Main Points:

- The “21st Century Home Loan Act” mandates consideration of crypto assets in mortgage underwriting.

- Lenders can no longer force conversion of crypto to USD for asset evaluation.

- Builds on FHFA’s June directive treating crypto as eligible assets.

- Enables borrowers to combine verified digital asset balances with traditional assets.

- Could broaden mortgage access for younger, crypto-savvy demographics.

- Part of a broader shift toward digital-era financial regulation under the current U.S. administration.

- Challenges include volatility, valuation standards, and regulatory consistency.

- Recent trends: 28% of U.S. adults own crypto, stablecoin regulation advances, education gaps hinder wider adoption.

1. The 21st Century Home Loan Act

Senator Cynthia Lummis introduced the “21st Century Home Loan Act” on July 29, 2025, aiming to modernize U.S. mortgage underwriting by requiring government‑sponsored enterprises—Fannie Mae and Freddie Mac—to recognize crypto‑recorded assets on secure digital ledgers as part of borrowers’ financial profiles. The bill prohibits lenders from compelling borrowers to liquidate their crypto holdings into U.S. dollars solely for valuation, ensuring that verified digital asset balances can be counted alongside cash, stocks, and other traditional assets in assessing creditworthiness.

2. Rationale: Addressing the Youth Homeownership Gap

Lummis highlighted a decline in homeownership among younger Americans, noting many millennials and Gen Zers accumulate savings in crypto rather than conventional accounts. By acknowledging these assets, the bill seeks to reverse barriers to entry for first‑time homebuyers. “Government entities must evolve to meet the needs of a modern, innovative generation,” Lummis asserted, emphasizing that penalizing crypto users hampers homeownership prospects for those who rely on digital assets.

3. Building on FHFA’s Policy Shift

In June 2025, FHFA Director Bill Parrott issued a directive instructing Fannie Mae and Freddie Mac to treat certain crypto holdings as eligible assets in single‑family mortgage risk evaluations. The new legislation codifies this policy, ensuring long‑term consistency regardless of future administrative changes. While borrowers cannot yet make mortgage payments directly in crypto, the act formalizes inclusion of digital asset balances in debt‑to‑income and loan‑to‑value calculations.

4. Implications for Borrowers and Lenders

- Expanded Borrowing Power: Verified crypto holdings may boost total asset profiles, potentially lowering required down payments or interest rates.

- Valuation Standards Needed: Regulators and industry must agree on fair‑market valuation methods for volatile crypto assets, balancing risk and borrower protection.

- Risk Management: Lenders will need robust frameworks to account for price swings, perhaps requiring periodic revaluation or haircuts on asset values.

5. Industry and Advocacy Reactions

Crypto industry groups have welcomed the act as a milestone for mainstream acceptance, arguing it could unlock homeownership for millions of young adults. However, some mortgage lenders express caution, citing operational challenges and potential legal liabilities. Consumer advocates stress the need for clear disclosure and safeguards to prevent borrowers from overleveraging volatile assets.Insert Figure 1 here

