Main Points :

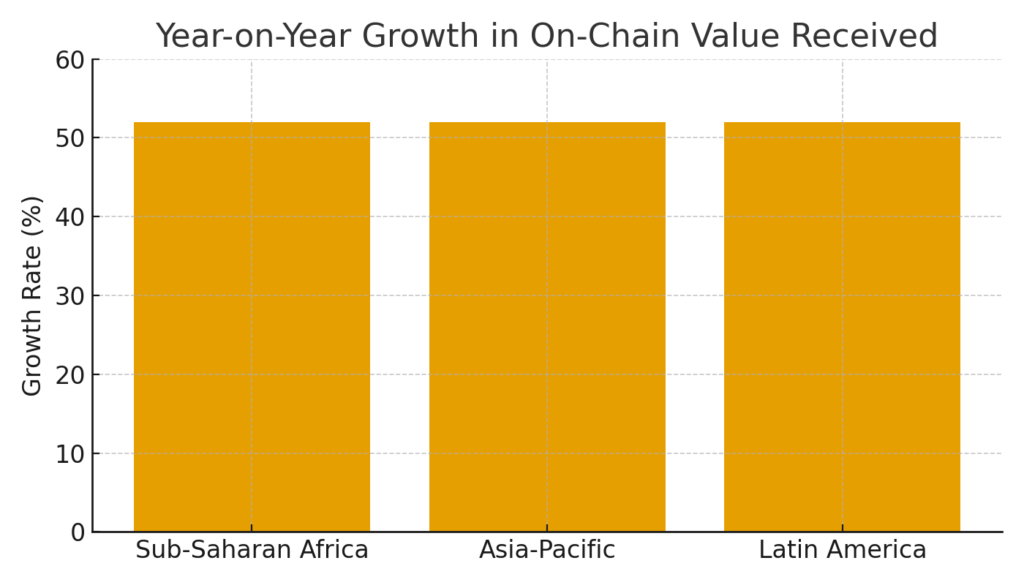

- Sub-Saharan Africa saw 52% year-on-year growth in on-chain crypto value received, reaching US$205 billion for July 2024–June 2025.

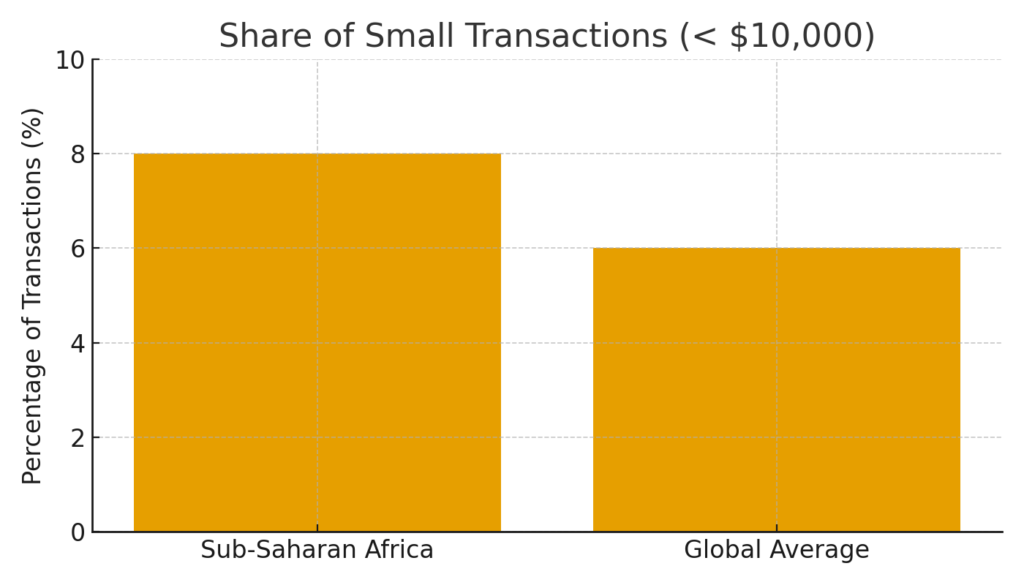

- Retail transactions (under US$10,000) account for over 8% of total value in the region, higher than the global average of ~6%, indicating grassroots / real-world use.

- Key countries: Nigeria led with about US$92.1 billion in received on-chain value; South Africa distinguished by its regulatory environment and rising institutional activity.

