The U.S. SEC’s August 5, 2025 guidance: liquid staking activities do not constitute securities offerings under the Securities Act.

Services like Lido, Marinade Finance, Jito Sol, and StakeWise are unburdened by registration requirements.

Potential acceleration of Ethereum spot ETF approvals with in-kind staking features.

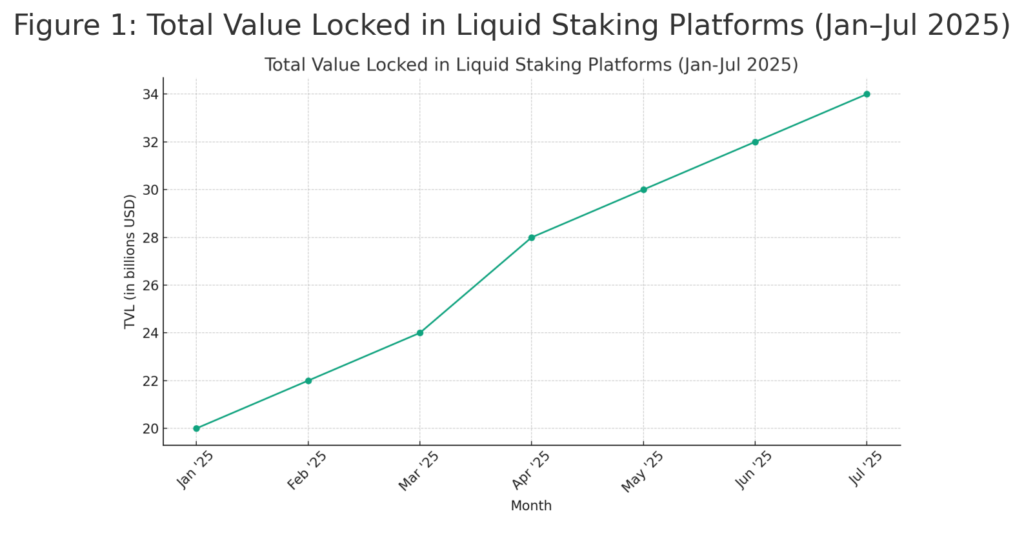

Rapid market growth: liquid staking TVL rose from $20 billion in January 2025 to $34 billion by July 2025 (Figure 1).

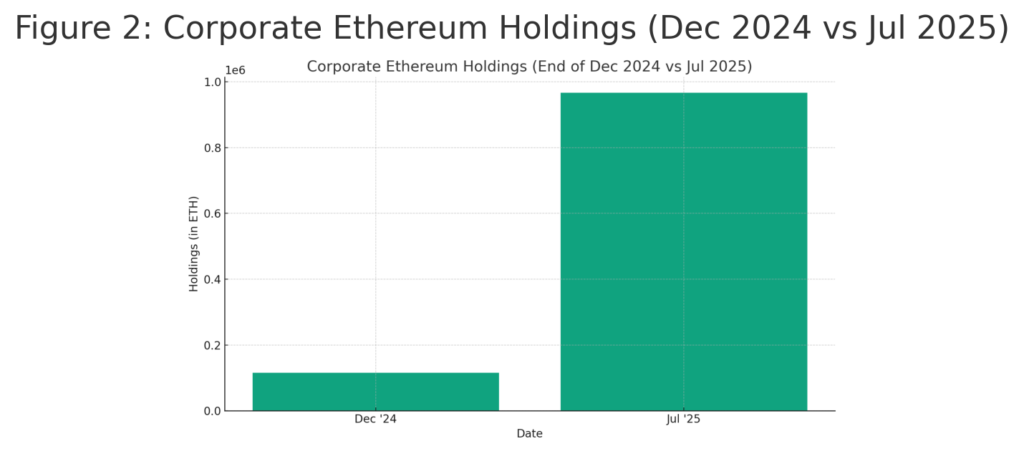

Small public companies’ ETH treasuries ballooned to 966,304 ETH ($3.5 billion) by July 2025, up from 116,000 ETH ($410 million) at end-2024 (Figure 2).

Solana DeFi TVL doubled to $9.3 billion in April 2025, underscoring demand for high-throughput chains.

“Project Crypto” under Chairman Paul Atkins signals an SEC shift toward crypto-friendly regulation.

Industry experts anticipate new product offerings and improved liquidity management across DeFi and institutional markets.

Introduction

On August 5, 2025, the U.S. Securities and Exchange Commission (SEC) released a staff statement clarifying that certain liquid staking activities fall outside the definition of “securities” under the Securities Act of 1933. This landmark guidance marks a pivotal shift in the SEC’s posture—moving from an enforcement-first approach to one that supports innovation in decentralized finance (DeFi). It particularly benefits platforms like Lido and Marinade Finance and sets the stage for staking-enabled exchange-traded funds (ETFs), potentially transforming how institutional and retail investors access staking rewards.

Background on Liquid Staking

Liquid staking allows token holders to lock assets (e.g., ETH or SOL) in a staking protocol to secure a blockchain network, while simultaneously receiving transferable “staking-receipt” tokens that represent their staked positions. These derivatives—commonly dubbed liquid staking tokens (LSTs)—can be traded or employed in DeFi applications, enabling users to earn yield and maintain liquidity.