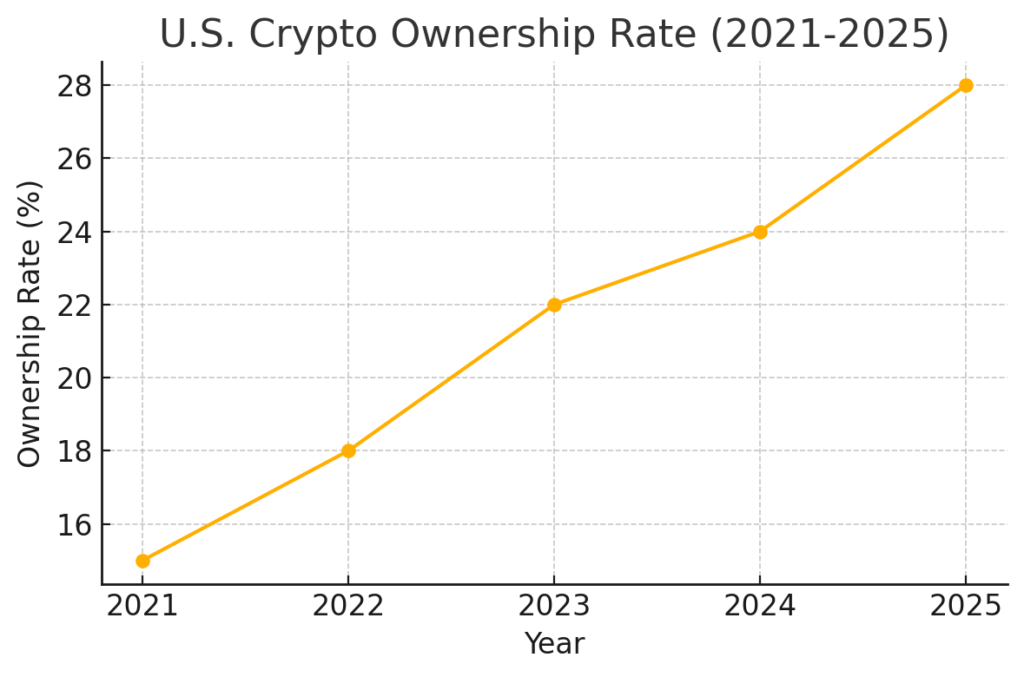

Figure 1: Growth in U.S. Crypto Ownership Rate, 2021–2025

6. Broader Crypto Regulatory Landscape

2025 has already seen significant crypto‑policy developments: the GENIUS Act established clear legal frameworks for stablecoins, fostering corporate and merchant adoption. Yet, widespread education gaps persist: 90% of non‑owners cite insufficient understanding as the main barrier to crypto investment.

7. Adoption Trends and Homeownership Challenges

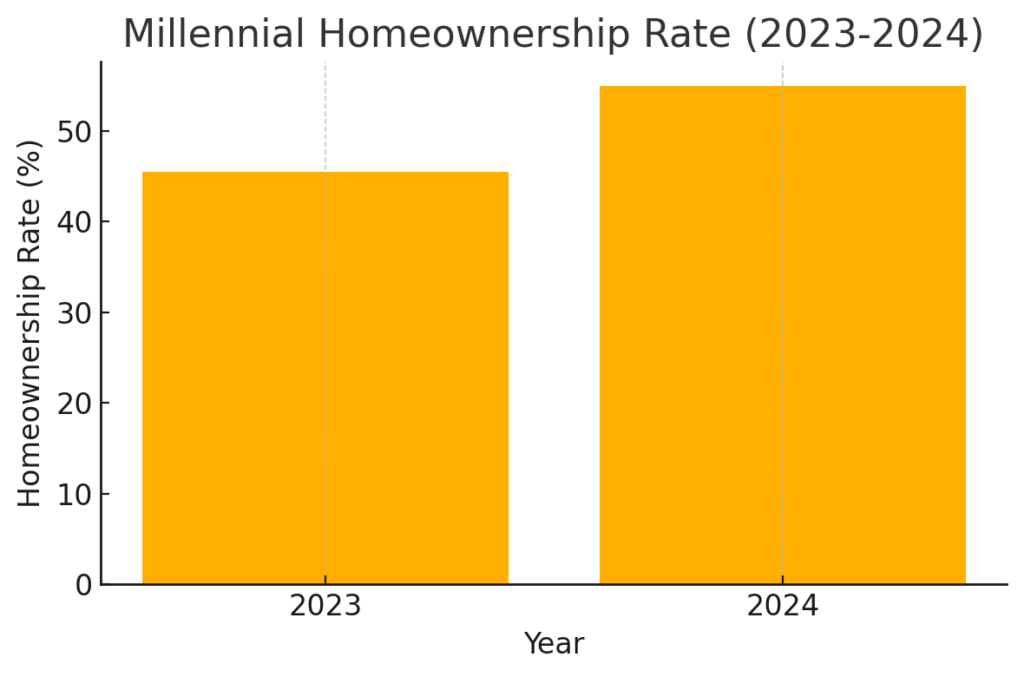

While 28% of American adults (≈65 million) now own cryptocurrencies, homeownership among young adults lags: millennials’ rate was just 45.5% in 2023 and rose to 54.9% in 2024 .Insert Figure 2 here

Figure 2: Millennial Homeownership Rate, 2023–2024

8. Future Outlook and Challenges

As digital assets become integral to personal finance, legislative and regulatory frameworks must adapt. Successful implementation will require:

- Standardized Valuation Protocols: Collaborations between regulators, exchanges, and GSEs.

- Risk Controls: Haircut policies and reserve requirements for lending against crypto.

- Consumer Protections: Clear disclosures and financial education to avoid overexposure.

- Technology Infrastructure: Secure, auditable systems for verifying on‑chain asset balances.

Conclusion

The 21st Century Home Loan Act represents a landmark step in bridging traditional finance and blockchain innovation. By formally integrating crypto assets into mortgage underwriting, the U.S. housing finance system acknowledges the evolving financial behaviors of younger generations. While challenges around volatility, valuation, and education remain, this legislative move could broaden homeownership opportunities and pave the way for further digital‑era reforms in real‑estate finance.