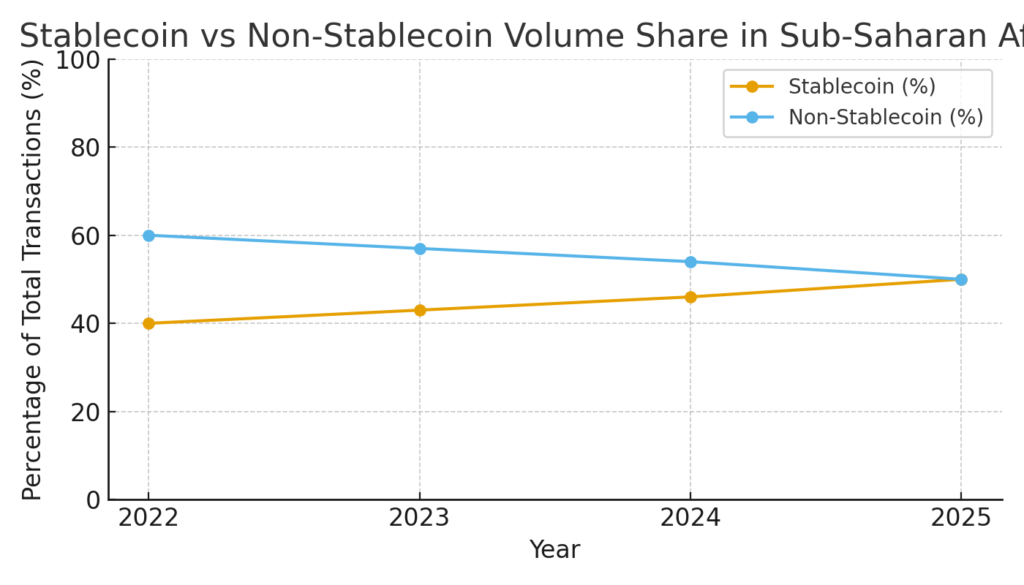

- Stablecoins are playing a large role in institutional flows and cross-border trade, as hedge against inflation, dollar access, and as substitute when fiat/local currency is volatile or foreign currency is hard to obtain.

- Emerging local regulated stablecoins are appearing (e.g. cNGN in Nigeria) aiming to serve local need rather than relying exclusively on USDT/USDC.

- Regulatory clarity (especially in South Africa) is enabling institutional players to move from exploration to real services: custody, product offerings, stablecoin issuance.

- Concerns and risks include fiscal implications (seigniorage, lost tax base), regulation fragmentation, infrastructure / identification bottlenecks, and competition between private stablecoins vs CBDCs.

Institutional and Retail Adoption: Subtitles & Analysis

Grassroots & Retail Use Takes Off

For many people in Sub-Saharan Africa, crypto is no longer just speculative: it’s practical. Transactions of under US$10,000 represent over 8% of on-chain value in the region, compared to ~6% globally. This reflects everyday applications: remittances, payments, savings, hedging against inflation, avoiding devaluation of local currencies. In countries where banking penetration is low, many are turning to digital assets because traditional financial infrastructure is lacking.

Stablecoins as Core Infrastructure

Stablecoins, especially US-dollar-pegged tokens (USDT, USDC etc.), are increasingly being used for cross-border trade, institutional payments, merchant payments, and as substitute for hard currency in local economies. In Nigeria, persistent inflation and limited access to foreign currency are pushing people and institutions toward stablecoins.

Also, the arrival of locally regulated stablecoins is a recent development: for example, cNGN in Nigeria became Africa’s first regulated native stablecoin (backed 1:1 by naira reserves), fully compliant with Nigerian Securities and Exchange Commission (SEC) under special regulatory incubation. This indicates opportunities: local stablecoins might gain trust, avoid some regulatory risks, and better respond to local regulatory landscapes and on-the-ground needs.

Institutional Players & Regulatory Maturation

In addition to retail, institutions are increasingly involved. In South Africa, with clearer regulation, virtual asset service providers are registered/licensed; banks and large firms are exploring custody, product offerings, stablecoin issuance.Nigeria also sees large inflows in on-chain value, and institutions are participating more, particularly in cross-border stablecoin flows.

Regulatory clarity seems a key enabler. South Africa’s legal/regulatory frameworks provide certainty, which reduces risk for institutional adoption. Regulatory fragmentation across other countries remains a challenge.

