Main Points:

- The ECB reaffirms that cash and the digital euro will coexist, preserving choice and financial resilience.

- Legal frameworks are being proposed to protect cash acceptance amid growing digital payments.

- The digital euro aims to bolster Europe’s monetary sovereignty against foreign payment providers and stablecoins.

- Public trust and understanding remain critical, as surveys show strong preference for traditional assets.

- A balanced ecosystem combining cash, CBDC, and innovative digital solutions will enhance inclusivity and stability.

1. Cash and CBDC: A Complementary Partnership

The European Central Bank (ECB) has made clear that the digital euro is not intended to replace physical banknotes and coins, but rather to complement them by extending the benefits of central bank money into the digital realm. Executive Board member Piero Cipollone emphasized at the ECB Forum on Central Banking in Sintra that “cash is indispensable as a means of payment and a store of value. We are committed to modernizing banknotes to ensure they remain accessible and widely accepted. The digital euro will complement cash by bringing its advantages into digital payments.” This stance underscores the ECB’s dual-track strategy: modernize the physical currency while simultaneously developing a secure, efficient CBDC.

By offering both forms—physical and digital—the ECB seeks to preserve payment choice for citizens, from cash’s anonymity and offline capability to the digital euro’s online convenience. This duality strengthens Europe’s payment autonomy, ensuring central bank money remains at the core of all transactions, whether in-store or online.

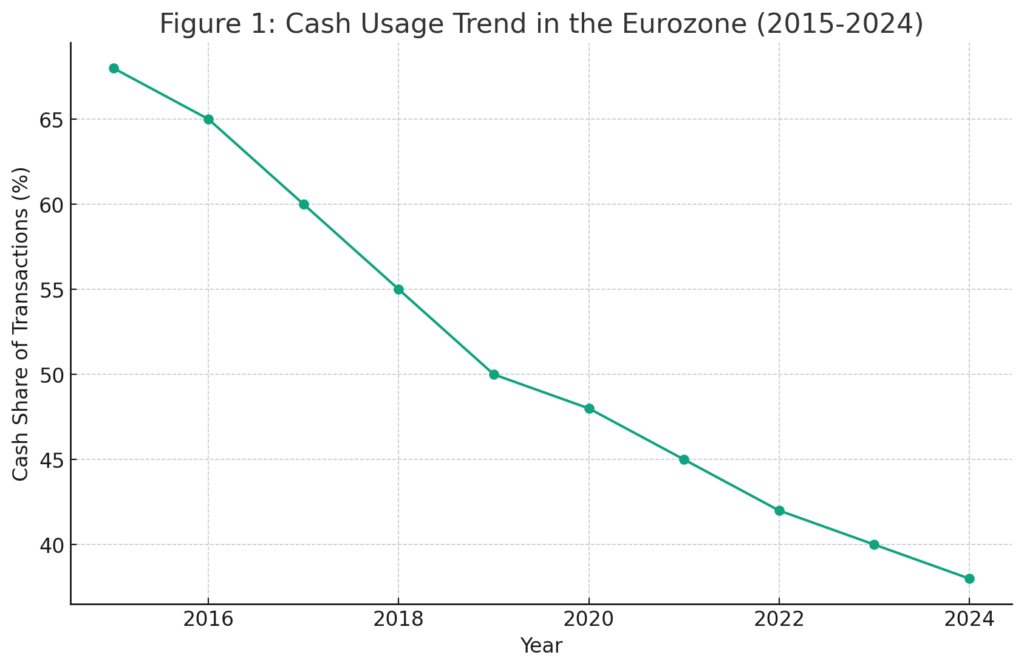

Insert Figure 1 here: Trend of Cash Usage in the Eurozone (2015–2024)

2. Safeguarding Cash Acceptance with Legal Protections

Despite the digital payment surge, the ECB has expressed concern over a growing number of merchants refusing cash. In response, the European Commission has proposed regulations mandating that businesses continue to accept euro banknotes and coins, with penalties for non-compliance. This legal framework is designed to guarantee universal cash acceptance, preserving an essential backup mechanism in cases of cyber-attacks or technical outages that can compromise digital systems.

Cash’s role as an emergency fallback cannot be overstated: it requires no electronic infrastructure and carries no counterparty risk. By embedding cash acceptance in law, the ECB aims to maintain payment resilience across all circumstances, from routine purchases to crisis scenarios.

3. Bolstering Monetary Sovereignty in a Global Landscape

As cross-border stablecoins—particularly those denominated in US dollars—gain traction for everyday transactions, the ECB views the digital euro as a strategic tool to preserve Europe’s monetary sovereignty. With two-thirds of euro-area card payments processed by US firms like Visa and Mastercard, the risk of economic coercion looms large. The digital euro would reduce reliance on these foreign networks, enabling EU residents to conduct secure, central bank–backed digital transactions without external intermediaries.

