin. Its price moves with market sentiment, which makes using it for payments or as part of core banking infrastructure risky unless volatility is hedged or managed.

- Institutional Trust & Auditing

- Banks require auditable, transparent systems. They need to trust the underlying blockchain infrastructure, governance, security, custody.

- Integration Complexity

- Operationally, integrating a token into settlement systems, payments networks, or using it as collateral involves technical, compliance, and risk management work.

- Regulatory Reputation Risk

- Because Binance and BNB have been under regulatory scrutiny in various countries, banks may fear reputational risk by association.

Recent Regulatory & Industry Trends

To give more context, here are related developments that help frame the likelihood of BNB’s banking adoption:

- In the U.S., major banks (e.g. Citigroup) are exploring custody and payment services for stablecoins and other digital assets following regulatory changes.

- Hong Kong continues to push to be a regional hub for virtual assets; licensed exchanges making more tokens (including BNB) available for professional investors under regulated frameworks. This helps build the bridge between crypto and traditional finance.

- The broader trend: tokenization of assets, interest in cross-border payments, institutional product offerings are gaining momentum globally. Banks are less interested in speculation now than in utility, compliance, and finance-grade infrastructure.

Market Metrics (Visual Data)

Below is a simple chart comparing BNB market capitalization vs UBS, and BNB price recent highs, to highlight the scale of recent movements.

| Metric | Value |

|---|---|

| BNB price at recent all-time high | ~$929-$943 per BNB |

| BNB market capitalization | ~ $130.6 billion |

| UBS market capitalization (for comparison) | ~ $129.1 billion |

| Analyst target for potential breakout | ~$1,300 per BNB if momentum and conditions persist |

Possible Scenarios for Bank Adoption

Given all of the above, here are some plausible scenarios of how banks might adopt BNB, along with pros/cons and likely timeline.

| Scenario | What Adoption Looks Like | Key Advantages | Main Challenges | Likely Timeline |

|---|---|---|---|---|

| Pilot integrations | Bank allows BNB for payments or remittances; possibly as settlement asset internally; or allows customers to hold BNB with compliance controls | Tests use, builds trust; incremental exposure; helps demand from clients; shows regulatory openness | Risk exposure to volatility; regulatory oversight; technical integration; customer protection concerns | 6-18 months in progressive jurisdictions (e.g. UAE, Singapore, HK) |

| Treasury adoption by banks | Bank puts BNB on its balance sheet as one reserve or asset class | Diversifies bank assets; potential upside if BNB grows; signals confidence | Regulatory capital requirements; risk of loss; volatility; accounting treatment; liquidity issues | 1-2 years if regulatory environment favorable |

| Full integration across services | BNB used for cross-border remittances, payment rails, collateral, lending, etc. | High utility, could reduce costs; create new revenue streams; innovation leadership | Huge infrastructure, regulatory, risk, legal, tax, governance work; market volatility; regulatory risk; public perception | 2-5 years; requires stable regulatory regimes and proving use cases |

Implications for Seekers of New Crypto Assets, Revenue Streams & Blockchain Practitioners

For those who are looking for the next crypto-asset to invest in, or revenue opportunities, or practical blockchain applications, BNB’s current trajectory suggests:

- Potential Reward vs Risk: BNB is showing strong upward momentum and institutional interest. If bank adoption begins, there could be significant upside. But volatility remains high.

- Use-case Expansion: Projects built on BNB Chain, payments, DeFi, NFTs etc., may benefit if BNB becomes more accepted. Developers might target integration with banking rails or services.

- Regulation Matters: Success depends heavily on local regulation. Jurisdictions with clear crypto regulation, openness to digital asset custodial services, or favorable policies are more likely to be first movers.

- Partnership Opportunities: Entities (fintechs, payment providers, remittance services) might find opportunities to collaborate with BNB or Binance ecosystem to build bridges to banks.

Recent Criticism & Skepticism

Not everyone in the crypto community or finance sector is convinced:

- Some question whether banks will adopt a token issued by a crypto exchange because of concerns about conflicts of interest, regulatory risk, or perceived lack of neutrality.

- Volatility is a core concern: for payments or settlement, high fluctuation undermines usability.

- Regulatory uncertainty: many banks operate in multiple jurisdictions; they tend to avoid assets that may become subject to bans or severe regulation.

Conclusion

BNB’s rise is more than just another altcoin bull run. With its market cap now exceeding that of major private banks like UBS, high price records, increasing institutional engagement (corporate treasuries, regulated exchanges), and CZ’s explicit call for adoption by banks, there is a credible trajectory toward BNB becoming more than a utility token inside the crypto bubble.

However, full-scale adoption by banks—using BNB in payments, settlement, remittances, or collateral—requires overcoming serious challenges: regulatory clarity, risk oversight, volatility management, accounting and legal frameworks, trust and custody infrastructure.

For practitioners and investors seeking new assets or revenue sources, BNB is one to watch closely: it lies at the intersection of speculative upside and potential structural change. Those positioning now—especially in supportive regulatory environments—might gain significant advantage if BNB’s institutional role expands.