Main Points :

- SEC Chair Paul Atkins has declared that “the era of crypto has arrived,” with a shift away from enforcement-heavy regulation toward clear, predictable rules.

- Under his “Project Crypto” initiative, most crypto tokens will not be treated as securities; regulatory frameworks will be clarified for issuance, custody, trading, lending, and staking.

- A “super-app” model is proposed, in which platforms can provide integrated crypto services—trading, lending, staking—and offer multiple custody options under a unified regulatory regime.

- Emphasis on minimizing regulatory burden: regulations should be “minimum effective dose” to protect investors, avoid overlapping license/regime requirements, allow competition and innovation.

- U.S. looks to international models, especially the EU’s Markets in Crypto-Assets (MiCA), and wants coordination globally.

- Rulemaking will also include clarifying when a token is a security, safe harbors and exemptions, allowing tokenized securities and on-chain markets.

Introduction: SEC’s New Message

Paul Atkins, the current Chairman of the U.S. Securities and Exchange Commission (SEC), delivered a major policy shift in September 2025, declaring at an OECD roundtable in Paris that the cryptocurrency era has officially arrived. His message is clear: the previous regulatory approach—which was often adversarial, reactive, and marked by enforcement actions without clear rules—is being replaced with comprehensive, predictable regulation tailored to the digital asset era.

Project Crypto: Framework and Goals

“Project Crypto” is the flagship initiative of Chairman Atkins. Its goals are multifold: to modernize and adapt securities laws to recognize the realities of blockchain, digital assets, token offerings, and on-chain markets. A central tenet is that most crypto tokens are not securities, meaning they won’t be subject automatically to securities regulation, though those that are will get clearer rules.

Key aims include:

- Defining clear lines for token classification (security vs. non-security) so that innovators aren’t operating in legal uncertainty.

- Establishing transparent rules for token issuance, custody, trading, staking, and lending.

- Encouraging on-shoring of token distributions (i.e., moving token offering activity back into the U.S.) to reduce offshore legal structures and uncertainty.

The Super-App Vision: Unified Platforms

A key component of Atkins’ vision is the idea of “super-apps” in the crypto space. These are platforms that under one umbrella license can:

- Offer trading, staking, lending, and possibly other services, instead of requiring separate licenses or having to segment services.

- Support multiple custody options, including self-custody, and allow both crypto assets that are securities and those that are not to be traded side by side, reducing friction.

- Operate under more streamlined licensing/regulatory requirements to reduce the compliance burden and barriers to entry.

This model is intended to foster innovation, encourage competition, and allow smaller companies to compete by not being overwhelmed by regulations designed for large incumbents.

Comparisons & International Influences

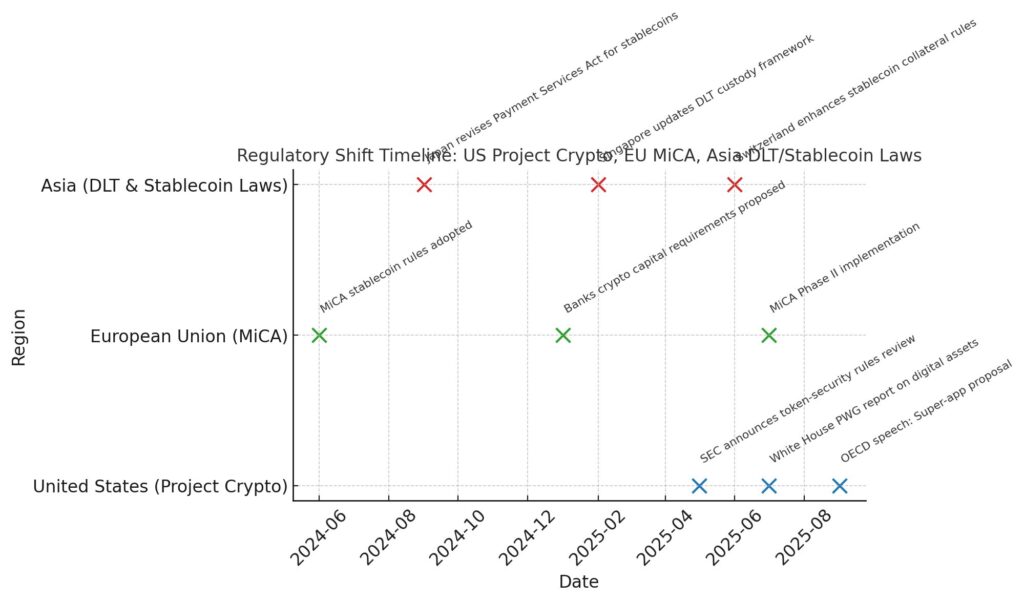

Atkins has looked outward, citing Europe’s MiCA (Markets in Crypto-Assets) framework as a useful model. He noted how other jurisdictions are advancing regulations for unbacked crypto assets, stablecoins, custody laws, and digital-asset banking. Specifically:

- The European Banking Authority is proposing strict capital requirements for banks holding unbacked crypto assets like Bitcoin or Ether.