New Local Projects & Stablecoin Innovation

Projects like cNGN show how local stablecoins can emerge, tapping local needs. It is fully backed by naira, launched in early 2025, growing transaction volume and integrating with local fintechs. Such projects may offer higher adoption potential if they avoid over-dependence on foreign stablecoins and comply with local law. Also business cases are expanding: payments, payroll, supplier payments via stablecoins are rising.

Risks, Risks & Bottlenecks

While growth is strong, there are several things to watch:

- Regulatory uncertainty in many countries: diverging rules, unclear definitions, potential crackdowns could reverse momentum.

- Fiscal impact: stablecoin adoption may reduce demand for local currencies (seigniorage revenue), make tax base erosion more likely, complicate government revenue projections.

- Infrastructure & identity issues: many lack IDs, banking access, internet/mobile connectivity, especially in rural regions. This hampers full participation.

- Competition from CBDCs, and whether they succeed: e.g. Nigeria’s eNaira has very low activity; local stablecoins may be preferred.

Recent Developments (Beyond the Base Report)

- cNGN: As noted, Africa’s first regulated locally-issued stablecoin in Nigeria; increasing adoption and transaction volume.

- Business use of stablecoins growing: According to Yellow Card, stablecoins accounted for ~43% of all crypto transaction volume in Sub-Saharan Africa in 2024. Business operations like payroll, treasury, supplier payments increasingly use stablecoins.

- Cross-border trade & remittances: Stablecoins are playing role in trade flows between Africa, Middle East, Asia; also, they are seen as cheaper/faster remittance rails versus traditional ones.

- Regulation incubation: Local regulators are beginning to incubate projects (as with cNGN), issue licenses for virtual asset service providers, clarify regulatory frameworks (South Africa being an example).

Implications for New Assets / Potential Revenue Sources / Practical Blockchain Use

For people/investors/practitioners looking into the next crypto or blockchain-based opportunity, the following areas look promising:

- Localized stablecoins or fiat-pegged tokens that are regulated and backed locally. These reduce regulatory risk, align with local monetary policy, and may benefit from both retail and institutional demand.

- Payment / remittance rails built on stablecoin infrastructure: companies that enable cheap cross-border payments, payroll across borders, merchant payments in stablecoin could gain traction.

- Onshore custody and institutional financial infrastructure: as regulatory frameworks mature (especially in South Africa and Nigeria), there is likely demand for custody providers, compliance services, exchange/licensing, KYC/AML, etc.

- DeFi / Web3 services addressing real-use cases: beyond speculation: savings, hedging (inflation protection), identity, supply chain, energy infrastructure. Particular attention to mobile money integration.

- Regulatory consulting / compliance / infrastructure: helping projects navigate varied country-by-country regulation, ID/identity verification, technical infrastructure (mobile, Internet, blockchain networks) in regions with weaker existing systems.

- Potential risk-aware yield or yield-bearing stablecoin products — though yield is not yet the primary driver, but financial products built around stablecoin savings or short-term fixed income may be well-received if trustable.

Suggested Graph / Diagrams (to Insert)

(Here are suggestions for graphs; you or your design team can create them. I will indicate insertion points.)

- Graph 1: Year-on-year growth in on-chain value received in regions: Sub-Saharan Africa vs Asia-Pacific vs Latin America (showing +52% for SSA, higher for APAC/LatAm). Insert after “Institutional and Retail Adoption” section.

- Graph 2: Comparative share of small-value transactions (< US$10,000) in SSA vs global average. Insert in “Grassroots & Retail Use Takes Off” section.

- Graph 3: Breakdown of stablecoin vs non-stablecoin volumes in SSA over time (past 2-3 years), with Nigeria and South Africa highlighted. Insert around “Stablecoins as Core Infrastructure”.

Summary

Sub-Saharan Africa is emerging as a “laboratory” for real-world adoption of crypto: not because people are speculating, but because crypto solves real problems—currency devaluation, limited foreign currency access, remittances, lack of traditional banking. Institutional adoption is catching up, aided by regulatory clarity in some countries (South Africa a leader), and local stablecoin projects (like cNGN) are beginning to compete with global stablecoins.

For investors, developers, or companies seeking opportunities, the biggest potentials lie in stablecoins, payments rails, custody/infrastructure, localized assets, and services that address financial inclusion. But the risks are nontrivial—regulation, tax policy, identity & infrastructure gaps, competition, and the need for trust.