Under the Markets in Crypto-Assets (MiCA) regulation, euro-pegged stablecoins are expected to emerge, but their adoption has been limited so far, highlighting the ECB’s opportunity and urgency in rolling out its CBDC. As Fabio Panetta, Governor of the Bank of Italy, notes, “Stablecoin issuance tied to the euro remains restricted under MiCA, reinforcing the case for a digital euro to serve cross-border payment needs”.

4. Understanding Public Sentiment and Trust

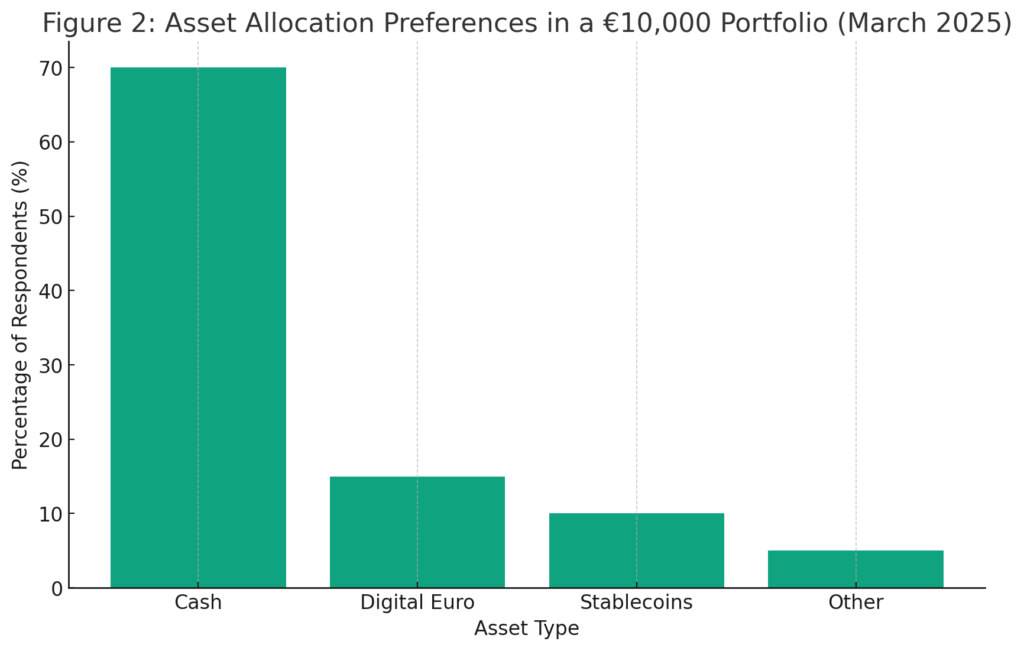

A March 2025 survey asked 10,000 euro-area citizens how they would allocate a €10,000 portfolio. Only 15% opted for the digital euro, while 70% stuck with cash or traditional assets. This reluctance underscores the trust gap the ECB must bridge through public education and transparent design features, such as privacy safeguards and offline functionality.

Insert Figure 2 here: Asset Allocation Preferences in a €10,000 Portfolio (March 2025)

Analysts emphasize that building confidence in the digital euro will require user-friendly wallets, clear holding limits to prevent bank disintermediation, and robust privacy protections to maintain anonymity for small transactions.

5. Integrating Innovative Technologies: Beyond CBDC

Beyond the CBDC itself, the ECB is exploring how distributed ledger technology (DLT) can support a broader ecosystem of payment options, including euro-denominated stablecoins and programmable money features for automated micropayments. Jürgen Schaaf, an ECB advisor, warns that “unregulated dollar stablecoins could enhance US dominance in international payments. Europe needs to develop its own digital solutions, leveraging DLT to diversify and future-proof its payment infrastructure.”

By investing in interoperable platforms, the ECB aims to foster innovation while ensuring that all digital payment instruments remain anchored to the euro, preserving monetary integrity.

Conclusion

The ECB’s strategy of cash and digital euro coexistence reflects a balanced approach to future finance: safeguarding the proven benefits of physical currency while embracing the efficiencies of CBDC and DLT. Legal protections for cash acceptance, coupled with vigorous public outreach and cutting-edge technology integration, will be key to realizing a resilient, inclusive, and sovereign European payment landscape. As the digital euro project advances toward a final decision in the coming years, stakeholders must collaborate to ensure that both cash and CBDC serve the diverse needs of European citizens, businesses, and cross-border transactions alike.