Main Points :

- Japan Post Bank is planning to issue DCJPY (Digital Currency JPY) to depositors in fiscal year 2026.

- DCJPY is a tokenized deposit pegged 1:1 with the Japanese yen, created by DeCurret DCP under IIJ Group.

- Users will link existing savings accounts to a DCJPY-specific account and convert yen to DCJPY at parity.

- DCJPY will be usable for instant settlement of security tokens (digital securities) and NFTs.

- The bank aims to streamline distribution of government subsidies, enhancing administrative efficiency.

- Leveraging Japan Post Bank’s massive deposit base (~¥190 trillion / $1.29 trillion), DCJPY is set to underpin fintech expansion and appeal to younger demographics.

1. DCJPY Launch Overview

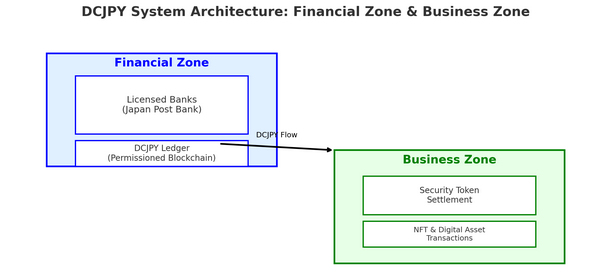

Japan Post Bank (Yū‑cho Bank) is set to launch a digital currency named DCJPY in fiscal year 2026. Developed by DeCurret DCP, part of the IIJ Group, DCJPY functions as a tokenized deposit rather than a typical stablecoin.

Depositors will be able to link this DCJPY account to existing savings accounts, converting desired amounts at a fixed rate of ¥1 = 1 DCJPY. Unlike JPYC, which is a public stablecoin pegged to the yen, DCJPY is managed on a permissioned blockchain by licensed financial institutions.

2. Target Uses: Security Tokens, NFTs, and Fast Settlements

Japan Post Bank intends to deploy DCJPY primarily for instant settlement of security tokens—blockchain-based representations of real-world securities like real estate or bonds—distributing investments efficiently with settlement times far faster than conventional methods. Additionally, DCJPY will support NFT transactions and other digital asset flows.

3. Public Administration Integration: Subsidies via DCJPY

A powerful use case under consideration is the distribution of local government subsidies using DCJPY. In eligible municipalities, subsidy payments could be made automatically and instantaneously to residents via DCJPY, dramatically streamlining administrative workflows.

4. A Leverage of Massive Deposit Base

With approximately ¥190 trillion (about US $1.29 trillion) in deposits across 120‑million accounts, Japan Post Bank has a substantial foundation to support DCJPY issuance and adoption. This gives the initiative significant scale and the potential to drive widespread digital currency usage in Japan.

5. Regulatory Clarity: Permitted Blockchain, Not Stablecoin

Crucially, DCJPY is characterized legally as a tokenized deposit under regulatory frameworks—not a stablecoin issued on public chains. Its design centers on compliance via permissioned blockchains, overseen by authorized financial institutions—ensuring a structure that aligns with Japan’s regulatory environment.

6. Broader Context and Digital Currency Trends

- The Bank of Japan continues its exploration of a CBDC (Central Bank Digital Currency), with progress documented through pilot programs and research milestones, though a decision on issuance remains pending.

- Globally, tokenization markets (RWA – Real World Asset tokenization) are projected to grow from US $600 billion in 2025 to US $18.9 trillion by 2033, highlighting massive macroeconomic opportunity.

- The Japan Digital Currency Forum, involving DCJPY stakeholders, has already conducted local pilot programs—from digital coupons in Aizuwakamatsu to health-related tokens and a tourism pass model—to explore programmable subsidy delivery and immediate settlement in practice.