- Other countries like Switzerland are advancing updated distributed ledger (DLT) laws to support custody and stablecoin guarantees.

These examples are being used to inform U.S. policy, especially in how to balance investor protection with innovation.

What’s New Since Earlier Developments

To place this in context, some recent developments and changes that reinforce this direction:

- Earlier in 2025, Atkins and his administration withdrew or paused many enforcement cases and proposed rules initiated under the previous SEC chair, signaling a break from the previous regime.

- The White House’s President’s Working Group on Digital Asset Markets released a lengthy report recommending legislative and regulatory changes to support the digital-asset industry. Atkins is leaning on that as a blueprint.

- There is legislative momentum: stablecoin regulatory frameworks, crypto market structure bills, etc., are being discussed in Congress, which may codify many of the ideas Atkins is promoting.

Implications for Practitioners, Innovators, Investors

For entrepreneurs, blockchain developers, token projects, and investors, these shifts offer both opportunities and areas to watch closely:

- Projects may find it easier to launch tokens and conduct fundraising if the token is non-security, or if the security classification is made clear in advance. Reduced legal uncertainty lowers risk.

- Platforms that can combine multiple services (trading, staking, lending) will have competitive advantage if regulatory frameworks enable “super-apps.” Those that can offer flexible custody—including self-custody—will be favored.

- Companies operating globally will pay attention to how U.S. rules align with foreign frameworks like MiCA; where divergence exists, there may be arbitrage but also risk of regulatory mismatch.

- Investor protection remains a concern: even while easing burdens, regulators will likely insist on minimum required disclosures, auditing, safeguards, and anti-fraud mechanisms.

Risks & Challenges Ahead

- Defining what constitutes a “security” for a token is legally and technically complex; there will be debates over the application of the Howey test (or whatever replaces or refines it).

- Ensuring that “super-apps” do not pose systemic risks—especially regarding custody of assets, conflicts between services, consumer protection, governance.

- Regulatory harmonization: U.S. states, federal agencies (SEC, CFTC, banking regulators) will all need to coordinate, which can be slow and adversarial.

- Lobbying and political risk: changes to regulation often provoke pushback from various stakeholders, including traditional finance players who may see competition, or from those worried about risk.

Case Examples / Recent Moves

In the U.S.:

- May 2025: Atkins announces plans to clarify token-security rules, examine non-security tokens for broker-dealer ATS platforms.

- July 2025: White House (President’s Working Group) issues report; Atkins launches “Project Crypto” speech.

- September 2025: OECD speech with super-app proposals; emphasis on unified licensing, flexible custody.

In Europe:

- MiCA frameworks progressing, rules for banks holding unbacked crypto; stricter capital weights.

In Asia:

- While specifics vary, some countries updating DLT, stablecoin, and custody laws. (e.g. Singapore, Japan) — less uniform, but generally moving toward more regulatory clarity. (Note: sources are more limited for Asia in these recent articles.)

Summary & Look Ahead

Paul Atkins’ leadership at the SEC marks a turning point: moving from a regulatory model heavy on enforcement and ambiguity toward one that seeks predictability, clarity, and an environment where innovation can flourish. If executed well, “Project Crypto” and the super-app strategy could lower barriers for startups, foster competition, and help the U.S. regain leadership in digital assets.

However, there are many moving parts—defining token status, ensuring investor protections, coordinating across regulators (both domestic and international), and avoiding unintended risks from consolidating multiple services into single platforms.

For those seeking new crypto projects or revenue streams, some key takeaways:

- Watch for token projects that leverage non-security classification or those that can demonstrate clarity in their legal status.

- Identify or build platforms that could act as super-apps—if licensing structure allows, such platforms may capture large market share.

- Observe legislation under consideration in Congress—stablecoin regulation, capital market structure laws—as these may enshrine or modify parts of Project Crypto.

- Opportunities may arise in tokenized securities, custody solutions, staking/lending services under one roof, or cross-border services aligned to U.S. and international regulations.

Conclusion

The U.S. is entering a new chapter in its relationship with cryptocurrencies and blockchain technology. Paul Atkins’ SEC is signaling that it wants to lead not by punitive enforcement but by laying out clear rules of engagement. For innovators, this could be a generational opportunity: one where regulatory certainty unlocks latent value, where platforms that combine services (super-apps) become viable, and where token offerings are not hampered by fear of retrospective enforcement. Yet, turning vision into functioning, safe markets will require careful legal drafting, robust investor protection, and international coordination. The next 12-24 months will be critical: for regulation, for projects, and for investment decisions.