Historically, the regulatory ambiguity around whether liquid staking involves an “investment contract” (Howey test) has hampered product development. Under the new guidance, however, the SEC clarifies that “the offer and sale of staking-receipt tokens do not constitute securities offerings, provided the underlying staked assets are not part of an investment contract”.

New SEC Guidance Details

The SEC’s Division of Corporation Finance statement explicitly states:

“Staking-receipt tokens, issued in exchange for deposited crypto assets, are not securities unless the underlying relationship meets the definition of an investment contract.”

Key takeaways:

No registration requirement: Liquid staking providers need not register token issuance or trading with the SEC.

Covered services: Lido (LDO), Marinade Finance, Jito Sol, StakeWise, and similar protocols are excluded.

Legal certainty: Clarifies protocols-based and third-party liquid staking are outside securities law.

Precedent for ETFs: Removes a regulatory obstacle for spot Ethereum ETFs that propose in-kind staking features.

Industry Reaction

Industry leaders have broadly applauded the guidance as a catalyst for innovation. Nate Geraci of Novadious Wealth described it as “the last hurdle for staking approval in Ethereum ETFs,” noting that using LSTs for liquidity management within ETFs addresses the SEC’s concerns about liquidity mismatches. Cointelegraph commented that institutions now have a clear legal basis to build staking products, unlocking new market segments.

Conversely, Commissioner Caroline Crenshaw cautioned that the statement’s generalizations may not map neatly onto all services, urging continued vigilance over consumer protections.

Implications for Staking ETFs

The guidance dovetails with ongoing efforts by asset managers to launch spot ETH ETFs with staking capabilities. Traditional ETFs face redemptions in cash, which can force managers to unstake ETH, incurring delays or penalties. By permitting in-kind creations/redemptions with staking derivatives, managers can maintain staked positions and streamline liquidity operations.

Sygnum Research found that revised ETF filings now include in-kind redemptions and staking—instruments not yet seen in U.S. ETF products—with promising signs for approval timelines. Many expect the SEC to permit the first staking-enabled ETF by Q1 2026.

Market Trends and Adoption

Rapid Growth in Liquid Staking TVL

Figure 1 illustrates the explosive growth of liquid staking platforms’ total value locked (TVL) from $20 billion in January 2025 to $34 billion by July 2025—a 70% increase in seven months.

Insert Figure 1: Total Value Locked in Liquid Staking Platforms (Jan–Jul 2025)

Corporate Ethereum Accumulation

Small public companies have significantly expanded their ETH treasuries. By July 2025, corporate treasuries held 966,304 ETH ($3.5 billion), up from 116,000 ETH ($410 million) at year-end 2024—a more than eightfold increase.

While Ethereum dominates, Solana’s DeFi TVL doubled to $9.3 billion in April 2025, driven by its high throughput and low fees—underscoring diversification opportunities for liquid staking outside Ethereum.

Regulatory Landscape under “Project Crypto”

Under Chairman Paul Atkins, the SEC’s “Project Crypto” initiative seeks to modernize U.S. digital-asset regulation, distinguishing token categories and simplifying capital-raising pathways. Project Crypto aligns with the White House’s recommendations to move financial markets “on-chain” and supports proposals to update tax codes for staking rewards, clarify custody rules, and foster tokenized securities markets.

This paradigm shift from enforcement to clear rule-making encourages market-makers, custodians, and institutional investors to build on-ramp products. It also lays the groundwork for global competitiveness by aligning U.S. policy with other jurisdictions that have embraced staking, such as EU’s MiCA frameworks.

Future Outlook

With regulatory clarity in place, the DeFi sector is poised for accelerated product innovation:

Institutional grade staking services: Traditional custodians will integrate LST support.

Tokenized real-world assets (RWA): Combined staking and RWA tokenization models deliver yield and collateralization benefits.

Cross-chain staking aggregators: Simplifying access beyond Ethereum to Solana, Polkadot, and Cosmos ecosystems.

Challenges remain around tax treatment of staking rewards and consumer disclosures. Continued engagement between industry and regulators will be essential to refine these frameworks.

Conclusion

The SEC’s August 5, 2025 guidance is a watershed moment for liquid staking and DeFi innovation in the U.S. By clarifying that staking-receipt tokens are not securities, the SEC has removed a key barrier for protocol builders and asset managers. This development, coupled with “Project Crypto,” sets a pro-innovation tone, likely accelerating the approval of staking-enabled ETFs and laying the foundation for a new generation of DeFi products. Market data—reflected in soaring TVL, corporate ETH accumulation, and growth on secondary chains—validate strong demand for liquid staking. As institutions and retail investors embrace these instruments, the lines between traditional finance and blockchain-native finance will continue to blur, heralding a more liquid, efficient, and transparent digital-asset ecosystem.

About Us and Media

Blockchain and cryptocurrency media covering and exposing the practical application development on the blockchain industry and undiscovered coins.

Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.